2026-07-11 02:09:57

Welcome to another edition of Generalist Intelligence, the weekly intelligence briefing that delivers situational awareness in 20 minutes or less. To unlock the full briefing, join as a member.

This week, we examine surging memory prices, Meituan’s US-chip-free breakthrough, and a surprising data center bottleneck.

— Mario

“There is only one proved method of assisting the advancement of pure science — that of picking men of genius, backing them heavily, and leaving them to direct themselves.”

— James Bryant Conant, the chemist who ran America's wartime science, writing to the New York Times in August 1945

How much?!

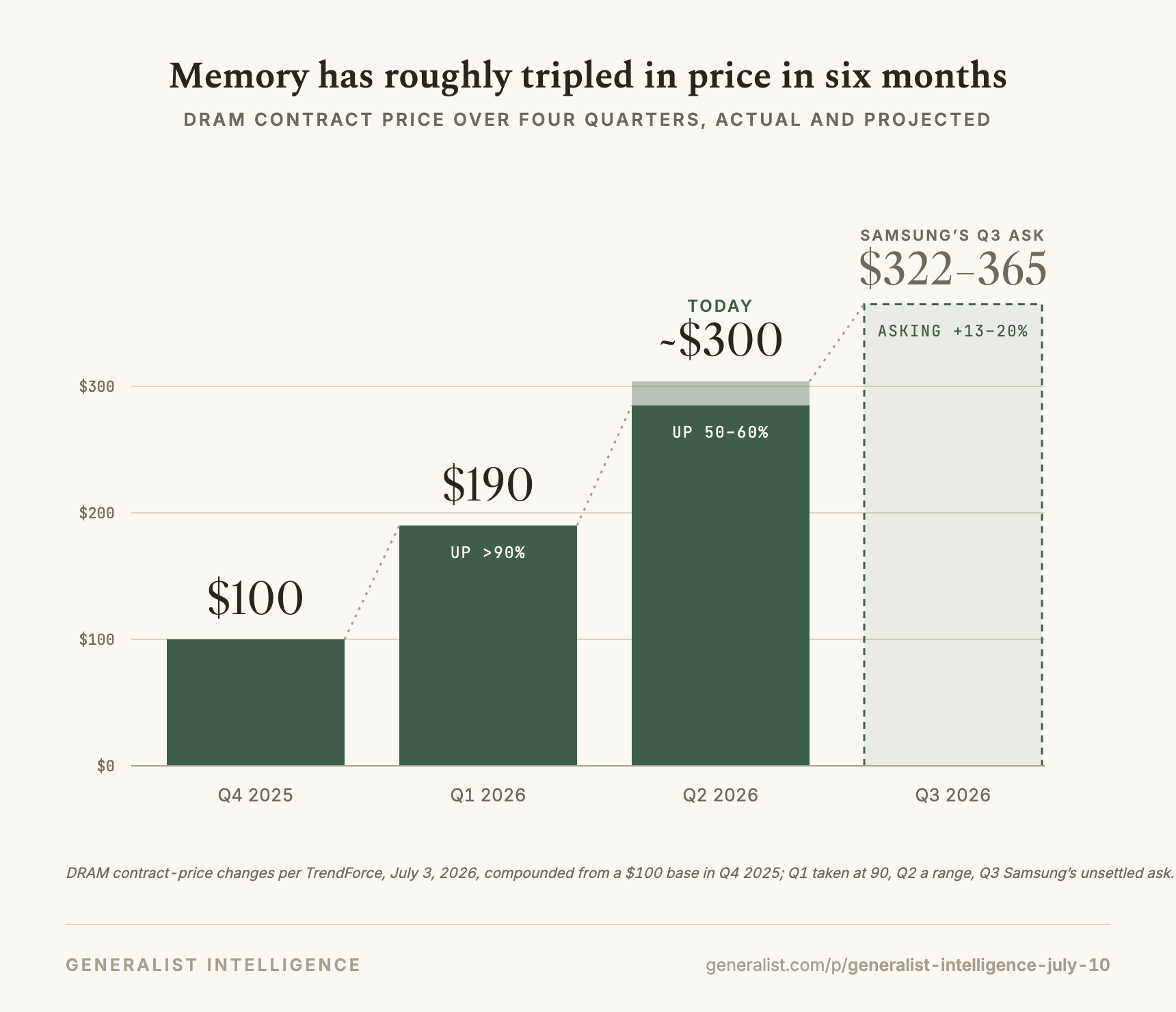

Samsung is pushing for another memory price increase of up to 20% for next quarter, on top of around 90% in Q1 of 2026, and 50-60% in Q2. That’s three consecutive quarters of major price hikes for DRAM, the type of memory chip that go into everything from your phone to AI servers, driven by data centers buying up nearly all available supply. For the first time in years, memory makers like Samsung, SK Hynix, and Micron hold real pricing power, which will show up in their margins and, eventually, in the price of every laptop, phone, and car you buy. For AI infrastructure, it’s a growing tax on anyone trying to build or scale compute that isn’t a hyperscaler with the leverage to lock in supply years in advance.

