2026-02-28 01:06:27

America’s greatest asset is its optimism — an attitude that’s unleashed unparalleled wealth and validated the thesis that anyone can achieve the American dream. But here’s the glitch in the matrix: Capitalism is the belief that there should be winners and losers, that incentives drive innovation and prosperity. And they do. But the gilded few amass power and use that power for regulatory capture to expand their wealth … a lot.

The Gini coefficient is a measure of inequality popular among economists. Zero indicates everyone in a society has the same; a score of 1.0 means one individual owns everything. In the U.S., we’re higher than 0.8 — about the level seen when the French were separating people from their heads. The superwealthy have amassed vast fortunes without fear of mobs arriving with pitchforks. U.S. policies, turbo-charged by a 2010 Supreme Court ruling that opened the gates to unlimited spending on elections, have widened the gap between the haves and the have-nots. As wealth concentrates, billionaire political spending rises higher, securing policy outcomes that further concentrate wealth. The chaser is inflation, which transfers still more wealth from earners, whose purchasing power erodes, to owners, who are insulated.

A reckoning is underway, ignited by the mountain of Epstein documents, which are giving the public a window into the rarefied world where the 0.01% are protected by the law but not bound by it, while the rest of us are bound by the law but not protected by it. Among hundreds of names appearing in the files are three of the nation’s best-known billionaires: Donald Trump, Elon Musk, and Bill Gates. Americans are fed up, not just with the depravity of some people in the Epstein class, but also with the massive wealth they continue to accumulate while the working class struggles. We aren’t talking about beheadings today, but modern-day guillotines are on the way: shame and taxes.

