2026-08-08 01:30:26

For a little under a year, everyone — myself included — has compared NVIDIA to Enron, largely because NVIDIA insisted, in detail, that it was nothing like Enron, WorldCom, or Lucent, a potent example of the Streisand Effect that would be much funnier if NVIDIA wasn’t holding up more than 7% of the value of the NASDAQ.

And as I covered in the first part of the Hater’s Guide To NVIDIA last year, there are material concerns about how the company makes money today and will continue to do so in the future.

I will concede that NVIDIA isn’t exactly like Enron in the sense that it isn’t, to my knowledge, doing anything outright fraudulent, like attempting to hide massive amounts of debt inside SPVs as Enron did with its “Raptors,” which I must be clear are distinct from the SPVs used in AI data center debt, though I’ll add that something being legal doesn’t make it a good idea or ethical.

That being said, NVIDIA CEO Jensen Huang has employed many of the same tactics used by Lucent, Nortel, and many of the big dot-com busts, but has been smart enough to make everybody else carry the risk.

Instead of doing direct vendor financing like Lucent did with Winstar (where it effectively loaned its customers money to pay it with), NVIDIA funded neoclouds like CoreWeave, Nebius, and IREN, operating as an early stage investor, IPO anchor, post-IPO investor, $6.3 billion customer and data center lease backstop, allowing them to raise tens of billions of dollars’ worth of debt from overly-eager asset managers and banks, allowing it to do basically the same thing as vendor financing without having to take on any of that messy risk.

These deeply-unprofitable, cash-intensive, debt-riddled companies exist for one purpose — to raise debt to buy NVIDIA GPUs — and would have fallen apart without the AI hype cycle and NVIDIA’s continued backing. Per Kakashii:

In an April 2026 interview with Dwarkesh Patel, Jensen Huang acknowledged my thesis and said it out loud: “In the case of clouds, if we didn’t support CoreWeave to exist, these neoclouds, these AI clouds, wouldn’t exist. If we didn’t help CoreWeave exist, they would not exist. If we didn’t support Nscale, they wouldn’t be where they are today. If we didn’t support Nebius, they wouldn’t be what they are today.” And, confirming that Nvidia wants lots of neoclouds, not just one: “Don’t pick winners. Either let them all take care of themselves, or take care of all of them.”

That is, in Nvidia’s own CEO’s words, the operating logic behind this sector. Rather than build a cloud business on its own balance sheet, which would put Nvidia’s own results directly at risk if utilization or pricing disappointed, Nvidia has helped create and sustain an entire class of nominally independent companies that take on the capital outlay, the construction risk, and the debt of building AI data centers, while Nvidia supplies the chips, frequently invests equity alongside the debt, and in a growing number of cases finances the build out directly.

In other words, NVIDIA has managed to find a way to do vendor financing without ever having to provide any, finding willing supplicants in the various backers of CoreWeave and other neoclouds that would be willing to front the money, all under the mistaken belief that they were funding the next industrial revolution.

To explain exactly how it works, I’ll return to my imaginary scenario from the Big Short 2:

HUANG: So there’re these companies I invest in that, at least in theory, build data centers using my AI GPUs, but I need them to buy more GPUs, so I sign a contract saying that I’ll rent the GPUs back from them in the future. Because NVIDIA has such a strong balance sheet, these companies can raise billions of dollars to buy my GPUs just because I promised to rent them in the future, and the best part is all the risk is held by the companies and the investors. When I need more money, I just sign another contract, they raise more debt, I sell more GPUs.

BAUM: So — just so I have this clearly — you, the guy who makes the GPUs, invest in companies that exist pretty much to buy GPUs from you and rent them to customers. Except you’re the customer too, and a big one.

HUANG: That’s right. We call them neoclouds. S&P just revised CoreWeave’s outlook to positive.

BAUM: That’s fucking crazy.

HUANG: It’s not crazy — it’s awesome.

It’s a win-win-win for NVIDIA, its customers, and the bankers involved. CoreWeave gets to raise more debt and keep its investors strung along on the still-theoretical, ever-expanding timeline of a return on invested capital, bankers get a slew of fees for pulling together the deal, and NVIDIA guarantees itself billions of dollars of business.

And this approach is something where any investment by NVIDIA has a habit of being amplified by others — like Australian startup Firmus, which just raised $2bn from a bevy of investors (including NVIDIA, which had also backed an earlier round), Jane Street, and Blackrock, with a significant chunk of that money guaranteed to go towards NVIDIA GPUs. NVIDIA also participated in Firmus’s previous $300m round, although was not listed as a “cornerstone investor.”

Earlier this year, Firmus secured a $10bn debt facility, led by Blackstone. NVIDIA will be a net beneficiary of that debt raise, and I would argue that its participation in the company’s fundraising — as well as the various announcements of partnerships between the two — has been instrumental in both the company’s fundraising and its ability to secure debt.

Sidenote: According to an AI industry insider interviewed by AlphaSense, Nebius was experiencing financial difficulty — the existential kind — and was saved by NVIDIA, which swept in and offered it access to hardware under a revenue sharing model. The insider also notes that neoclouds hate said revenue sharing agreements, because they tend to stack the deck in NVIDIA’s favor.

You’ll notice I haven’t mentioned “AI” or “LLMs” up until this point, and that’s because technology has, for the most part, very little to do with these transactions. As I discussed in this week’s free newsletter, 70% or more of hyperscaler revenues are from OpenAI and Anthropic, and CoreWeave’s largest customers are Microsoft (for OpenAI), Google (for OpenAI), Anthropic, NVIDIA itself, and Meta. Customers are not coming to it for any particular technological moat or unique offering outside of its ability to sling more NVIDIA GPUs to the same customers that everybody else has.

While GPUs technically are used for AI training and inference, their relationship to NVIDIA is only as good as their ability to create more hype. As I discussed a few weeks ago, it has promised somewhere between 10x and 25x “operating cost savings” with every successive generation of GPUs, though it’s never really clear how that manifests or what it actually means, or whether any of that even matters to OpenAI and Anthropic, its largest customers by proxy.

Nevertheless, it’s pretty difficult to work out what each generation really changes. SemiAnalysis claims it “delivers 5.4x performance per MW and 5x performance per dollar against [the previous generation] GB200 NVL72,” but that’s for DeepSeek R1, a year-and-a-half old open source model that’s vastly smaller and less-powerful.

But that’s not really a problem, because all NVIDIA needs to do is keep up the appearance of innovation in as precise or imprecise a way to justify increasing prices with each new generation, and to convince people that they’re building “AI factories” as they fund data centers for customers that don’t really exist outside of the big AI labs. While NVIDIA has thousands of talented engineers building its GPUs and the associated software, the only real purpose is to create a vague sense of “more” and “bigger” and “more powerful” to justify racks of 72 GPUs that are more than twice the price of their predecessors.

That’s because NVIDIA is no longer a technology company so much as it is an asset management and marketing firm that happens to sell semiconductors. To that point, I believe that the comparisons to Enron, Lucent, and other dot-com flameouts are on the right path, but misses one very, very obvious comparison: GE Capital, the financial services of General Electric, specifically in the Jack Welch years that I covered two years ago in the Shareholder Supremacy.

Welch’s GE did whatever it needed to to survive, buying and selling companies to help boost GE’s earnings every quarter, and eventually grew into what David Gelles would call a “large, unregulated bank,” to the point that GE Capital was at about $425 billion in assets in 2001 (and about 50% of GE’s revenue), providing everything from direct leases of equipment to assuming its customers debts to investing directly in its customers, all to make sure that, well, said customers continued being able to buy GE gear.

Unlike GE Capital, NVIDIA has the advantage of a much, much simpler business model and far fewer products to sell, but said advantage is a problem for two brutal reasons: its customers are driven by desperation and a fear of missing out, and its remarkable revenue growth means that it must in turn grow by ridiculous amounts every single quarter from here to eternity.

Yet this problem is driving it to take increasingly-Welchian measures to make sure that demand keeps up with investor expectations. It (per the FT) just signed leases worth as much as $50 billion for a Texas-based data center built by Hut 8, which makes it likely that this capacity is being built for Anthropic, with which it already has multiple deals. In the same piece, the FT mentions that NVIDIA is in talks to backstop $250 billion in compute costs for a still-theoretical 10GW data center in Ohio.

And again, much like GE, NVIDIA uses its stellar credit rating (AA- - two rungs lower than GE at its height) to secure these deals, per the FT:

“They have the balance sheet to acquire power, and in doing so, ensure their product is deployed,” the person said, asking not to be named.

In the end, GE’s greater collapse led to lawsuits, SEC fines and revenue revisions, all as a result of its “aggressive” accounting practices. For example, it was forced to restate its 2016 and 2017 earnings as a result of “new accounting standards” it instituted as a result of an SEC investigation into its insurance and power divisions that eventually cost it a $200 million fine, cutting a remarkable $4.24 billion off of earnings in the period.

While I’m not accusing NVIDIA of anything untoward, it’s impossible to ignore the sheer aggression of its circular financing and willingness to do whatever it takes to keep selling further GPUs. NVIDIA is now a semiconductor manufacturer, a venture capitalist, a lender of last resort,

Today’s premium newsletter is the story of NVIDIA’s descent into circular madness, and how Jensen Huang is increasingly becoming the Jack Welch of AI.

This is Part 2 of The Hater’s Guide To NVIDIA, or WUDA CUDA SHUDA

2026-08-06 02:41:14

Executive Summary:

As I discussed in yesterday's free newsletter, analyst estimates have OpenAI and Anthropic making up over 70% of all AI revenues across Microsoft, Google and Amazon.

While some might have disagreed, Bloomberg is now reporting that OpenAI "accounted for more than half, and likely about 70%, of Microsoft's actual AI sales during its most recent fiscal year."