2026-07-04 01:35:32

Welcome to another edition of Generalist Intelligence, the weekly intelligence briefing that delivers situational awareness in 20 minutes or less. To unlock the full briefing, join as a member.

This week, we distill the second and third-order effects of GLP-1s, a narrative violation in AI, and growing tension around rare earth minerals.

— Mario

“Advertising may be described as the science of arresting the human intelligence long enough to get money from it.”

— Stephen Leacock, teacher and humorist, in The Garden of Folly.

Welcome to GLP-World

There is a large, venomous desert lizard called a Gila monster, which eats only once or twice a year. In the early 1990s, an endocrinologist named John Eng started wondering how that was possible – just an idle curiosity, but he cobbled together a small study. He soon isolated a novel peptide in the reptile’s venom that dramatically lowered blood sugar, just like the human body’s naturally occurring GLP-1 hormone, only it lasted for hours instead of minutes. Three decades later, a synthetic version of the molecule Dr. Eng discovered in Gila monster venom is quietly upending capitalism. You know it as Ozempic, and it’s changing everything.

So, no more obesity?

There’s that, obviously, with all the knock-on effects for junk food makers (bad – research shows high-calorie, ultra-processed foods are first to go) and tailors (very good – all those alterations and newly body-confident folks buying their first really good tuxedo). But the mechanism by which GLP-1 drugs like Ozempic suppress people’s appetites looks likely to be far more powerful than cutting out mere “food noise” for those who want to snack less.

2026-06-30 20:03:34

“There are a lot of people that are going out there and saying things like, ‘all jobs are going away,’ or ‘we're going to automate everything,’ or this language about the permanent underclass. And it really upsets me because not only is it inaccurate, but it's really harmful to the psychology of a lot of people that I think have a very important role to play in the future of humanity.” – Matan Grinberg

Listen or watch now on

YouTube, Spotify, or Apple Podcasts

Matan Grinberg is the co-founder and CEO of Factory, an AI company valued at $1.5 billion that helps enterprises like Nvidia, Morgan Stanley, and Adobe automate software development through “Droids,” intelligent agents designed to streamline software engineering. Before Factory, Matan spent more than a decade in theoretical physics, studying string theory at Princeton and UC Berkeley. His work now centers on a different kind of complex system: how software gets built in an era of increasingly capable AI agents, open models, and shifting compute economics.

In our conversation, we explore:

How Emmy Noether’s theorem continues to shape Matan’s approach to technology, business, and AI

Why Matan believes there will always be more problems to solve, even as AI becomes more capable

The resource allocation problem facing CEOs as they balance headcount, compute, and token budgets

Why Factory is betting on model independence and Matan’s take on the SpaceX-Cursor deal

Why Matan pushes back on conflating open models with “Chinese models” and wants a stronger open-model ecosystem

The identity crisis that followed Matan’s decision to leave physics

Lessons from Factory’s first few years, including learning to push back and identify gaps in his own knowledge

Factory’s culture, values, and Matan’s partnership with co-founder Eno Reyes

.tech domains: An identity for builders at their core.

Brex: The intelligent finance platform.

Persona: Trusted identity verification for any use case.