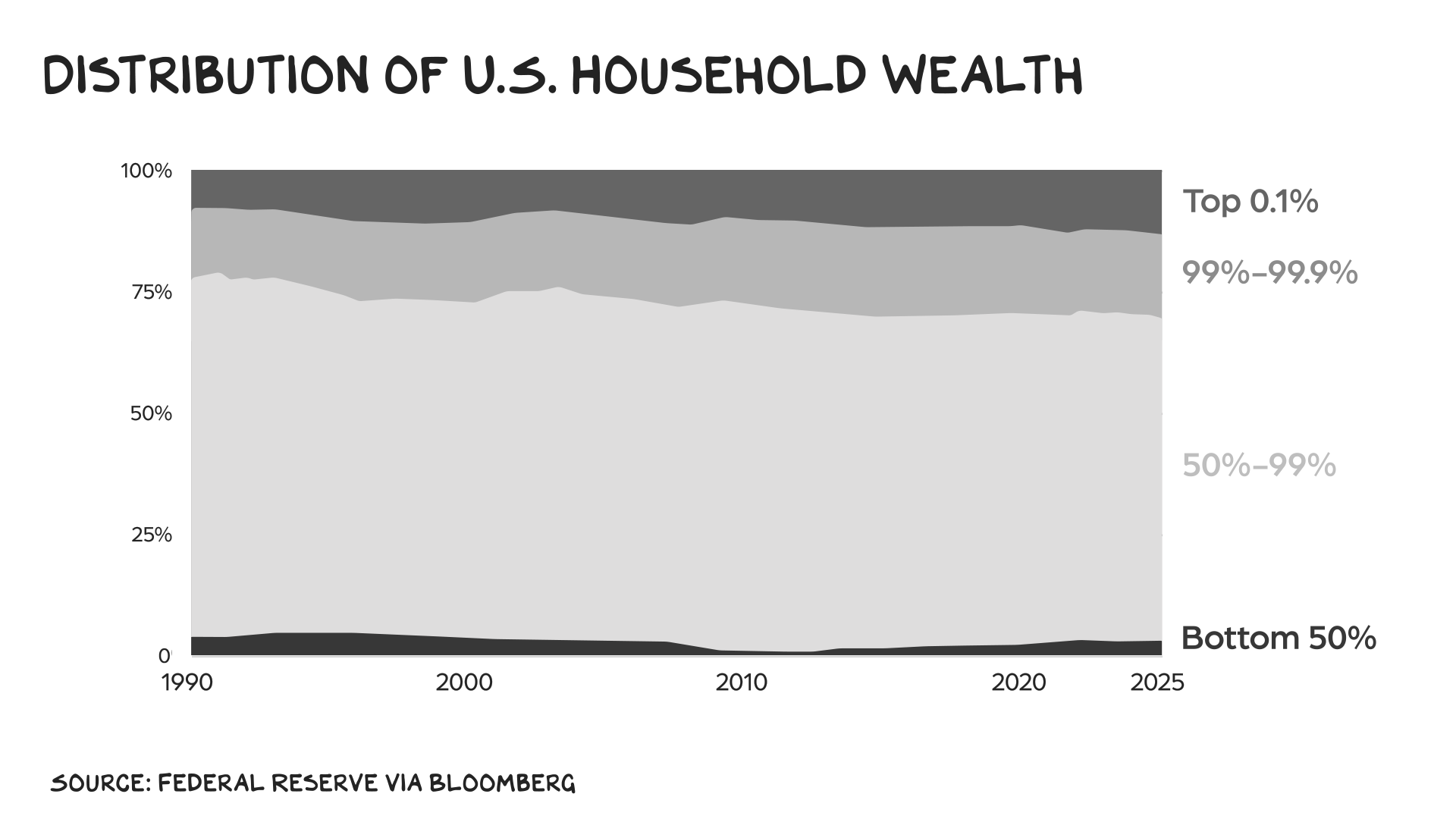

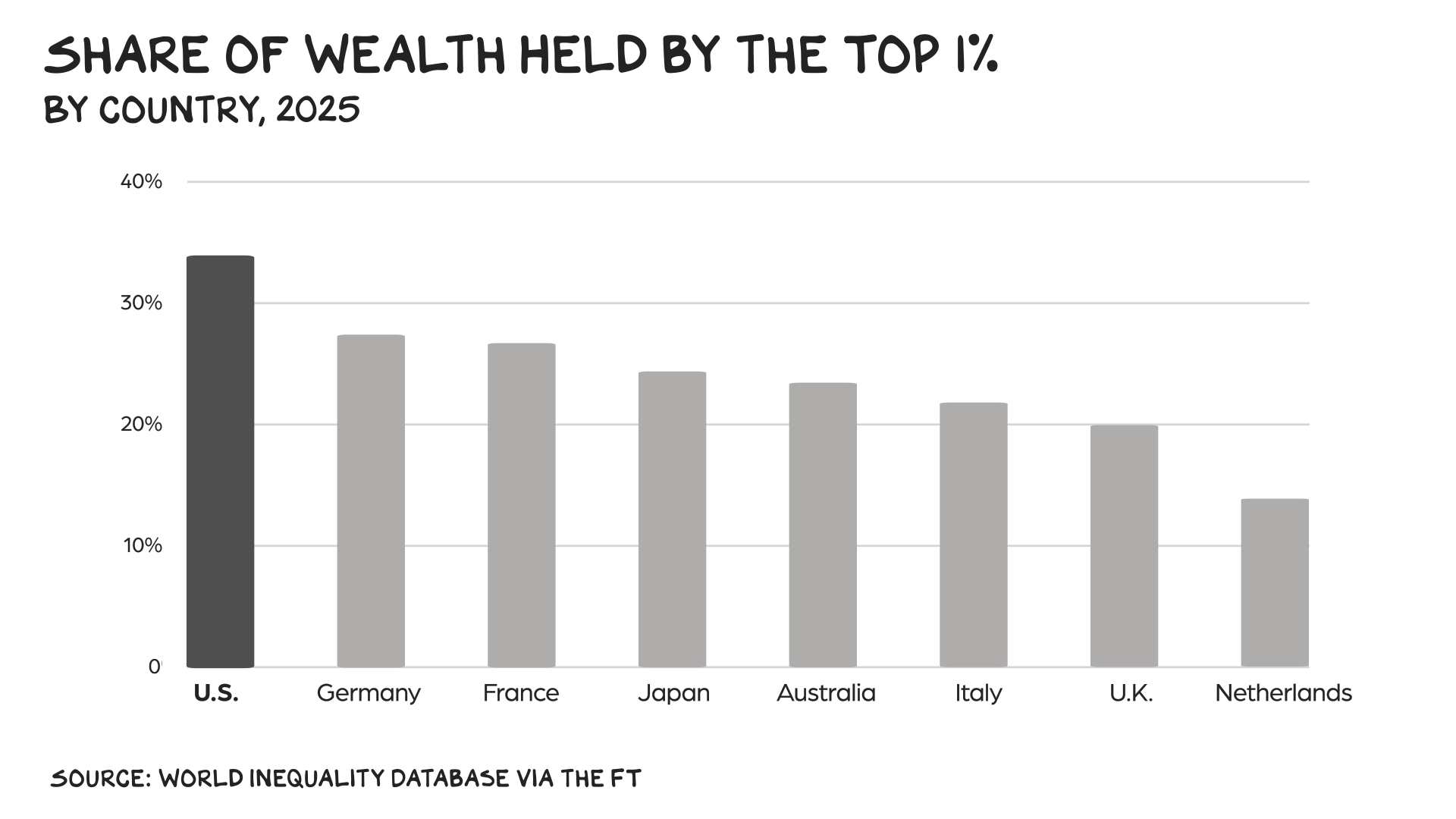

The top 1% control almost one-third of the nation’s wealth, their biggest share since World War II. The top 0.1% increased their wealth by 40% in the last three years. But UC Berkeley researchers say the top 400 paid only an estimated 23.8% of their income in taxes from 2018 to 2020 — a smaller percentage than the average American — down from 30% between 2010 to 2017. It’s not just an American phenomenon. Last year, the world’s 500 richest people added more than $2 trillion to their collective net worth, according to the Bloomberg Billionaires Index.