Bloomberg's maths is explained as such:

"Bloomberg’s analysis assumes that Microsoft’s annual AI run rate continued growing at the rapid 123% the company reported for March. At that growth rate, the company’s AI business would have tallied roughly $34 billion in the fiscal year ending in June, which can be directly compared with the new disclosure that OpenAI provided $24.1 billion of revenue in that year."

The actual disclosure from Microsoft comes from its most-recent earnings:

For fiscal year 2026, we recorded revenue from commercial arrangements with OpenAI, inclusive of revenue sharing payments, of $24.1 billion, and accounts receivable from OpenAI as of June 30, 2026 was $6.0 billion.

The other incredible fact from these disclosures is that OpenAI's spend and revenue share accounted for 7% of Microsoft's $331.8 billion in FY26 revenue - or around 7.26% to be specific.

At this point, it's impossible to ignore that Microsoft has spent $270 billion in capital expenditures to prop up a single client, and that its overall AI plays have failed to create any significant revenue growth or opportunities.

We are now four years into the AI bubble, and Microsoft has little to show for it other than one very large and very unsustainable company that requires near-infinite resources to keep paying its cloud compute bills.

If you liked this piece, you should subscribe to my premium newsletter. It’s $70 a year, or $7 a month, and in return you get a weekly newsletter that’s usually anywhere from 5,000 to 18,000 words, including vast, detailed analyses of NVIDIA, Anthropic and OpenAI’s finances, and the AI bubble writ large. My Hater's Guides To the SaaSpocalypse, Private Credit and Private Equity are essential to understanding our current financial system, and my guide to how OpenAI Kills Oracle pairs nicely with my Hater's Guide To Oracle, as well as the Hater’s Guide To Oracle (Part 2).

Subscribing to premium is both great value and makes it possible to write these large, deeply-researched free pieces every week. On Friday, I’ll publish the second installment of the Hater’s Guide to Nvidia — where I’ll take a look at how the AI bubble transformed the company from a pure hardware player to a purveyor of the financial dark arts.

If you want to get in touch — and especially if you have any juicy information about Anthropic, OpenAI, or any other companies in the AI bubble — hit me up on Signal at ezitron.76. I’m also on IB on The Terminal.

2026-08-04 23:49:28

If you liked this piece, you should subscribe to my premium newsletter. It’s $70 a year, or $7 a month, and in return you get a weekly newsletter that’s usually anywhere from 5,000 to 18,000 words, including vast, detailed analyses of NVIDIA, Anthropic and OpenAI’s finances, and the AI bubble writ large. My Hater's Guides To the SaaSpocalypse, Private Credit and Private Equity are essential to understanding our current financial system, and my guide to how OpenAI Kills Oracle pairs nicely with my Hater's Guide To Oracle, as well as the Hater’s Guide To Oracle (Part 2).

Subscribing to premium is both great value and makes it possible to write these large, deeply-researched free pieces every week. On Friday, I’ll publish the second installment of the Hater’s Guide to Nvidia — where I’ll take a look at how the AI bubble transformed the company from a pure hardware player to a purveyor of the financial dark arts.

If you want to get in touch — and especially if you have any juicy information about Anthropic, OpenAI, or any other companies in the AI bubble — hit me up on Signal at ezitron.76. I’m also on IB on The Terminal.

Soundtrack: Tool - Forty Six & 2

The question I want to ask anyone reading this who might have invested in or in some way backed the hyperscalers and the greater AI industry:

What is it you think you’ve gotten yourself into? Because I think you’re being sold a lie.

Last week’s tech earnings saw outlet after outlet claim that Amazon, Google, and Microsoft’s AI bets were “paying off” as their respective cloud segments reported record revenue growth, casually ignoring that none of them have broken out their AI revenues. To add insult to injury, Microsoft decided, after sharing that it had a $37 billion AI run rate (about $3.08 billion a month) in Q3 FY2026, that it simply didn’t have to share anything about its actual AI payoff in Q4, realizing that its overall numbers would beguile reporters and analysts — especially those with little interest in what was actually going on as long as the topline stuff looked good.

To be clear, all three of these companies’ cloud platforms have many other customers paying for many other things other than generative AI services or AI GPUs, and they’ve all engaged in a combination of multiple outright price increases and changing their core subscriptions to force AI features on them as a means of boosting revenues and conning the street into believing that “AI is paying off” every time they non-consensually thrust it on their customers, framing higher prices as “better value” in a way that fucks the user to appease Wall Street.

Yet the biggest con of all is that a vast majority of this revenue growth comes from the compute spend of Anthropic and OpenAI, both of whom account for the vast majority of AI revenues and overall cloud growth we’ve seen in the last few years.

Every publication you read right now will tell you that AWS and Azure and Google Cloud are growing like wildfire as a result of the hundreds of billions of dollars they’ve invested in AI GPUs and data centers, when the truth is far simpler: their revenues are being buoyed by two unprofitable, unsustainable AI labs that cannot exist without being funneled tens of billions of dollars each year.

And a decent chunk of that money is coming from the hyperscalers themselves. In the last seven months alone, Google has sunk $10 billion (and up to $30 billion more) into Anthropic, with Amazon funnelling $5 billion to Anthropic within a week of that investment and a total of $50 billion into OpenAI. For all the concern about circular financing in the AI world, it’s astonishing that so much attention has (rightly, to be clear) centered on NVIDIA’s backstopping and funding of neoclouds, and less on the fact that hyperscalers are propping up their now biggest customers, giving them cash that will eventually migrate back to the hyperscaler.

I’d also argue that the vast majority of their capex exists to support these two load-bearing failsons. A few months ago, a Microsoft executive told the judge during the Musk-Altman trial that its OpenAI relationship had cost it “over $100 billion,” including both the $13 billion it sunk into the company and the associated infrastructure.

Microsoft has dedicated its Fairwater data centers (however much actually exists) entirely to OpenAI, much like Amazon has for Anthropic with however much of its massive Indiana-based Project Rainier has actually been turned on, and much like Google is in talks to backstop a $15 billion data center project for Anthropic, along with data centers with Cipher Mining and TeraWulf and a $35 billion private credit-funded Broadcom-backstopped deal where Google will sell Anthropic its TPU AI chips, put them in a Google-built data center, and rent them back to Anthropic.

I want to spell this out: when you remove Anthropic and OpenAI’s compute spend, I am not confident that Google, Microsoft and Amazon have much of an AI business.

While many people believe — largely because the big three refuse to break out their actual AI revenues or disclose their customer concentration — that they have AI revenues coming from a diverse set of different customers, the reality is that their largest cloud customers, let alone AI customers, are two companies that can literally not afford to pay them without a near-infinite flow of venture capital or debt.

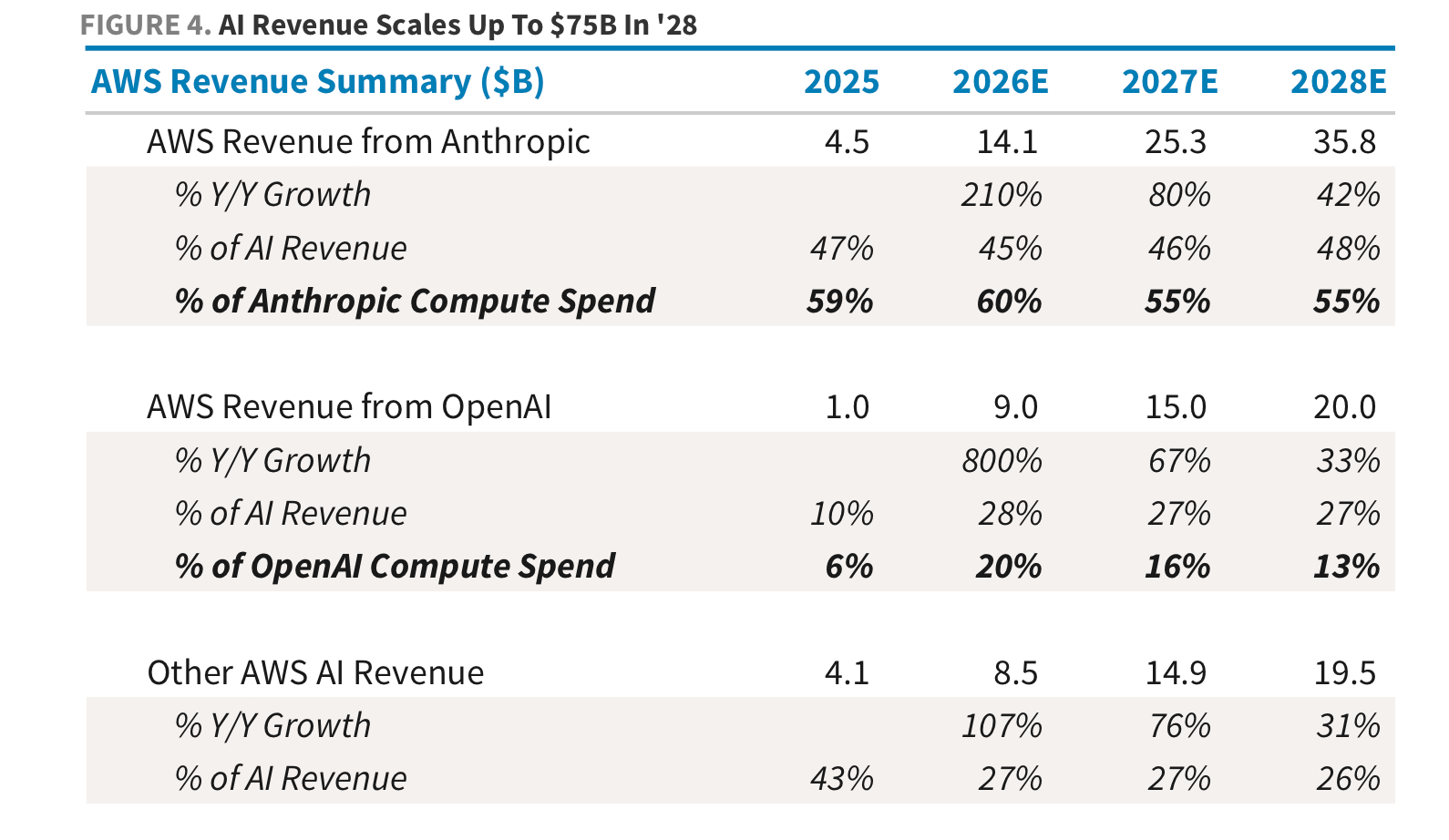

Per Ross Sandler of Barclays, Anthropic and OpenAI are estimated to make up 73% of all of Amazon’s AI revenues in both 2026 and 2027 and 75% of AI revenues in 2028, with Anthropic spending $14.1 billion in 2026, $25.3 billion in 2027, and $35.8 billion in 2028, and OpenAI spending $9 billion in 2026, $15 billion in 2027, and $20 billion in 2028.