(00:00) Intro

(03:50) Noether’s theorem explained

(06:45) How the search for what’s conserved informs Matan’s work

(10:53) Why there will always be more problems to solve

(11:58) The resource allocation problem of the AI era

(15:54) Factory’s mission: bringing autonomy to software engineering

(18:28) How Factory decides what to build next

(20:10) Why Factory abstracts away model choice

(22:07) How Factory wins enterprise customers

(23:15) Matan’s take on the SpaceX-Cursor deal

(27:48) Why open-weight models matter

(29:19) Anthropic’s Fable 5 release and the debate over AI guardrails

(35:33) How Matan got into string theory

(38:21) Working with Juan Maldacena

(41:53) Startup founders vs. theoretical physicists

(46:15) Rethinking physics and redefining his identity

(51:29) Discovering AI and code generation

(52:53) The origins of Factory

(55:52) Lessons from Factory’s first few years

(59:58) Learning to push back and finding the holes in his knowledge

(1:03:17) Factory’s culture and values

(1:08:11) Matan’s predictions for the future of AI and Factory

(1:10:49) Final meditations

LinkedIn: https://www.linkedin.com/in/matan-grinberg

Website: https://factory.ai

A Tale of Two Cities: https://www.amazon.com/Tale-Cities-Dover-Thrift-Editions/dp/0486406512

The Picture of Dorian Gray: https://www.amazon.com/Picture-Dorian-Gray-Oscar-Wilde/dp/0141439572

The Brothers Karamazov: https://www.amazon.com/Brothers-Karamazov-Fyodor-Dostoevsky/dp/1685781152

Zero to One: Notes on Startups, or How to Build the Future: https://www.amazon.com/Zero-One-Notes-Startups-Future/dp/0804139296

Invisible Cities: https://www.amazon.com/Invisible-Cities-Italo-Calvino/dp/0156453800

Collected Fictions: https://www.amazon.com/Collected-Fictions-Jorge-Luis-Borges/dp/0140286802

Emmy Noether: https://en.wikipedia.org/wiki/Emmy_Noether

Juan Maldacena: https://www.ias.edu/scholars/maldacena

William Shakespeare: https://en.wikipedia.org/wiki/William_Shakespeare

Shaun Maguire on X: https://x.com/shaunmmaguire

Frank Slootman on LinkedIn: https://www.linkedin.com/in/frankslootman

Sridhar Ramaswamy on LinkedIn: https://www.linkedin.com/in/sridhar-ramaswamy

Eno Reyes on LinkedIn: https://www.linkedin.com/in/enoreyes

Noether’s theorem: https://en.wikipedia.org/wiki/Noether%27s_theorem

Factory: https://factory.ai

Why One Superintelligence Is More Dangerous Than a Thousand (Vincent Weisser, CEO & Co-Founder of Prime Intellect): https://www.generalist.com/p/why-one-superintelligence-is-more

IMDb Top 250 movies: https://www.imdb.com/chart/top/

Harakiri: https://www.imdb.com/title/tt0056058

La Grande Bellezza: https://www.imdb.com/title/tt6155190

La Haine: https://www.imdb.com/title/tt0113247

The Master: https://www.imdb.com/title/tt1560747

Interstellar: https://www.imdb.com/title/tt0816692

Proper Time to the Black Hole Singularity from Thermal One-Point Functions: https://www.researchgate.net/publication/345261524_Proper_time_to_the_black_hole_singularity_from_thermal_one-point_functions

I’d love it if you’d subscribe and share the show. Your support makes all the difference as we try to bring more curious minds into the conversation.

Production and marketing by penname.co. For inquiries about sponsoring the podcast, email [email protected].

2026-06-26 23:08:14

Friends,

This week, we look Eastward. While the West concerns itself with which model is the smartest, Beijing published a 17-point plan to shove AI into every shop, clinic, and classroom in the country. It is one America cannot afford to ignore.

Read for our view on what Xi Jinping’s AI push means, Google’s brain drain, what satellite imagery tells us about data center build-outs, and the obscure crystal in high demand.

— Mario

P.S. To learn more about our process and vision for Generalist Intelligence, read our introductory piece. To unlock the full briefing, join as a member.

“Civilization advances by extending the number of important operations which we can perform without thinking about them.”

— Mathematician-philosopher Alfred North Whitehead, 1911

China’s latest AI push

Earlier this month, almost entirely unnoticed by the Western press, China dropped an AI policy document – the fabulously resistible Implementation Opinions of the Ministry of Commerce and 8 Other Departments on Accelerating the Development of ‘AI+Consumption’ – that we think is worth a closer look. It feeds into two things old China hands often say: “America invents, China applies” and, effectively, “China likes central planning.” And once you get past the title and the usual platitudes about how the plan is “Guided by Xi Jinping Thought on Socialism with Chinese Characteristics for a New Era,” it becomes clear that something serious is going on.

