2026-07-14 08:00:00

I was born in the USA. Many tongues call me "American": Italian (americano), French (Américain), German (Amerikaner), Dutch (Amerikaan), Afrikaans (Amerikaner), Japanese (アメリカ人, amerika-jin), Filipino (Amerikano), Hebrew (אמריקני), Arabic (أمريكي), Portuguese (americano), Russian (американец), and Hindi (अमरीकी, Amreeki).

I grew up in Southern California. Many of my friends were zeroeth-generation immigrants from Mexico. Weren't their parents born in North America, too?

As an adult, I lived in Washington State. There I met many fine Canadians, visiting for work, education, and play. Were they not Americans too?

We of the United States, in justice to Canadians and Mexicans, have no right to use the title "Americans" when referring to matters pertaining exclusively to ourselves.

-- James Duff Law

Circa 1903, James Duff Law coined the term "Usonian" for the peoples of the United States of America.

Esperanto speakers adopted "usonano" as early as 1905.

But why this term "America" has become representative as the name of these United States at home and abroad is past recall. Samuel Butler fitted us with a good name. He called us Usonians, and our Nation of combined States, Usonia.

– Frank Lloyd Wright

Wright popularized "Usonia" around 1927. To him, the US middle class outclassed European aristocracy. His Usonian homes celebrated the simplicity and individualism of US suburbia.

His Usonian homes inspired ranch-style houses.

But "Usonia" sounds too beautiful for the United States -- collegial, polished, academic. "Would you prefer Italian or Usonian wine with your halibut, ma'am?"

Our heritage is that of pilgrims and prophets and rednecks and reverends. We've got the best medical centers and the most overdoses; the best universities and the most young-Earth creationists.

I feel less than American and more than Usonian. I wish there were a word between…

Yankeeism is the general character of the Union. Yankee manners are as migratory as Yankee men. The latter are found everywhere and the former prevail wherever the latter are found. Although the genuine Yankee belongs to New England, the term "Yankee" is now as appropriate to the natives of the Union at large.

-- Thomas Colley Grattan

"Yankee" is a silly word. It probably originated from Dutch Janke ("Little John") or Flemish Jan Kees ("John Cheese").

During the Revolutionary War, British troops sang "Yankee Doodle" to paint US folk as raucous clowns. And in true Yankee fashion, US troops put it in their caps and called it macaroni. Yankee Doodle remains a source of national pride.

Brits (and Aussies) still use "Yankee" in a pejorative sense.

The US still exudes that panache. In the early 1800s, colonials built a civilization while consuming ~1 gallon of 90-proof liquor per month. Their children's children invented plastic and Hollywood, which pollinated via red cups and reality television. Only the US could elect a reality TV star to be its leader (twice). It takes gall to produce Idiocracy and then make it happen.

We should move the US capitol from DC to Las Vegas.

Only the US could give casinos to its decimated native populations as a consolation prize. Only we could inflict upon ourselves epidemics of painkillers, crack, school shootings, and Tide Pods. Only we could produce evangelicals.

US folk are Yankees. We're obnoxious, tacky, foul, and we're proud of it.

To foreigners, a Yankee is an American.

To Americans, a Yankee is a Northerner.

To Northerners, a Yankee is an Easterner.

To Easterners, a Yankee is a New Englander.

To New Englanders, a Yankee is a Vermonter.

And in Vermont, a Yankee is somebody who eats pie for breakfast.

-- E B White

But Southern Yankees reject the label. Many still cling to the failed Confederate nation of their fathers' fathers. They're right to remain angry -- we've since let our Southern siblings slide ever further into poverty, illiteracy, and hopelessness. To them, Yankeeism is another flavor of European aristocracy.

Southerners are suffering, and it's easier to be dismissive than to be helpful. The Civil War will not end until Southerners are proud to call themselves Yankees too.

the spartan, cramped, and unstintingly functional jeep became the ubiquitous World War II four-wheeled personification of Yankee ingenuity and cocky, can-do determination.

-- Doug Stewart

We should make Yankee synonymous with the best of the United States -- dynamism, ingenuity, hospitality, self-sufficiency.

I like "Usonia", but it ain't US. We're Yankees, for better and worse, and we should act like it.

2026-07-08 08:00:00

I like reading letters for particular persons.

You and I talk about simulating each other. I've got a little Jon (not a Lil Jon) inside me. He tells me about chemistry, and systems, and to not take it all so seriously, dude. That voice is one of the wisest and best parts of me. Thanks.

I can't simulate just anybody. Only high-fidelity training data creates simulations, and we've shared the human experience. I cherish our training data -- years of spats, riffs, tiffs, spills, wins, and shenanigans.