Amazon plans to spend $220 billion in capital expenditures in 2026 and even more in 2027, and appears to be doing so almost-exclusively to provide compute for a company that had to raise $95 billion in funding in the space of six months, with $5 billion of that coming from Amazon itself.

Editor’s Note: Just before I headed to press on this piece, I found another note from Stephen Ju (who you’re just about to learn about for the first time) about AWS revenues, with the numbers a little different. He has estimated total AI revenues at around $30.9 billion for 2026, with OpenAI and Anthropic’s compute spend sitting at 59% of those revenues ($18.3 billion) and the remaining $12.6 billion coming from Bedrock, the platform from which Amazon sells access to both TPUs and AI models from Anthropic and (more recently) OpenAI. This revenue concentration improves to 55% in the 2027 estimates.

Anyway, the rest of this piece focuses on Sandler’s numbers, as I did not get a ton of time to dig over these. These numbers, while different, do not meaningfully change my perspective.

As I’ll argue about Vertex, making money by proxy of having monopoly permission to sell OpenAI and Anthropic’s models absolutely counts as revenue related to Anthropic and OpenAI to me. A chunk of both labs’ revenue comes from the resale of these models, easy money that also becomes another way in which hyperscalers feed their revenues back into the AI labs so that the AI labs can spend the money on compute. I will add that Microsoft no longer pays a revenue share to OpenAI.

In any case, the viability, efficacy, and attractiveness of these models are still a product of Anthropic and OpenAI’s ongoing work.

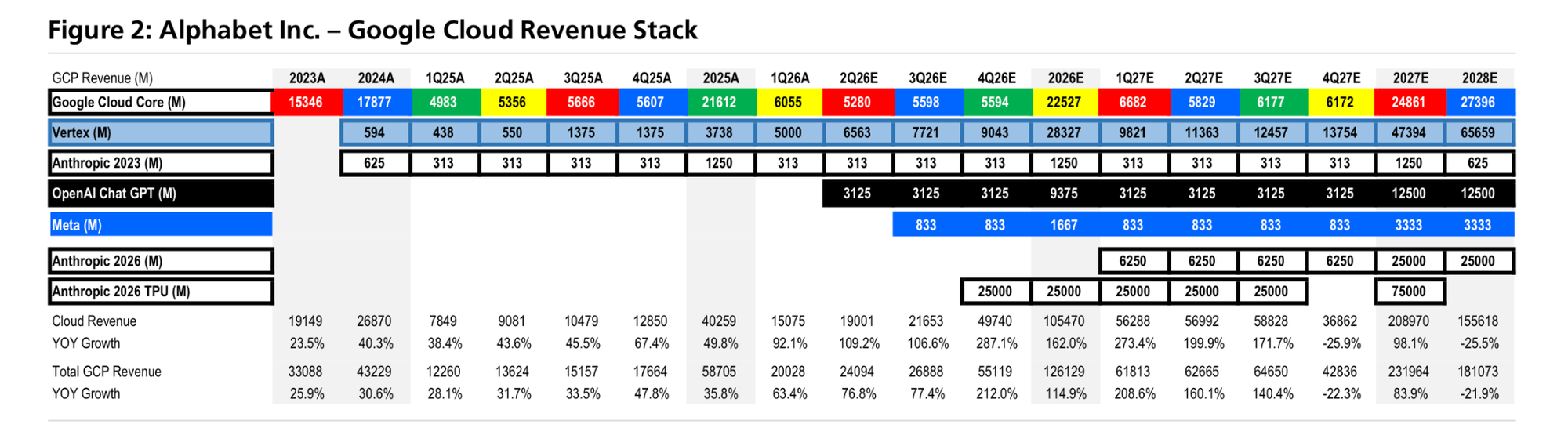

Google is in a similar-position. Per Stephen Ju of UBS, “...Anthropic, OpenAI and Meta will account for 21%, 7% and 1% of 2026 Google Cloud revenues, respectively, and 44%, 5% and 1% of 2027 revenues,” or, put another way, 28% of all 2026 and more than 48% of all 2027 Google Cloud revenues are from Anthropic and OpenAI.

Ju also estimates Meta will make up a whopping 1% of Google Cloud revenues in each year, and does not mention a single other customer, which heavily-suggests that there aren’t really any large ones.

Based on Bloomberg Intelligence’s consensus estimates for Google Cloud’s revenues in 2026 ($105.9) and 2027 ($173.8), OpenAI and Anthropic represent $29.4 billion ($7.4bn/$22bn) in 2026 and $84.69 billion ($8.69bn/$76bn) in 2027. To be explicit here, this is all Google Cloud revenues. It is reasonable to believe that this represents at least 75% of Google’s AI revenue, if not more.

What’s crazy is that these numbers are actually lower than UBS’ estimates. As the chart below demonstrates, OpenAI and Anthropic’s spend is estimated to sit at over $35 billion in 2026, larger than both its entire Google Cloud core non-AI business and Vertex AI model rental business that is largely boosted by Google’s ability to sell Anthropic’s models.

Sidenote: Ju and Sandler appear to disagree on how much of Anthropic’s compute spend that Amazon and Google get, which is fair, because both Google and Amazon separately claim to be Anthropic’s primary provider.

Eagle-eyed readers will also see that Google’s non-AI cloud business is estimated to be effectively flat in 2026, 2027, and 2028.

I also don’t think it’s common knowledge that OpenAI is such a large customer of either Google Cloud or Amazon Web Services, spending at least an estimated $52.5 billion in 2026 and at least an estimated $125 billion in 2027.

In the Musk-Altman trial, OpenAI estimated it would spend $50 billion on compute in 2026, and based on those estimates, that gives us about $16.4 billion across Amazon and Google, leaving a likely $33.6 billion in spend left for Microsoft Azure, though I’ll add that OpenAI continually underestimates its own compute spend and losses.