2026-06-25 22:02:53

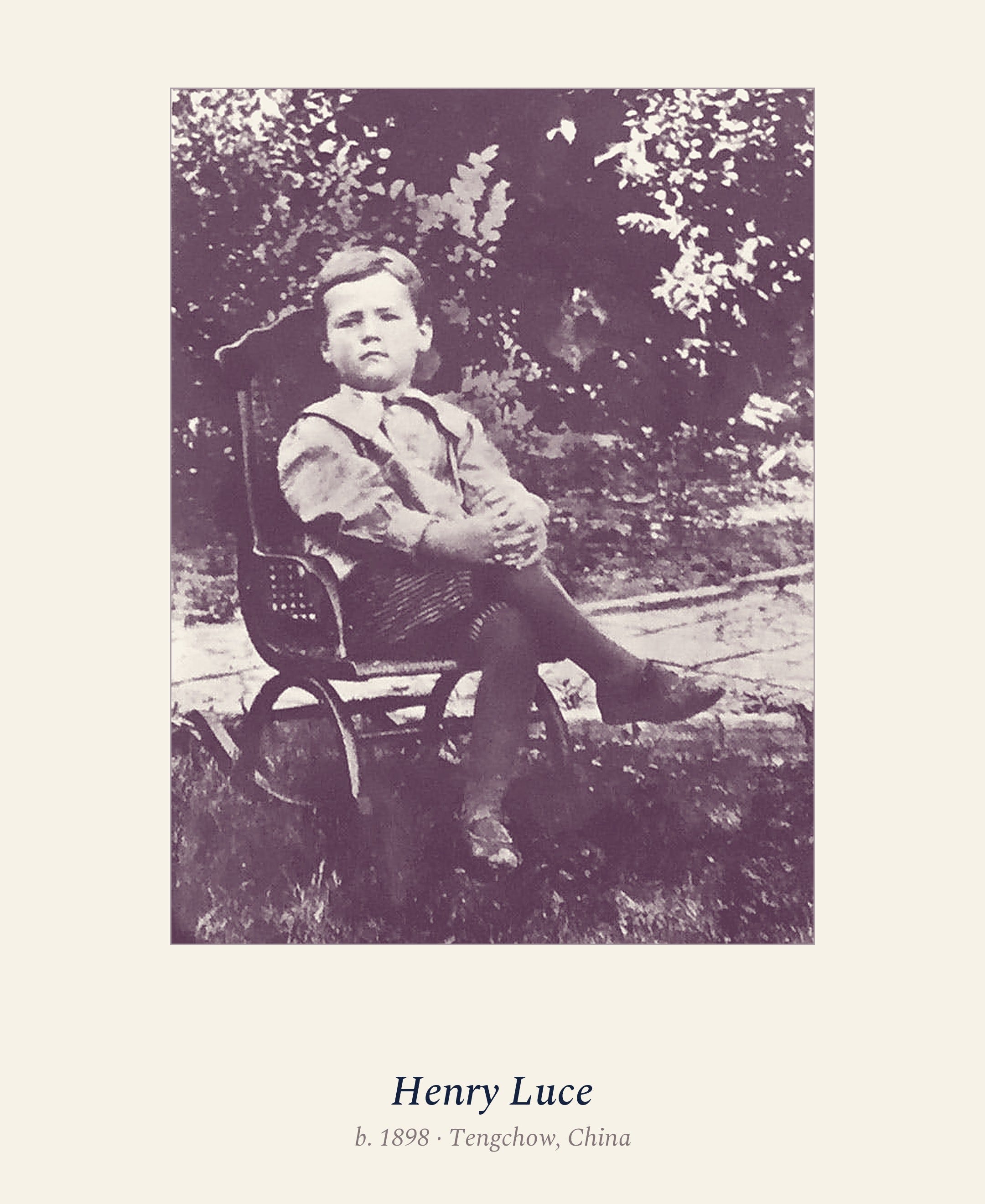

By the end of his life, Henry Luce was at home in any room. Not loved, of course. His strong opinions, a staunch conservatism and a fervent anti-communist bent among them, hardly earned universal approbation. But he appeared unfazed, unperturbed, more than a little superior. “He lived well above the tree line on Olympus,” one of his editors remarked. Fundamentally, at home.

As the founder of Time, Fortune, Life, and Sports Illustrated, Luce had met the good and great of every industry. And not merely met them, but shaped their lives. That had propelled him not just to eminence but extraordinary wealth. In 1966, Luce’s holdings generated $503 million. He’d founded the company 43 years earlier with $86,000.