My blog sometimes feels like a pro-wrestling match, where I pretend(?) to beat myself up for others' enjoyment. But I always lose those fights. After crowds grow bored, Vince McMahon sends me to the guillotine.

You once said something about how you talked to your brother in your head. Okay, I don't remember the words, but it made an impression on me, and I'm not sure what that impression is. An echo of an echo rattles in my skull now.

Long ago, we had a late-night (or early-morning?) Uber ride to LAX. We started chatting about anabolic steroids. Our driver talked to us about pro-wrestling.

I'm sorry I abandoned you. I'm always so desparate to find greener pastures for us. Was it green enough already? I'm glad I'm back.

Litte Jon (not Lil Jon) is great, but he's not you. Not even close. I need more training data.

tt

2026-07-05 08:00:00

tl;dr: Investors can dodge taxes by parking their capital gains in ~6,400 designated low-income census tracts.

After the 2008 financial crisis, investors retreated from risky markets (e.g. distressed towns) and chased trusted collateral (e.g. coastal real estate). Affluent communities recovered while poor towns starved of capital.

Changes in jobs/businesses by community prosperity quintile, 2011-2015, via EIG.

Meanwhile, US investors sat on trillions of dollars of unrealized capital gains. Selling a stock triggers taxes, so people held on for opportunities that (A) offset their realized capital gains and (B) make more money.

In 2015, EIG suggested waiving taxes for capital gains deployed into a capital-starved community, i.e. an "opportunity zone" (OZ).

The 2015 paper was co-authored by Kevin Hassett (Trump's Council of Economic Advisers chair) and Jared Bernstein (Biden's Council of Economic Advisers chair).

Deferring a capital gain typically only works when trading real estate for real estate (i.e. 1031 exchange). But with EIG's OZ proposal, you could defer a gain from any asset class (e.g. stocks, crypto, a whole business, collectibles) by rolling it into an OZ fund.

Opportunity zones hit Congress in April 2016 as the Investing in Opportunity Act. It died in the Senate Finance Committee.

The bill was sponsored by Tim Scott (R-SC), Cory Booker (D-NJ), Pat Tiberi (R-OH), and Ron Kind (D-WI).

In December 2017, Congress folded the idea into the humongous Tax Cuts and Jobs Act, which became law.

Here's how it works for investors:

The whole OZ 1.0 clock runs to a fixed date: the deferred tax is due at the end of 2026 no matter when you bought in, so the pause is shorter the later you invested — about seven years for 2019 money, five for 2021.

Here's what you got for parking your gains:

Bonus: A Qualified Opportunity Zone Business (QOZB), which keeps 70% of its tangible property in-zone, unlocks a 31-month "working-capital safe harbor" (i.e. it doesn't need to pay taxes on its unspent cash).

$100 long-term gain at 23.8% top rate, fund value doubling over ten years.

In early 2018, 31,680 low-income tracts (and ~9,450 contiguous neighbors) were eligible to become opportunity zones; each governor could nominate 25% of their State's eligible tracts. In June 2018, the US Treasury certified 8,764 tracts (including most of Puerto Rico). These designations were locked for 10 years with no mechanism to swap tracts.

Low-income tracts are defined by populations who (A) exceed 20% poverty or (B) fall below 80% of surrounding area's median family income.

Designated Opportunity Zone tracts per 100,000 residents, via CDFI.