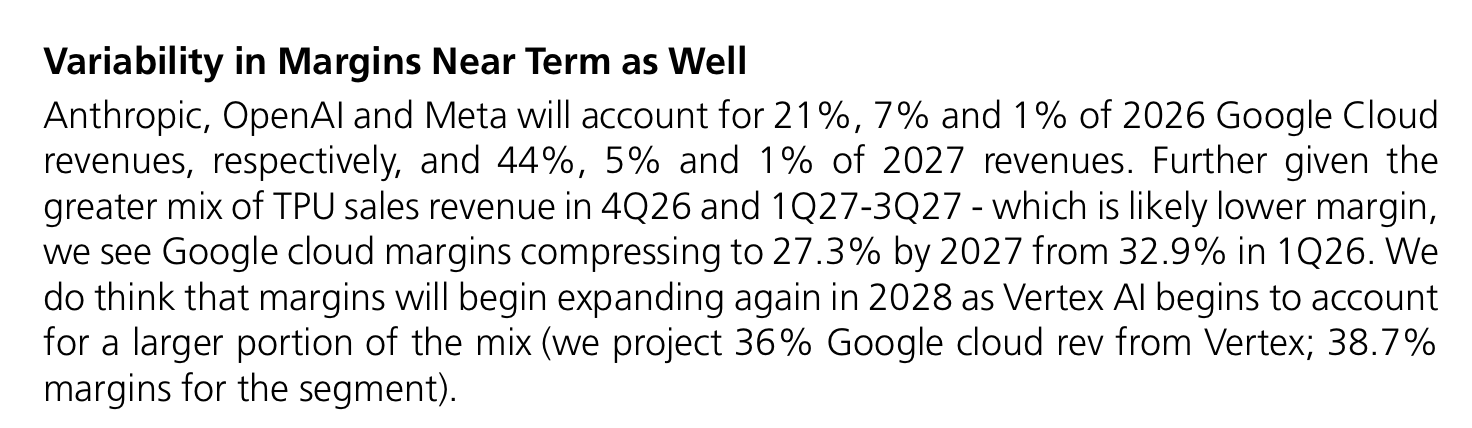

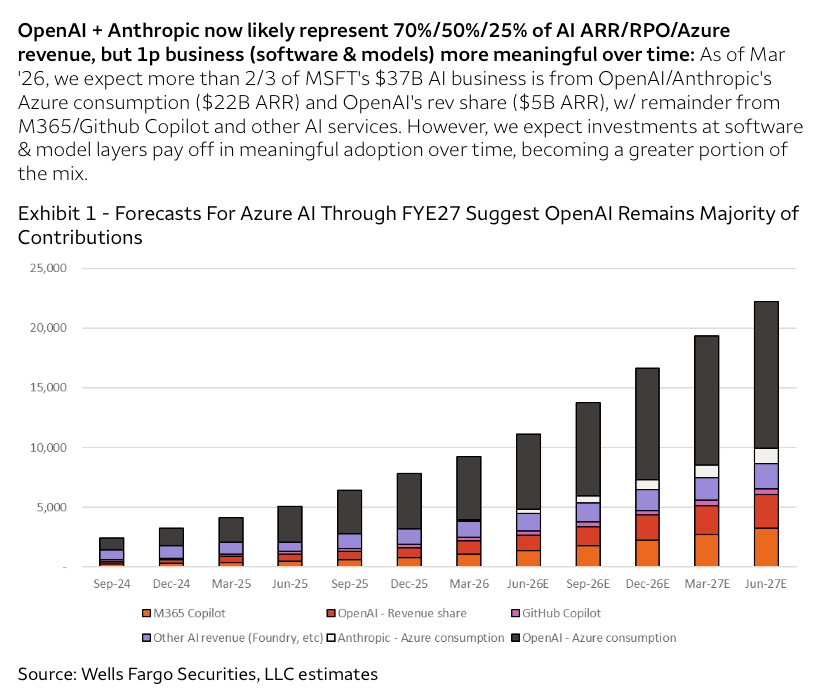

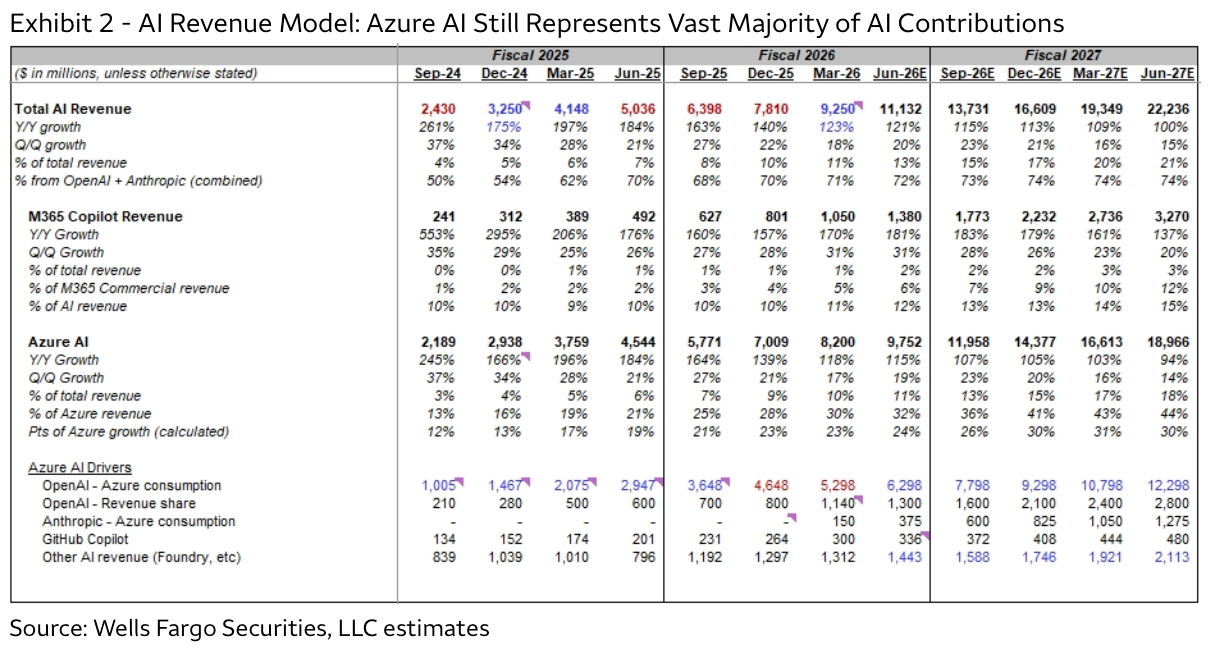

And based on a note from Michael Turrin of Wells Fargo from May 31 2026, things are just as bad for Microsoft, with 70% or more of its AI revenues coming from Anthropic and OpenAI. While Turrin “expects investments at software & models layers [to] pay off in meaningful adoption over time,” it’s difficult to argue that Microsoft has any meaningful AI strategy outside of OpenAI and Anthropic’s compute spend.

To make matters worse, based on Wells Fargo’s estimates, it appears that Microsoft 365’s AI revenues are barely — and I mean barely — beating the revenue share Microsoft gets from OpenAI’s sales.

Wells Fargo also includes a helpful cheat sheet of its estimates for AI contributions, estimating that even at the very end of FY2027 (which began on July 1 2026), OpenAI and Anthropic’s spend will represent a dramatic 74% of all AI revenues. Wells Fargo also estimates that the two AI labs represented 23% of Azure revenue in FY2026, growing to 35% in FY27.

Considering Azure grew 41% year-over-year, this means that 40% or more of Microsoft Azure’s growth came from them — and remember, Azure sells far more than just AI services.

This is an absolute fucking scandal.

The vast majority of Microsoft, Google and Amazon’s AI revenues and revenue growth in their representative cloud platforms are from Anthropic and OpenAI, and they are blatantly, unashamedly misleading investors by not disclosing that this is the case. We’re talking 73% of AWS’ AI revenues, 74% of Microsoft’s, and likely 70%+ of Google Cloud’s considering that just Anthropic and OpenAI’s AI spend is expected to be more than 48% of all cloud revenues.

This is not me being a hater, a skeptic, or a doomer, but the product of actually investigating what’s happening in the real world rather than just looking at whatever numbers the hyperscalers fart out and assuming it’s “all from AI,” and that “AI” means something more than just the two main model labs.

Investors in Amazon, Google and Microsoft have been led to believe that the $994 billion spent on AI GPUs and data centers exists to boost their existing businesses and build what amounts to the next industrial revolution. In fact, this is the line that just about any AI bull will give you about NVIDIA’s GPU sales — that all compute will be used because there’s endless, insatiable demand.

Well, other than the fact there isn’t.

What hyperscalers have actually done is demolish their free cash flow and purchased hundreds of billions of dollars’ worth of GPUs, TPUs, and XPUs to support a customer base dominated by two customers that are now accounting for the vast majority of their revenue growth and quite literally cannot afford to pay their bills without a near-infinite flow of venture capital investments.

Based on these estimates, these analysts also don’t seem to believe that any other large customers are going to emerge, bringing into question both the rationale of their capital expenditures and those of basically anyone building any data center anywhere in the world.

This is all very important, so I want to spell it out really simply for you:

Remember: Microsoft Azure, Google Cloud and Amazon Web Services represent a large chunk of all global cloud spend and AI compute, and thus are a representative sample of all AI compute…and if diverse, “insatiable” demand existed, it would be represented in these estimates.

Sidenote: For the sake of clarity and transparency, Microsoft’s Amy Hood noted in the most recent earnings call that 90% of all cloud spending came from outside the two main frontier AI labs.

The problem is that "cloud revenue," in this case, encompasses a lot of things, including (but not being limited to) "Microsoft 365 Commercial cloud, Azure and other cloud services, the commercial portion of LinkedIn, and Dynamics 365."

With that being said, the fact that frontier spending is just 10% of cloud revenue doesn’t tell us anything — and is arguably a way of obfuscating how dependent Azure is on the two main AI model labs.

This is the single-worst capital misallocation in the history of business. Every single story you’ve read about the “incredible growth” of these cloud platforms is an embarrassing misread of three companies that are misleading investors that will more than likely be forced in the next year or two to have to restate revenues, cut remaining performance obligations, and admit that they’ve drastically overbuilt capacity.

The counterargument to my warnings is always that “this is useful infrastructure that will be used in the future,” or that we’re in an OpenAI Bubble not an AI bubble (which, I argue, is basically the same thing), but when you remove Anthropic and OpenAI, Amazon Web Services and Google Cloud go from exciting growth-engines to chernobyls of capital expenditure.

Without these two “startups,” AI revenues are catastrophically small — for example, Sandler estimates that Amazon Web Services will make a pathetic $8.5 billion in AI revenues in 2026, or roughly 25 times less than the $220 billion Amazon intends to spend this year. While Ju estimates that Google Vertex AI model platform (which is one of the main ways that large enterprises integrate Anthropic’s models) will pull in $28.3 billion in 2026, that’s still a little under $10 billion less than the $35.6 billion that Anthropic and OpenAI will spend on compute.

This needs repeating. Investors and the general public are being lied to. When you remove OpenAI and Anthropic, Amazon, Google and Microsoft’s capex has likely accounted for very little revenue growth, which means that if either or both of them die, the majority of capital expenditures and debt raised as part of the AI bubble have been a waste.

So, let’s go look at the non-Anthropic/OpenAI part of that Barclays note, with each column representing 2025, 2026, 2027 and 2028, with the last three being estimates.

For some context, in the year 2025, Amazon spent $131.8 billion in capex, or roughly 32 times Barclays’ estimates for non-OpenAI/Anthropic revenue — a number that barely improves with the full total ($9.6 billion) to 14 times.

If Amazon has its druthers and invests $220 billion in total capex in 2026, the (pathetic) $8.5bn in non-OpenAI/Anthropic revenue will be roughly 26 times smaller, or 7 times smaller when you use the full $31.6 billion in projected AI revenue for 2026.

If your counterargument here is that “the gap is getting smaller each year,” you are a mark. $31.6 billion is $22.6 billion less than Amazon spent on capital expenditures in its last quarter, or roughly $18.4 billion less than it invested in OpenAI this year. Barclays’ estimates for 2028 have Amazon’s AI revenues — 75% of which are from OpenAI and Anthropic’s compute spend — at around $75 billion, four god damn years into the AI bubble.

Amazon will have, by 2028, likely sunk over $650 billion in capital expenditures into AI, all to earn (and this assumes OpenAI and Anthropic exist and can pay) a little over $171 billion in AI revenue, with the vast majority of it contingent on two entirely venture-backed startups.

Similarly, even if UBS’ estimates come true, Google will have spent roughly $408.5 billion (including consensus estimates of $120.5 billion for the rest of the year) in capital expenditures to create an AI business that makes about $80 billion a year, with most of that coming from either selling Anthropic’s compute or access to its models via Vertex.

Microsoft is in the same position. Wells Fargo’s estimates have its AI revenues for FY2026 (which just ended) at around $34.5 billion, in a year where it spent $115.9 billion in capex, with $41 billion of that in the last quarter, or roughly $6.5 billion more than its entire estimated AI revenues for the god damn fiscal year.