He died the year after, aged 68, leaving behind the trappings of the Great Man, the consummate insider.

Whether the man ever felt that solidity, that sense of ultimate belonging, only he could have answered. The boy, the Luce of five and nine and fifteen, did not. No matter where Luce went, he did not fit, did not belong. First, he was the son of a missionary in Shandong, an American in China. Then, after he was sent to the China Inland Mission school at Chefoo, he was the American among English students. Worse yet, he was a stammerer, a tic he’d acquired the year prior and that his tutor had declared “absolutely imaginary” and an “evil habit.”

“Everything is going as usual but not very well,” Luce wrote in a letter home from Chefoo. “It sort of seems to hang on not in spells of homesickness but a hanging torture, I well sympathise with prisoners wishing to commit suicide.” He was ten years old, precociously articulate, and utterly alone. “I am getting that hatred of which I will never get over even tho I was here hundreds of years.”

In tandem with Luce’s suffering, a commensurate competitiveness emerged. In other missives, he writes of his desire to destroy his peers. “My years ambition has been accomplished, that is to lick Hayes.... For this year I have made the form record in going up places, that is 8 places.” A sense of deficiency seemed to give way to obsessive self-comparison and ferocious drive.

At fifteen, Luce was sent to boarding school in Connecticut, attending Hotchkiss. Yet again, he was a child apart, an “aid boy” among New England’s blue bloods. As a condition of his scholarship, he had to wait tables in the dining hall, serving breakfast to his paying classmates. Rather than living on campus, he was sent to a boarding house a mile away. He knew little of American life (“I did not know a single rule of football when I came here,” he said, wore shabby clothing fabricated in China, and his halting speech was devoid of the Yankee idioms. He earned the nickname “Chink.” He had gone from an American boy in China to a Chinese adolescent in America.

Luce’s response to serving the richer students was not to disdain them, but rather to aspire to join them. Instead, he looked down on the scholarship boys, assuming himself to be their superior. “These scholarship fellows here are all fundamentally fine, but they lack certain qualities — especially noticeable at table — that one misses!” Rather than find acceptance within a group, Luce chose to separate himself from it, to set his sights on ascending America’s social ladder. He achieved it.

Not every founder was ostracized quite as totally as Luce. Culture, class, geography, and even his manner of speaking conspired to separate him from his peers. But the experience of being an outsider, of being profoundly out of place, is the most common trait observed from studying the formations of great entrepreneurs. It is also among the most acute, contributing to a desire to prove one’s relative worth and breeding a sense of specialness, even if reflected through a dark mirror. Perhaps every adolescent feels some moment of difference; this is the beginning of selfhood. But not everyone experiences it quite like this.

Part I of the Saplings series, which studies the early lives of legendary founders, explores this quality, its variations, and its impact. As follows:

A world apart. We discuss the ways in which differences in nationality, ethnicity, class, and other external factors make these children feel like outsiders. Often, this seems to be coupled with a commensurate desire to overprove one’s worth to the rejected environment.

Familial interlopers. In some cases, children are strangers in their own homes. They’re shunned by parents and siblings, or perceived as somehow alien, which influences a sense of independence.

Isolated by their body. Illness, disabilities, and deformities impacted some founders similarly, separating them from their peers physically and forcing them to spend more time in their own minds.

Wired differently. Having a mind that runs on unusual tracks distances many founders from those around them. They often struggle to communicate, finding it easier to demonstrate their abilities and intelligence in other ways.

From the other side. Negative transformative experiences, like a close familial death, force children to grow up early and contribute to a sense, in some cases, of being somehow special.

It is worth noting that neither this series in general nor this piece in particular imagines that it can explain everything about these people. To notice that so many remarkable founders were marginalized by the world around them in their early years is not to say that it is a necessity of greatness or to draw a direct correlation between exile and achievement, nor to valorize the very real, often terrible suffering these people endured. Humans are capable of metabolizing hardship into many things — helplessness, energy, cruelty, inspiration, revenge, and grace—none of which ennoble the original sin.

And, of course, every case is a matter of degree and a matter of perspective. Only the founders themselves could tell us how they perceived their remove from the world around them, and given what unreliable narrators these characters often are, you would be a fool to take them at their word. (“I’m super normal” is Jensen Huang’s self-appraisal.) This is, then, just a fragment of something, a sliver of colored glass we are putting up to the light to look at the shadows it casts.

If you are interested in the broader process behind the Saplings project, you might enjoy our piece introducing it here.