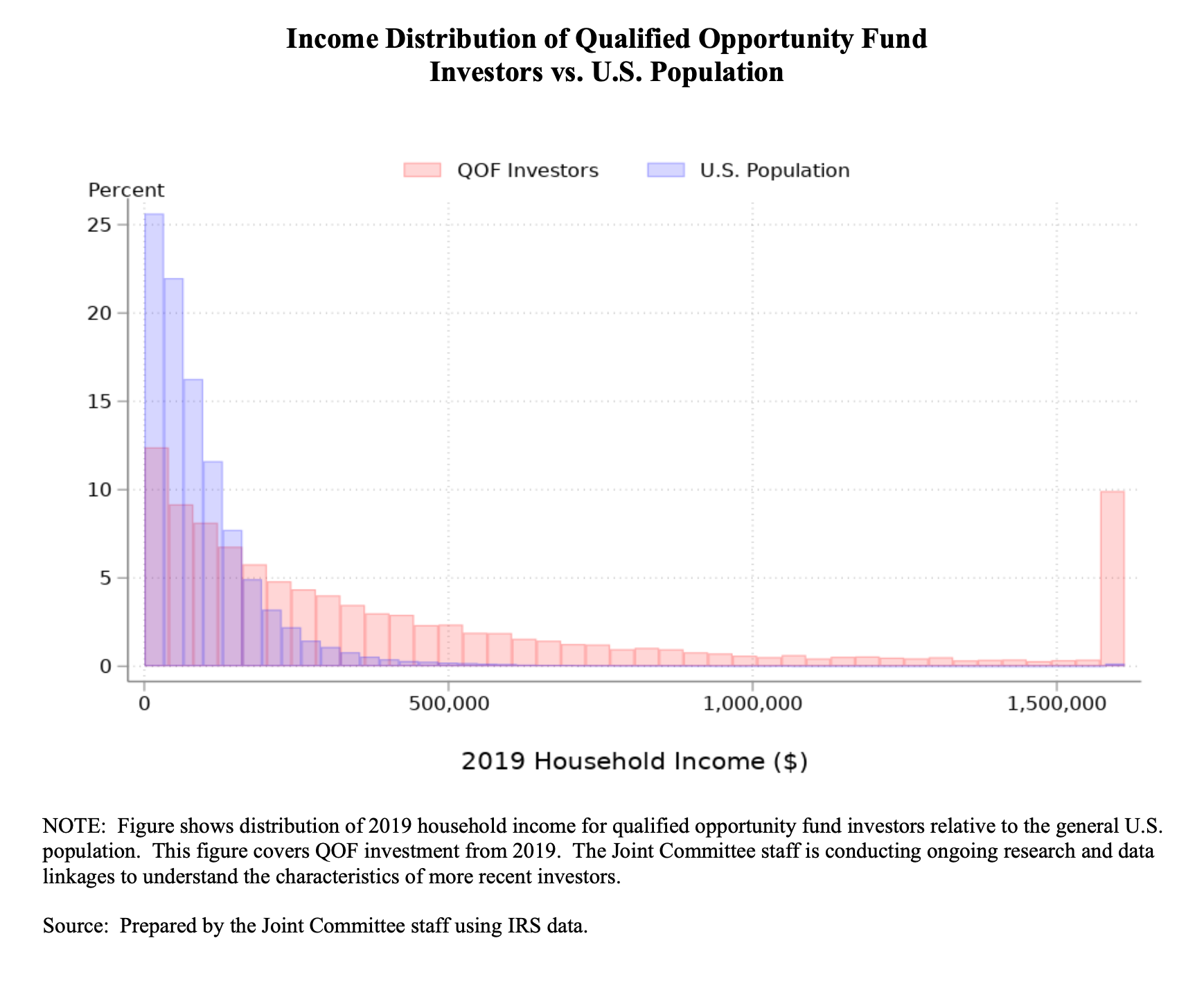

Opportunity zones lured in the billionaires. This should be no surprise — the investors with all the unrealized capital gains suddenly had a safer way to put their money back in the game. Well-designed incentives can entice people to trade their valuable stocks for distressed land.

The biggest OZ fund sponsors were conventional real-estate shops. Bridge Investment Group led with roughly $3.7 billion raised, followed by CIM Group (~$2.3B), Griffin Capital (~$1.6B), and Cantor Fitzgerald (~$1.1B).

Cumulative equity in opportunity funds, via JCT.

But opportunity zones specifically reward holding appreciating assets in a fixed place for ten years. Real estate naturally fits these criteria, but buildings are not necessarily businesses.

Share of investment by sector, via JCT.