I realize I’m being a little repetitive, but I need you to see that without OpenAI and Anthropic, Microsoft, Google, and Amazon’s AI revenues are absolutely pathetic, and are thus entirely-dependent on their compute spend.

Let’s be serious, and take the absolute kindest read of UBS’ estimates, saying that Google’s Vertex AI platform will make approximately $22.5 billion in annual revenue, and assume, wrongheadedly, that it’s not near-entirely made up of demand for Anthropic’s models…

…

Sundar Pichai, did you spend $288 billion god damn dollars to make an annual business that makes less revenue than YouTube? We haven’t even talked about margins or costs or whether any of this is actually profitable, largely because it’s immaterial, as there is absolutely no way to read this situation as anything other than a historic failure!

Andy Jassy, is that you? Get your country ass over here! You did NOT just go out there and spent $429.5 billion god damn dollars to stand up data centers for a pair of companies you have to literally hand the money to them to pay you, did you? I’m gonna tell momma Jassy what you’ve been up to! She’s gonna paint your back porch red!

Wait, what’s that?

You just gave OpenAI $35 billion dollars? Wasn’t that dependent on it going public or reaching AGI? Are you kidding me man? It’s almost as if you realize that the only way your largest customers are gonna pay y’all is by giving them the money to do so!

Okay, all jokes aside, there’s very clearly a problem here with AI demand, in the sense that it doesn’t really exist without hyperscalers paying themselves to do so.

When you look at these numbers, you see a brutal story of unproductive capex. Looking at Wells Fargo’s estimates, it doesn’t appear that Microsoft 365 Copilot is a meaningful business, hitting a meager estimated $3.859 billion for the entire fiscal year 2026 for a product that allegedly has 30 million paid seats, suggesting massive discounts and questionable value.

Wells Fargo estimates it’ll grow to an unremarkable $10 billion in annual revenue in FY2027 — barely more than OpenAI is estimated to spend in Q1FY2027.

Very Blunt Sidenote: if Microsoft is struggling to sell AI-powered software attached to the literally-most-used enterprise software in the world with a sales team of tens of thousands of people and tens of thousand more resellers, how do you think that the rest of the AI software world is going to do long term?

To be explicit: the demand for AI-powered software is not there, and neither is the demand for selling AI-powered add-ons to other software.

This is an embarrassing accident of an industry with two ticking time bombs underneath it.

There’re really two scenarios:

And, to be explicit, the last part of that sentence is exactly what’s going on. Microsoft, Google and Amazon are have spent over a trillion dollars in capex and equity investments specifically so they can create growth engines that are entirely-dependent on Anthropic and OpenAI, who are entirely-dependent on Microsoft, Google and Amazon to either (or both) feed them money or continually build them more infrastructure.

Sidenote: I haven’t even mentioned how Google’s $99 billion and Amazon’s $53.4 billion in profits were inflated by their stakes in Anthropic (and SpaceX, in Google’s case), because I could write an entire newsletter about how deceptive and ridiculous it is that GAAP allows companies to do this. We need new regulations, and we need them urgently, as investors are being misled.

However you feel about what I’m saying, these estimates also require OpenAI and Anthropic to keep growing at the rate necessary to keep up with expectations for Amazon Web Services, Microsoft Azure and Google Cloud.

The most important question is which part of the machine breaks first.

The wind cannot fall out of the sails OpenAI and Anthropic, as both of them have to keep pace to be able to pay for all this data center capacity, which would mean they would, across Amazon and Google alone, have to produce over $125 billion in 2027, which would require both the actual demand (from customers for inference and for training) to use that much compute and the means to pay for it (from venture capital and the hyperscalers themselves).

Sidenote: To give you some context about how large that amount of money is, Microsoft just announced that its entire fiscal year 2026 revenue for Azure was $100 billion.

For this to be possible, both the demand for access to OpenAI and Anthropic’s models and the money to pay for the inference to serve it must be there to realize these revenues and to keep Google Cloud, Microsoft Azure and Amazon Web Services growing at historical rates.

To even have a shot at doing that, compute capacity must come online fast enough, which is an open question in and of itself. As I covered a few months ago, AI data centers are some of the single-most ambitious construction projects in history, requiring massive amounts of capital, specialist talent, and materials, and execution that includes building decades’ worth of power infrastructure in a few short years, making them take anywhere from 18 to 36 months to complete. If capacity doesn’t come on fast enough, OpenAI and Anthropic can’t pay for it.

It seems very possible that the only reason growth hasn’t stumbled for Microsoft, Google, and Amazon is OpenAI and Anthropic’s compute spend and the ability to sell access to their models, which means that they may see their capital expenditures as existential.

It kind of makes sense. If they fail to build more and more data centers and continue to sink money into Anthropic and OpenAI, growth will slow across both their cloud platforms and associated services, as the two AI labs are the only real aggressive purchasers of AI compute, which makes up the vast majority of hyperscaler AI revenues.

It’s a dangerous game. Without OpenAI and Anthropic, it’s clear that the underlying businesses of the big three hyperscalers are deteriorating, and that their AI plays are a catastrophic failure, because the sheer amount of cash they’ve required to date (and the even greater pile of cash they’ll need in the months and years ahead) demands an outsized return for years to come.

Apparently things are so dire that the only way to patch over slowing growth was to fund two giant startups beholden to massive compute contracts that feed venture capital dollars to hyperscalers in a circular motion that mostly equates to eating poisoned cardboard.

Things look great right now, as long as you avoid thinking too hard about what it means that so much of this revenue growth is coming from Anthropic and OpenAI, and that their other AI plays are producing the lowest end of double digit billions of revenue for something that has cost them over a trillion dollars, their free cash flow, and burdened them with hundreds of billions of dollars of debt, along with off-balance sheet liabilities now totalling over $1.35 trillion (including Meta).

I can already hear the counter-argument that “Anthropic and OpenAI are the fastest-growing companies in history,” and I certainly hope you’re right, because there does not appear to be anyone else who wants to buy compute at their scale other than hyperscalers selling it to them and whatever weird also-ran bullshit Mustafa Suleyman, Demis Hassabis, and Alexandr Wang will be allowed to do until one of the CEOs tries to make them the fall guy.

I really need to be as clear as possible: the current consensus view on AI is entirely divorced from reality. Based on what I’ve shared with you today, it is ridiculous to suggest that hyperscalers are building data centers under the belief that they will make a lot of money or that demand exists. They may believe — or hope — that’s the case, but that doesn’t make it true.

Outside of OpenAI and Anthropic, there appears to be less than $30 billion dollars of non-AI lab compute demand across Amazon, Google and Microsoft. I need to also be clear that this is almost certainly an overestimate, because it includes revenues from Azure Foundry, Amazon Bedrock, and Google Vertex, which includes both compute and API spend on Anthropic and OpenAI’s models.

This means that we are likely overbuilding data center capacity at the scale of hundreds of billions of dollars. As the largest providers of AI compute with the most experience and the biggest brand recognition, it’s hard to argue that there’s pent-up AI demand waiting elsewhere that hyperscalers haven’t realized. If anything, it suggests that everybody else is completely and utterly fucked.

Perhaps you’ll argue that the analyst was wrong or that my analysis is wrong or that demand will magically appear, and you’re welcome to if you want to continue burying your head in the sand.

Let me spell it out for you: if Anthropic and OpenAI each had a run rate of $100 billion, they would still not have the scale to generate the compute demand to cover what their commitments are to Microsoft, Google, Amazon, and, of course, Oracle.

And CoreWeave. And Cerebras. And Cipher Mining and TeraWulf. And IREN. And Nebius. And Broadcom. And AMD. And SpaceX. And maybe Meta, SB Energy, and whoever might build a $30 billion data center in Georgia. While some of these — like Cipher, IREN, Nebius and TeraWulf — will flow revenue directly to Google Cloud or Microsoft Azure, there’s still tens of billions of dollars’ worth of compute revenue that needs to get paid somehow above and beyond OpenAI and Anthropic’s spend on the major platforms.

This is not sustainable. In fact, it’s pretty fucking awful.

Let’s also be blunt about something: neither OpenAI nor Anthropic have worked out their business models. You can fart around claiming that Anthropic was profitable (it wasn’t) for a single quarter or repeat theoretical mantras about “positive gross margins” or say “they can just stop training” all you want. These companies lose tens of billions of dollars, they are horrendously unprofitable, an[d at this time do not have an actual answer to “how do these businesses function without infinite resources?”

Even if they were somehow profitable — which they are not! — they would still need to grow at an impossible rate. Putting aside all of the estimates from this piece, OpenAI projects to spend $750 billion in compute in the next three-and-a-half years, which either means it will need to grow its revenue to hundreds of billions a year very soon or raise half a trillion dollars or more over the next few years, at a time when even hyperscalers are having trouble raising that much money.

And based on both these estimates and the massive amounts hyperscalers are spending on capex, I think they’re well aware that there isn’t diverse demand, and that the only path forward is to continue building capacity specifically for OpenAI and Anthropic, funding them in whatever way possible — either through backstopping the compute costs or helping organize massive private credit deals — to make sure that revenue growth never slows.

This is a doomed mission.

These estimates show that Microsoft, Google and Amazon do not have meaningful AI business outside of the ones they’ve incubated, at least not ones that will pay off their capital expenditures. Consensus estimates for Microsoft’s FY2027 capex are around $186 billion in a year where its non-OpenAI/Anthropic AI revenue is expected to be $18.7 billion, meaning that even if these services had 100% net profit margins (IE: zero costs), it would take a decade of those revenues to pay back the capex.

While you might argue this is unfair — especially as OpenAI and Anthropic are unlikely to die before the fiscal year ends — it is time to start seriously discussing what happens to hyperscaler revenues once they do so.