A young Masayoshi Son, Softbank’s flamboyant impresario, considered his grandmother “repulsive.” This was the woman who raised him and loved him. The son of Korean immigrants in Japan, the Son family had little money. Each morning, the elderly woman placed a tiny Masayoshi on a two-wheeled wooden cart and pulled him through the neighborhood, through dirt and pig slop, to see what food the restaurants near the train station had discarded the night before. This was what they fed the family pigs. Son recalled the scene as an adult, describing the “slippery” ground and its “rotting smell.”

2026-06-23 20:03:42

“No one is data ready. Absolutely no one is data ready.” —Yash Patil

Listen or watch now on

YouTube, Spotify, or Apple Podcasts

Yash Patil is the 23-year-old founder and CEO of Applied Compute, a $1.3 billion company helping businesses train custom AI models on their own data: smaller, cheaper, and purpose-built for the work they actually do. Before founding the company, Yash dropped out of Stanford and spent two years at OpenAI working on post-training infrastructure and Codex. He left with one core conviction: every company that runs its critical workflows on someone else’s model is building on shifting sand. Applied Compute is his answer to that problem, already serving customers including DoorDash, Cognition, and Mercor.

In our conversation, we explore:

Why “own or be owned” is becoming existential for any company that relies on frontier AI models

What it was like inside OpenAI the weekend the board fired, and then reinstated, its CEO

Why post-training is where competitive advantage is now being built, and what reinforcement learning with verifiable rewards actually is

Why evals have become the new production environment, and why companies will never share them with frontier providers

How a specialized model built for DoorDash outperformed frontier models on a narrow, high-value task

Why cost, not capability, is now the primary driver pushing companies toward custom models

Why Yash believes AI’s transformation of the economy will unfold over decades, and why near-term fears about mass job displacement are misplaced

Brex: The intelligent finance platform.

Guru: The AI source of truth for work.

Persona: Trusted identity verification for any use case.

(00:00) Introduction

(03:50) Fable 5 and the case for owning your own models

(09:22) Why Applied Compute is betting on custom AI models

(12:30) Yash’s early influences and first projects

(17:42) His brief time building at Stanford

(19:29) Leaving Stanford for OpenAI

(25:58) Inside OpenAI during Sam Altman’s firing

(28:18) What Yash admires about Sam Altman

(29:43) Teaching models to reason

(35:39) The core insight behind Applied Compute

(39:40) How Applied Compute works with its customers

(45:55) Why model training never ends

(48:56) Why not every task needs a frontier model

(51:25) The culture and people of Applied Compute

(54:50) Applied Compute’s training infrastructure

(58:43) The coming compute crunch and other predictions

(1:03:48) Final meditations

Website: https://yashpatil.me

LinkedIn: https://www.linkedin.com/in/yash-s-patil

The Design of Everyday Things: https://www.amazon.com/Design-Everyday-Things-Revised-Expanded/dp/0465050654

Brendan Foody on X: https://x.com/BrendanFoody

Luke Metz’s website: https://lukemetz.com

Barret Zoph on X: https://x.com/barret_zoph

John Schulman on X: https://x.com/johnschulman2

Ian Osborne on LinkedIn: https://www.linkedin.com/in/ian-osborne

Applied Compute: https://www.appliedcompute.com

Claude Fable 5 and Claude Mythos 5: https://www.anthropic.com/news/claude-fable-5-mythos-5

Goldman Sachs: https://www.goldmansachs.com/

Sarah Chieng’s post on X: https://x.com/MilksandMatcha/status/1983587401688870972

Science Olympiad: https://www.soinc.org

Chai Discovery: https://www.chaidiscovery.com

TreeHacks: https://treehacks.com

Thiel Fellowship: https://thielfellowship.org

Building a hill-climbing machine: Launching seven new MAI models: https://microsoft.ai/news/building-a-hillclimbing-machine-launching-seven-new-mai-models

Kirkland & Ellis: https://www.kirkland.com

Palantir: https://www.palantir.com

Automating Merchant Onboarding at DoorDash: https://www.appliedcompute.com/case-studies/doordash

Composer: https://cursor.com/blog/composer

NVIDIA: https://www.nvidia.com

DeployCo: https://www.deployco.co

I’d love it if you’d subscribe and share the show. Your support makes all the difference as we try to bring more curious minds into the conversation.

Production and marketing by penname.co. For inquiries about sponsoring the podcast, email [email protected].