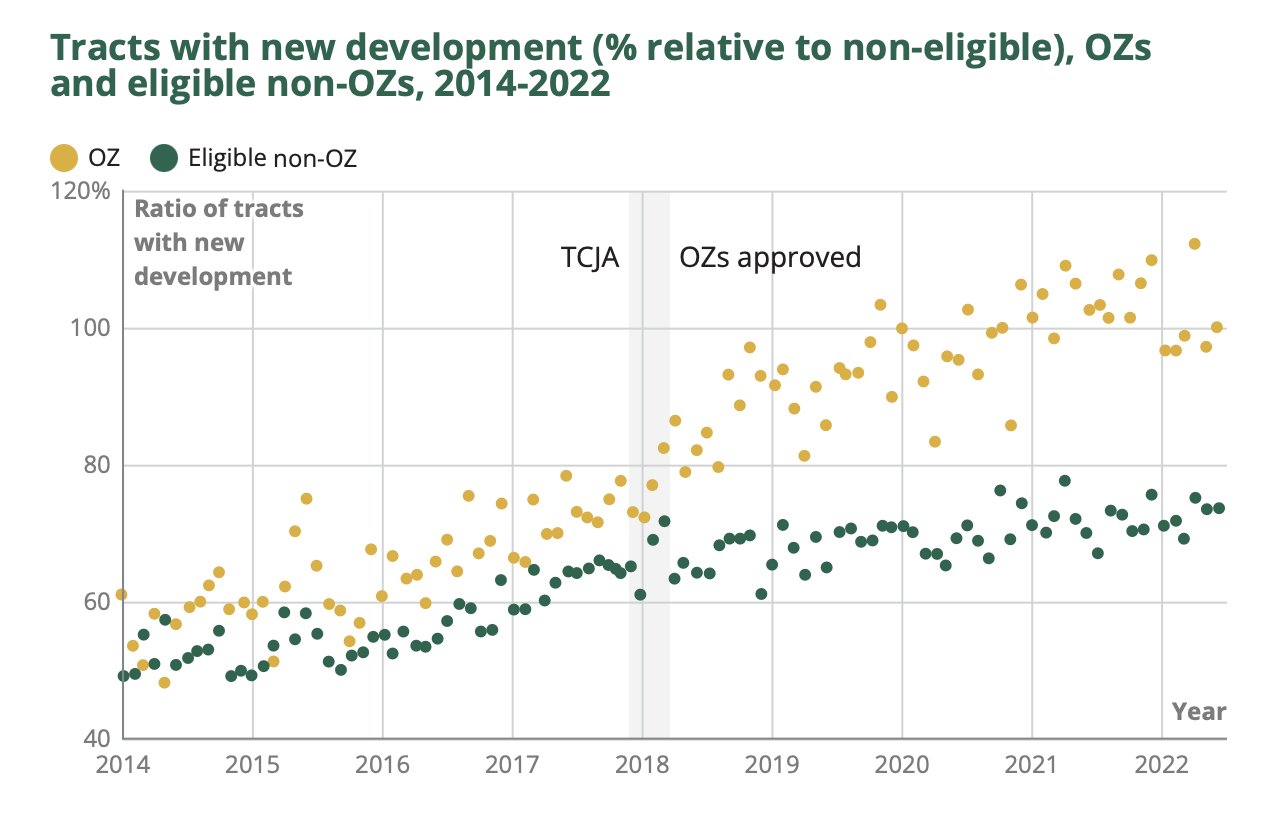

Even with tax perks, ten years is a long shadow. Of the eligible tracts that were nominated, most received no investment whatsoever. OZ funds ate low-hanging fruit. Money flowed into tracts with already appreciating land values (or intrinsic strategic value).

Distribution of QOZ property investment, US Treasury.

5% of a State's designated zones could bypass the low-income threshold if (A) they shared borders with a designated low-income tract and (B) their median family income did not exceed 125% of the poorer tract's.

Reporting requirements were stripped from the original law, so investigative journalists filled gaps for the program's first two years. The New York Times traced how a Nevada tract (Tesla's Gigafactory) with 7.5% poverty made the list when the Treasury overruled its own staff after a Milken Institute event. ProPublica documented how a Baltimore $233M waterfront megaproject (owned by Under Armour's Kevin Plank) qualified via a digital-mapping artifact.

But the "contiguous loophole" was not exploited as much as expected. Only 230 non-low-income tracts (2.6% of the 5% threshold) were designated.

Averages of tract-median values, via Urban Institute.

Of course some investors abused OZ incentives, but money generally flowed into low-income tracts as intended. Someday we may know whether those private investments actually outweigh lost tax revenue.

OZ 1.0 was set to expire on December 31, 2026.

But the One Big Beautiful Bill made opportunity zones permanent in July 2025. OZ 2.0 follows the same playbook with stricter eligibility requirements (and zero contiguous tract provisions). Only 60% of OZ 1.0 tracts are fully eligible for OZ 2.0.

Tracts' median family income threshold was reduced to 70% (prev. 80%) of the State's median (or surrounding metro area).

Starting January 2027, here's what you get in OZ 2.0:

2026-06-29 08:00:00

You can literally hire me (Taylor) via API:

curl -X POST https://looop.ai/api/doodle \

-H "Authorization: Bearer looop_YOUR_KEY" \

-H "Content-Type: application/json" \

-d '{

"gig_id": 5,

"input": { "prompt": "write a poem about horses" },

"deadline": 3600

}'Yes, I am building a dystopian cyberpunk hellscape. No, I can't provide more details yet. Just know that if I ever achieve my goals, every human will have shoes, blankets, clean drinking water, medical care, leisure, etc.

Create your account at looop.ai if you'd like to work via API too.