Put another way, investing in Microsoft, Google, and Amazon as part of the AI trade is an investment in Anthropic and OpenAI’s ability to both survive and grow to become companies of comparative size and revenue growth as their hyperscaler progenitors.

It is clear based on the estimates I’ve shown today that the vast majority of growth in AWS, Google Cloud and Microsoft Azure comes from two companies that can literally not afford to pay their bills.

Jensen Huang has said that he has visibility into $1 trillion in GPU sales through the end of 2027, or, as I estimated, about 40GW of compute capacity requiring $435 billion in annual revenue. Though these estimates do not specifically break out compute demand from Bedrock, Foundry or Vertex, the combined AI revenues — including Anthropic and OpenAI’s compute spend, all API spend run through the platforms, and Microsoft 365 Copilot — for their fiscal years 2027 sits at around $304 billion, with the vast majority of that (around $197 billion) coming from AI lab compute spend.

There is not enough demand. We are overbuilding data centers. If compute demand existed to justify the amount of data center capacity being built — or even close! — then analyst estimates for AI revenues would be both significantly higher and meaningfully diverse rather than centralized around two unprofitable, unsustainable companies.

To be specific, for any of this to “make sense” we’d need to see multiple different companies or groups of companies spending comparable amounts to OpenAI and Anthropic, dramatic amounts of revenue generation from Google Workspace and Microsoft 365, and revenue diversity driven by multiple customers spending billions or tens of billions of dollars at the very least in estimates for 2028.

It’s also likely much worse than I’m explaining because of how the big three bundle every single imaginable AI service inside Foundry, Bedrock, and Vertex, all of which blend direct GPU rentals with API spend on models from Anthropic and OpenAI, which I believe generates a large majority majority of revenue on these platforms rather than diverse interest in renting AI chips or other models.

Microsoft, Google, and Amazon are selling their investors a lie about their AI strategies, and in a properly-regulated market would be forced to file investor disclosures that document the heavy revenue concentration of Anthropic and OpenAI’s compute spend.

In not doing so, they continue to mislead investors and the general public into believing that hyperscalers are funding the next great growth engine in tech, when what they’ve actually done is spend a trillion dollars in capex and investments to make tens of billions of dollars of revenue, much of which came from their own equity investments.

And in doing so, these hyperscalers have mangled their balance sheets, tripling their PP&E, encumbering themselves with over $500 billion in data centers and GPUs that exist mostly to support two companies that can’t afford to pay their bills long term. At the end of this hype cycle, Microsoft, Google and Amazon (and, I guess, Meta) will have left themselves in a much-worse condition than before, with revenue expectations that are overwhelmingly inflated by two unsustainable companies.

As I wrote in the Rot-Com Bubble two years ago, these companies are fundamentally out of hypergrowth ideas, and these analyst estimates confirm my absolute worst fears about the condition of these companies.

AI is not working. A $10 billion or $30 billion-a-year business is not sufficient to justify either the massive capital expenditures or scars on hyperscaler balance sheets. In fact, it’s kind of hard to imagine what that might actually be at this point, because Google, Microsoft and Amazon continue to spend somewhere between $170 billion and $230 billion a year in capital expenditures, and each time they do so, they increase the size of the payback necessary.

Sidenote: I’ve seen a note floating around Twitter from Bank of America that claims there’s $2.3 trillion in backlog across “the top 4 CSPs,” referring to Amazon, Google, Microsoft and Oracle.

Before anyone makes any vivid assumptions about these numbers, know that they refer to literally every dollar of incoming revenue for these companies, including long-standing compute deals, Oracle’s database contracts, and at least (per The Information) $1 trillion in commitments from OpenAI and Anthropic, though remember that we do not actually get a breakdown of RPOs based on segment, company, or related terms around cancellation or amendment.When companies tell you their RPOs, they do so so you’ll believe the revenue is diversified and, ideally, about whatever hype cycle they’re currently focused on (like AI!), which is exactly what’s happening with basically anyone covering them.

Let’s break down when they’ll be realized!

Microsoft: 30% — around $203 billion — will be realized in the next 12 months, for a company with over $300 billion a year in revenue.

Oracle: 12% — around $76.6 billion — will be realized in the next 12 months, for a company with around $62 billion in annual revenue.

Google: 22% or so within the next 24 months, or around $115 billion for a company with over $400 billion in annual revenue.

Amazon: Amazon doesn’t disclose, but it has a backlog of $496 billion, with at least $238 billion of that from OpenAI and Anthropic, and annual revenues of over $700 billion.

At this point, AI would need to become — and this is without OpenAI and Anthropic — a business at the scale of Amazon Web Services ($170 billion, though this number is inflated by OpenAI and Anthropic’s compute spend), Google Search ($200 billion), or at the very least Azure ($100 billion, again inflated by both AI labs’ compute spend) to make sense, and even then, for this to make sense, hyperscalers would have to stop spending money on capex.

Put another way, AI bets cannot “pay off” if hyperscalers continue to funnel three or more times their AI revenues every single year into capital expenditures.

Sidenote: If I had to guess the rationale at this point, it’s that OpenAI and Anthropic have signed up for massive amounts of compute capacity that has yet to be built or invested in, putting hyperscalers in a vicious circle where they must spend more capex to earn revenue from companies that they also must keep alive through either backstops or outright equity investments.

I haven’t even gotten into the other vicious cycle — that the more of these data centers hyperscalers build, the more expensive they become thanks (at least, in part) to the skyrocketing costs of memory that continue to increase primarily because hyperscalers keep buying servers for their AI data centers. As discussed last week, this only increases the amount of debt they’ll need at a time when the market is getting increasingly nervous about AI data center debt.

Yet as we speak, the market is ripping, because hyperscalers have swindled investors, the media, and even the analysts themselves. Article after article after article claims that AI bets have “paid off” because these companies are glazed any time they inflate their earnings using the compute spend of two unstable and unsustainable companies, in part because hyperscalers both refuse to and face no pressure to share their AI revenues, knowing that they’ll get credit as long as the topline numbers look good.

I want to be clear that the air is coming out of these companies, no matter how good these earnings may look.

Everybody is taking the growth of their existing businesses and two AI labs’ compute spend as proof that all this capex is paying off, even though there is now consistent proof that the direct opposite is happening, and that their businesses are becoming increasingly-dependent on that compute spend.

I understand that nobody really wants to think about the logical endpoints of what I’m arguing, so I’m going to do it for them.

To put things really simply, Anthropic and OpenAI are a way that hyperscalers can feed their revenue to themselves by spending money on capex, backstopping compute contracts, or doing direct equity investments.

Their continued existence allows the AI bubble to continue inflating, but this can only continue as long as venture capital and hyperscalers are capable or willing to invest. There is simply not the demand — not from open source, not from other AI labs, not from self-hosting, not from anywhere — to justify the capex or the massive data center buildout.

And for those arguing that there would be a dot-com bubble recovery story, I must be clear that if there isn’t demand today, it won’t magically appear tomorrow. AI GPUs will cost just as much to run in five years as they do today, as will unfinished data centers cost just as much to finish, as will electricity remain expensive, and all this will be happening after it’s easy to raise venture capital to actually buy the compute.

To quote my buddy Kasey, every major cloud compute provider is solely standing on OpenAI and Anthropic.

OpenAI and Anthropic are time bombs, and when either of them explodes, everybody will ask why we didn’t see the brutality that follows coming.

The truth is that nobody wanted to look.

To stare at these numbers and reconcile with their meaning is to acknowledge that the current state of the tech industry is based on mania, deceit, circular financing, and outright cons, and that the ascent of NVIDIA was primarily driven by three companies building compute capacity for two unsustainable companies that became existential to their growth, inspiring hundreds of billions of dollars of waste by obfuscating how little real demand existed.

I realize it’s difficult to think about scary things, and how easy it is to dismiss me as a doomer or a catastrophist, but mine is a logical and rational argument in an era poisoned by hype and grifting at a scale unseen in history.

The greatest lie of this era is that the tech industry is building the next industrial revolution, when what they’re actually building is a monument to everything that’s wrong with modern capitalism — wasteful expenditures disconnected from any real benefits generated as a means of pursuing growth at all costs, setting up a collapse that will tear a hole in the tech industry and the markets, and leave the world full of half-built monoliths sold to local communities as job creators.

The fact we’re talking about compute futures is a joke. The fact we’re talking about AI factories is a joke. Almost every aspect of the AI bubble is a joke, and in the end, investors and the general public will be the punchline. The rich will have gotten richer, the banks will have harvested fees, the hedge funds will have traded and taken profits, the private credit funds will have gotten their fees, and anyone who didn’t have an active inside track will be fucked.

All of this could’ve been avoided, but the world has a cult-like obsession with the wealthy, believing that the CEOs of the largest companies in the world could never make a bad decision, and that any executive is automatically smart by virtue of being rich and powerful.

And oh, how silly that’ll look in retrospect.

If you liked this piece, you should subscribe to my premium newsletter. It’s $70 a year, or $7 a month, and in return you get a weekly newsletter that’s usually anywhere from 10,000 to 18,000 words, including vast, detailed analyses of the biggest events and companies in the AI bubble.

2026-07-31 23:53:49

A great deal of the discussion of the so-called benefits or problems with AI comes down to the theoretical jobs that are (or are not) lost as a result of things LLMs can (or cannot do), or the equally theoretical productivity benefits that’ll come from using LLMs in place of (or in conjunction with) humans.

Anthropic’s Economic Index and OpenAI’s Economic Research Exchange are marketing operations that exist to propagate the (wrongheaded) belief that LLMs are either leading or will soon lead to massive economic or productivity shifts, even though little or no actual evidence exists to show that this is the case, other than the occasional story about LLMs make people worse or slower at their jobs or single lines in studies that are used (incorrectly) to prove that “AI is making it harder to find a job for young people.” In fact, Anthropic’s Head of Economics recently said there was “no material increase in the unemployment rate to date.”

These conversations materially detract from the actual harms or effects of AI, and exist only to make you scared that AI will take your job. They do not have any vested interest in expressing the actual economic effects of AI, which are, at this point, a simmering cauldron of different speculative bets on whether or not LLMs — a definitively niche technology — will create or become general-purpose software (per Roger MacNamee) that scales into the next Google Search, iPhone, or Microsoft 365.

As I’ve argued again and again, the AI industry’s revenues are, outside of Anthropic and OpenAI, incredibly small. Even in Exponential View’s deliberately-pro-industry analysis, there’s only around $110 billion in trailing twelve-month revenues across the entire industry, including OpenAI and Anthropic’s cloud spend.

For those counting at home, that’s $12 billion less than the $122 billion OpenAI raised in March, and a full $145 billion less than all AI startups raised combined in the first quarter of 2026.

Anthropic and OpenAI want you to talk about the theoretical so that you don’t focus on the tangible — their hundreds of billions of dollars’ worth of commitments, said commitments effects on the remaining performance obligations of hyperscalers and chip manufacturers, and the sheer scale of venture capital’s investment in AI, which (as I’ve argued in the past) largely allows for massive on-paper gains with little or no hope of liquidity.

To put this bluntly, I believe the entire conversation around AI’s theoretical relationship to jobs to be masturbatory and a conscious attempt to avoid having a messy conversation about the scale of the actions taken based on the flimsily-founded promises of AI labs and hyperscalers.

Today’s piece will dig into the true scale of the money needed to make AI make sense, by which I mean how much OpenAI and Anthropic will need to meet their commitments, how much money hyperscalers will need to pay off their investments, venture capital’s true exposure to the AI bubble, and what will have to go right for the bubble not to be, well, a bubble.

I’ll also make the case that the longer the bubble continues to inflate, the harder the basic economic puzzle of AI becomes to solve, as creating and deploying infrastructure becomes vastly more expensive — meaning that in order to achieve profitability, hyperscalers and neoclouds need to charge significantly more for compute than before, and the only two real potential customers are ones that cannot pay for it.

This will be a more more-pointed newsletter than usual, focusing on hard numbers and harder truths.

Let’s get it on.

2026-07-29 00:29:37

If you liked this piece, you should subscribe to my premium newsletter. It’s $70 a year, or $7 a month, and in return you get a weekly newsletter that’s usually anywhere from 5,000 to 18,000 words, including vast, detailed analyses of NVIDIA, Anthropic and OpenAI’s finances, and the AI bubble writ large. My Hater's Guides To the SaaSpocalypse, Private Credit and Private Equity are essential to understanding our current financial system, and my guide to how OpenAI Kills Oracle pairs nicely with my Hater's Guide To Oracle, as well as the Hater’s Guide To Oracle (Part 2).

Subscribing to premium is both great value and makes it possible to write these large, deeply-researched free pieces every week.

Soundtrack: Queens of the Stone Age — Infinity

Two years ago, NVIDIA CEO Jensen Huang said that “the more you buy, the more you save,” referring to its new (at the time) Blackwell GPUs that would “reduce LLM inference operating cost and energy by up to 25x.” Two years later, those supposed gains have been pared back to 10x, based on case studies with private inference providers that do not share their margins and are most-decidedly not profitable, and absolutely nobody seems to mind that NVIDIA overstated the gains on Blackwell (in a vacuum, in specific circumstances) by 150%, partly because these numbers are utterly meaningless, and partly because the media in most cases ardently refuses to criticize this company.

Blackwell being “10x better” than Hopper does not appear to have made any AI startups profitable (or even more profitable), it does not appear to have lowered anyone’s costs in a way that we can measure using dollars and cents, and as a result, I feel very little when I’m told that Vera Rubin provides “up to 10x more tokens per megawatt,” especially as that was with DeepSeek R-1, a year-and-a-half-old open source model.

Nevertheless, all of this is immaterial to the larger problem that none of this appears to have resulted in anything tangible other than horrendously-overstuffed balance sheets and spuriously-puffed stock prices.

Hyperscalers will have sunk over $1.3 trillion dollars into generative AI by the end of 2026, and have plans to spend a trillion dollars more next year. On a very rational level, nothing that large language models (LLMs) have done, do or will do in the future can or will ever bring in the more than $2 trillion (or more) in brand new revenue that will be required to make any of this worth it.

To be more specific, between March 2022 and July 2026, Meta, Google, Amazon, and Microsoft added over $850 billion in property, plant, and equipment (PP&E), nearly tripling their PP&E from $498 billion or so, and in a period where they spent over $1 trillion in capital expenditures.

In that same four year period, none of them have disclosed their actual revenues from AI or AI-related services, and, as of their latest quarters, capital expenditures now represent 24.4% of Amazon’s, 33.7% of Meta’s, 37.3% of Microsoft’s, and an astonishing 43.4% of Google’s revenue, a number that’s steadily increased over the last three years.

They’ve also added over $307 billion in on-balance sheet debt, leaving them with a total of $557 billion, doubled from $250 billion or so in March 2022. I mention on-balance sheet because Nikkei reports that Meta, Google, Amazon and Microsoft have over $1.35 trillion in off-balance sheet debt — either data centers/GPUs yet to be delivered, or debt raised via SPVs that shift the actual “ownership” of them over to another party as a means of making them look less-indebted than they really are.

To be clear, it’s totally fine accountancy-wise to not include leases or commitments yet-to-commence, but it’s very important to know how big an anvil hyperscalers are conjuring above their heads. Google, for example, has $811 billion in contracted future spending commitments as of its latest quarter, increasing by a dramatic $661 billion ($478 billion or so in the latest quarter) in the last 6 months, and Meta has over $237 billion in non-cancellable contractual commitments.

Over $167 billion of that on-balance sheet debt has been raised in bonds across Google, Meta, and Amazon, with its $25 billion bond sale from July receiving (per Bloomberg) a cool reception, with “demand [settling] at 1.6 times the deal’s size…[and to] put that in perspective, US high-grade corporate deals have seen orders average around four times their size this year.”

For some further perspective, per Freedom Broker’s Saken Ismailov, there was around $100 billion of demand for $20bn of Google’s three to fourty-year-long bonds (5x) and around £9.5 billion of demand for its £1 billion 100-year bond sale (9.5x).

As of last week, Google’s century bond has already lost 10% of its value.

This is a problem, as all four are certain to become repeat visitors to the bond markets. Herman Chan of Bloomberg Intelligence estimates that hyperscalers will need to raise $1.5 trillion in investment-grade debt in the next five years just to keep up with their trillions in estimated capital expenditures.

To make matters worse, hyperscaler bonds are, to quote Bloomberg, “...underperforming on almost every metric,” and are “in the red on average,” though that includes Oracle, whose credit just got downgraded to a single rung above junk by S&P Global.

Sidenote: As an aside, whenever you hear bonds are measured in something called “spreads,” it’s how much more an investor would expect to get paid above the current US treasury bond rate in “basis points,” with 100bps referring to 1%.

The thing is, when treasury rates go up, bond prices go down, even though you’re still getting paid on the coupon (the yield, IE: the money it pays regularly) and the payoff at the end of the bond’s life. As a result, spreads exist to tell you how much more or less it pays than an equivalent US treasury bond, or a similar ultra-low-risk government bond.

Bonds are also generally raised in tranches, in different currencies, at different lengths, which makes their prices less useful than you’d think. Furthermore, bonds can be resold to third-parties, and often for cheaper than the original purchase price — which is something that would happen if people started to get worried about the company not being able to pay back its debts.

Let’s give you a (hypothetical) example. US Treasuries are 5%, and a hyperscaler raises $10 billion in bonds at 6.5%.

The “spread” here would be 150bps — which suggests that investors think they’re mostly safe. In general, 150-300bps is worth keeping an eye on, 300bps+ is worrying, and 700bps+ is a company that the market is concerned about repayment. For example, a high-credit company's bonds would have an average OAS of 20-80bps, or an investment grade (like Amazon at 118bps) would have between 80-150bps.

And, well, then there's the rest.

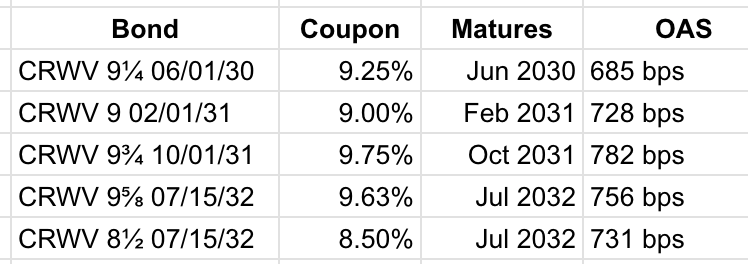

For example, CoreWeave’s $1.25 billion in bonds raised in June 2026 currently sit at an option-adjusted spread of 756bps, despite being issued somewhere around 540bps on the day of issuance. Put another way, bondholders have dumped the shit out of them in the last month and have material concerns that CoreWeave won’t pay. To make matters worse, the average for its bond/credit rating (Ba3) is 200-400bps, meaning the market is really, really concerned about whether CoreWeave pays its bondholders.

All of this is a way of telling, in realtime, how much riskier a bond might be than the rock-solid guarantee of the US government (or whatever currency it was raised in). When I say “option-adjusted spread,” that’s a forward-looking model that strips out things like if a company can recall (IE: buy back a bond early) a bond to give you a generalized spread that tells you how the market feels about a particular bond.

Things can muddle a little bit depending on the company, or should I say one company in particular.

EDITOR'S NOTE: To be clear, this is an edit to the piece, because I wanted to clarify some stuff and the article I previously linked got things wrong.

Also, thank you to eagle-eyed premium subscriber Clayton for noticing!

So, SpaceX's "investment-grade" bonds (issued in late June) are rated BBB - the lowest level possible - and have an average OAS of around 270bps, with the widest spread sitting at 346 (for its 30-year dated bond). I previously linked to a piece that said it was "trading like junk," and I was completely right in that assessment, but didn't give you, the reader, the juice to understand why.

As of writing, the average spread of Bloomberg's Corporate High Yield Index - which, to be clear, is made up of junk bonds in most cases many rating levels lower than SpaceX - is around 282bps. In other words, Musk's "investment-grade" bonds are trading like junk!

As complex as all of this sounds, it’s all pretty simple: hyperscalers have borrowed a bunch of money to fund AI, to the point that it’s pushing them into cash-flow negative territory, and every time they raise more money, bondholders become more worried about them paying it back, especially given that both Amazon and Google have now gone cash-flow negative as of their latest quarters.

Or, put more-simply, the more they raise, the more it costs.

Then there’s the other, more-obvious problem — the more they buy, the more they spend.

As I wrote in the Hater’s Guide To The Memory Crisis, the sheer scale of Microsoft, Google, Meta and Amazon’s spend on AI data centers has led to a massive supply chain crisis and price-gouging from the triopoly of Micron, SK Hynix and Samsung, with Micron alone bumping prices for DRAM by 60% in its last quarter, shooting up the price of every single kind of RAM possible, at a rate increased by the amount of GPUs and servers that hyperscalers buy.

To give you a sense of how memory hungry AI is, single 72-GPU GB300 NVL72 AI server has over 20 terabytes of high-bandwidth memory (used almost exclusively in GPUs and other AI chips), and 17 terabytes of the LPDDR5X RAM used in mobile devices, and a gigawatt data center has thousands of those NVL72 servers (or something similar). Moreover, that high-bandwidth memory that AI GPUs use requires more wafer space during manufacturing — further reducing the amount of manufacturing capacity for other kinds of memory.

This naturally creates a vicious cycle. The more AI servers that hyperscalers buy, the more demand they create for RAM and high-bandwidth memory, which increases the price of RAM and HBM, which makes the AI servers more expensive, which means hyperscalers need more money, and because AI has yet to provide meaningful improvements in revenue or cashflow, they’re forced to raise more debt.

The more they raise that debt, the more expensive that debt becomes, and the more of that debt they use, the more of it they need, because the more they spend, the more the stuff they’re buying costs, which means they need more debt.

And, to be clear, I’m talking about some of the best-capitalized companies in the world with some of the best credit in the world. Things get magnitudes harder and more expensive for a neocloud like CoreWeave (or a counterparty), or a data center SPV, or anyone that isn’t backstopped by a hyperscaler, like Google’s backstop of Cipher Mining’s data center for Anthropic.

Are you beginning to see the problem yet?

You can dance around making whatever noises you want about future GPUs or cadres of data centers magically giving somebody the margins you crave, but it appears that using AI only seems to be getting more expensive for hyperscalers, the companies that rent the GPUs, and basically anyone running a business using AI models.

Spare me your anecdata! Every AI startup is unprofitable, and every time somebody describes an AI company “getting profitable” it’s during some mythology-adjacent rain dance about mythical 90% gross margins on inference, or, in the case of the data center providers, after they’ve amortized billions (or tens of billions) of dollars’ worth of GPUs.

The problem is that the longer this goes on, the more expensive it gets, and the more extreme the payoff has to be. A trillion dollars of capex and the near-entire capitulation of the media and finance class cannot be justified by “some incremental improvements somewhere that nobody can really understand and an incredibly unprofitable way to let people write software that sometimes is faster but never in a way anyone can capture.”

Every wibbly-wobbly, fan fiction-adjacent analyst note or Twitter screed claiming that we’re in some sort of CPU or GPU supercycle never seems to reconcile with the reality that money doesn’t really seem to come out the other end when you buy something from NVIDIA unless you’re Anthropic or OpenAI. Data center operators have yet to show substantive proof of a sustainable business model renting out GPUs, let alone profits that would justify taking on billions in debt, and the payoff date seems to exist somewhere between “fuck knows” and “never.”

Take CoreWeave, the perennially debt-raising no IT loads refused neocloud, which has raised over $23 billion in the past two years with bond spreads that communicate a near-existential anxiety about the future of the company. Their previously-mentioned $1.25 billion bond raise — raised a little over a month ago — is now trading over 200bps higher than issuance when it was already at a 9.625% yield, which genuinely brings into question how future debt raises will go considering it’s guiding $31 billion to $35 billion in capex for a year and still has yet to build most of the capacity it needs to fulfil its massive backlog.

In fact, CoreWeave’s bond spreads look like a dog’s arsehole after eating a Thanksgiving turkey:

And because it hasn’t built it yet, that means it hasn’t bought all the stuff, and the longer it takes to buy the stuff, the more expensive it’ll get.

That’s also before you consider talent shortages, transformer shortages, electrical grade steel shortages, and generator shortages, which means you’re paying more money for the same thing (or less), likely having to accept whatever quality of material or talent you can get, all while battling to secure power as local authorities begin forcing data center builders to pay their fair share. This just happened in the Midwest, with local regulators in Port Washington, Wisconsin demanding Oracle puts up a $7 billion guarantee (costing it $100 million a year) to protect taxpayers if the power behind its Stargate data center doesn’t get built, largely due to that S&P credit downgrade…associated with it building so many data centers for OpenAI.

Nobody seems to want to discuss that every data center we’re describing is 2 to 3 years in the future, and the market is becoming increasingly impatient and showing signs of non-compliance with the greater AI narrative. The theoretical payoff for anyone buying a GPU in the last 12 months is that sometime in the year 2030 you will, in theory, make somewhere between 30% and 40% gross margins, assuming that you have had near-constant utilization of your GPU infrastructure from an industry where effectively every customer is either an unprofitable AI lab or a hyperscaler trying to keep their theoretical future compute off their balance sheet.

How does any of this work? Has anyone worked that out yet? Because it isn’t working right now, the only reason that any of you think it’s working is because CoreWeave (which lost $740 million last quarter) and Nebius ($399 million in revenue, $8.45 billion in debt) haven’t had trouble raising debt.

Be real with me: do any of you seriously believe CoreWeave exists in 2030?

Remember: its largest customer is OpenAI, either through Microsoft (70% of its revenue), Google (for OpenAI), or its own payments that are paid net 360.

In fact, why stop there — do you think OpenAI will be around in 2030?

I’m not asking these questions to be a dick or because I’m a hater, but more out of a genuine sense of curiosity. Over the weekend, the Wall Street Journal reported that NVIDIA was in talks with OpenAI to guarantee $250 billion in financing for a 10GW data center (allegedly) being built by SoftBank affiliate SB Energy, by which I mean NVIDIA would guarantee the compute payments (as it has with CoreWeave and Lambda but at a much bigger scale) so that SB Energy can raise debt to buy the chips from NVIDIA to rent to OpenAI:

Nvidia’s backing would allow the data-center developer, which is owned by Japanese billionaire Masayoshi Son’s investment firm SoftBank, to raise debt at more favorable terms than it could if OpenAI had no financial backer, since OpenAI has no investment-grade credit rating as an unprofitable private company. The AI company has been in advanced talks to lease the site for several weeks, people familiar with the matter said.

What’s even crazier is that the $250 billion guarantee would only cover lease payments and construction costs, and, per The Journal, NVIDIA is also discussing a deal to finance the $350 billion in GPUs to go inside it. It is unclear how that would happen, who would fund it, how it would get funded, or really anything about the deal.

This is the final boss of circular financing. SoftBank, which owns over $100 billion (on paper) in OpenAI stock, is using its affiliate SB Energy (which OpenAI and SoftBank invested in in May) to raise debt to build a 10GW data center — likely costing more than $500 billion in chips and construction — by getting a backstop from NVIDIA (which invested $30 billion in OpenAI and cited it as a material indirect customer in its 10K), which will also make upwards of $350 billion in revenue from the deal.

If/when this deal closes, SoftBank (which owns more than 15% of SB Energy) will use the contract signed with OpenAI as a way to take SB Energy public, giving both it and OpenAI a massive equity gain, all while feeding revenue from one investment to another investment, at least in theory.

Will any of this happen? God no. SB Energy is a confusing and murky business. SoftBank sold 85% of its shares to Toyota to form a company called Terras Energy in 2023, and it’s unclear if the new SB Energy has anything to do with the old one. Even if it did, neither company named SB Energy has ever actually built a data center, and to my knowledge, nobody has gotten close to building a 10GW data center.

Then there’s the problem of the debt itself. It’s unlikely that SB Energy raises all this money at once, which means that it’s going to fall into the same problem as hyperscalers are facing — that the more debt that AI data centers raise, the more expensive it becomes to raise debt for AI data centers.

That, and the debt markets are already showing their distaste. Back in May, SB Energy (via an SPV called SE Cosmos LLC) raised $999 million in 144A bonds (private debt sold exclusively to qualified institutional buyers) rated BB- (junk) by Fitch and BB+ by S&P Global to buy a former 3M campus and turn it into a 70MW data center, and it only got that with a guaranty from SoftBank Group.

Since issuance, its (option-adjusted) spread has grown from 351bps to 536bps, and that’s for a relatively low amount of debt for a relatively-straightforward data center.

Sidenote: It’s also unclear how that project gets built. Based on TD Cowen estimates, a 70MW data center would cost about $3 billion including chips and construction. The data center, per S&P Global, will be leased to “Silver Bands 3,” a company that, based on the existence of two SoftBank subsidiaries called Silver Bands 4 and 6, appears to be a subsidiary of SoftBank that is renting a data center from a subsidiary of SoftBank.

None of this appears to matter to ratings agencies.

Even with the cast-iron guarantee of mag7 findom NVIDIA, it’s hard to see how SB Energy pulls together what will likely be a succession of different $10 billion debt deals of the course of several years, especially given the above-discussed curdling of the AI data center debt markets.

I also think it’s fairly likely somewhere between nothing and very little happens as a result here, even if NVIDIA offers its backstop.