Governments around the world are putting the rich on notice, hoping to address this disparity, plug fiscal holes, raise money for defense, and address the challenge of aging populations. A few examples:

Wealth taxes are a tempting way to tackle inequality. They’re also an obvious means of raising revenue. In America, $5 trillion of receipts and $7 trillion in spending is (again) a transfer of wealth from earners to owners, as it’s inflationary. This isn’t sustainable. Fiscal strain in the U.K. prompted 30 economists to sign an open letter calling for a wealth tax to raise tens of billions of pounds. Voters also like this idea: Three quarters of British adults backed the idea of a 2% tax on wealth above £10 million.

But there’s a problem; wealth taxes don’t work. In 1990 a dozen OECD countries had wealth taxes. By last year, only three remained, in Norway, Spain, and Switzerland. Most of the measures collected little revenue and failed to meet their goals, sparking concerns they could stifle innovation and growth. In some cases, the superrich packed their bags and fled.

If the megawealthy don’t leave the country, they’ll deploy accountants and lawyers to value their assets at 40% of what tax authorities believe they’re worth. How are you going to value a stake in a small business? If you don’t have the cash sitting in your bank account, will you have to sell assets to pay your bill? Wealth taxes in the U.S. would also face challenges on constitutional grounds. Targeting people’s assets may violate private property laws while creating massive administrative complexity.

Finding flaws in wealth taxes is easier than coming up with solutions. But there are commonsense ideas we should adopt to ensure the superrich and large corporations pay their fair share. One is tackling the carried-interest loophole, which allows private equity and venture capital managers to be taxed at the capital gains rate of 20%, well below the top rate of 37% for ordinary income. Taxing carried interest as ordinary income could raise about $15 billion over the next 10 years. That’s not a game changer, but it’s a start.

Capital isn’t more noble than sweat. There’s no reason someone should pay a 37% tax on their income while the wealthy pay much less when they sell stocks. In 2021 income from capital gains accounted for 39% of pretax income for the top 1%, compared with less than 1% for those in the bottom three quintiles.

If you want to climb into the upper echelons, follow a three-step strategy: Buy, borrow, die. While wages are taxed when they’re earned, assets are taxed when they’re sold. The wealthy often borrow against stock holdings and other assets, which grow more valuable over time, rather than selling them, deferring their tax liability. As long as interest rates are lower than the rate of return on the assets they hold, billionaires can spend more on houses, yachts, or even islands, while enjoying significant wealth appreciation. In 2011, a year in which Jeff Bezos was worth $18 billion, he reported so little income that he received a $4,000 child tax credit. Americans with more than $100 million of wealth held an estimated $8.5 trillion in unrealized capital gains in 2022.

One idea: When the rich borrow and use their assets as collateral, they should pay tax on the difference in the value of that stock or property between when they originally bought it and the day it’s pledged. Treating borrowing as a taxable event could raise more than $100 billion over a decade.

A hobbled IRS is a massive tax cut for rich individuals and large corporations, amounting to the most regressive tax in recent history. Auditing lower- and middle-income tax returns is easy; holding wealthy taxpayers with high-priced lawyers accountable requires a lot more resources. The tax gap, the difference between the amount of taxes owed and the amount collected on time, surged to almost $700 billion in 2022. Most of the taxes owed stem from underreporting of income by richer taxpayers.

An $80 billion increase in IRS funding planned under Biden’s Inflation Reduction Act (since rescinded) would have alleviated some of the pressure, netting more than $600 billion over a decade. Instead, the agency faces even more pain after losing more than a quarter of its workforce. If we want to move the needle on wealth inequality, strengthening IRS enforcement is critical.

In 1969, Congress learned that 155 taxpayers with incomes exceeding $200,000 had paid no federal income tax in 1966. So legislators created an early version of the alternative minimum tax, which essentially compares an individual’s income before and after they claim certain deductions and embrace all the loopholes. After a portion of their income is exempted, the taxpayer must pay tax on whichever amount is greater. Legislation in 2017 didn’t eliminate the tax, but it limited its scope, dropping the number of taxpayers affected from more than 5 million to 200,000.

We should have an individual AMT, with people above a $1 million threshold taxed at 40% and those over a $10 million threshold taxed at 60%. I estimate this could raise hundreds of billions per year, while only affecting the top 0.2%, or 275,000 taxpayers.

As the tax debate heats up, billionaires inevitably start to focus on spending more time with their family — as long as they live in a low-tax state. In 2023, Bezos announced he was moving to Miami after almost three decades in Seattle to be close to his parents. His family must have used all the face time to persuade him to sell billions in stock in a state that doesn’t tax capital gains. In 2022, Washington state imposed a new 7% capital gains tax on sales of stocks or bonds of more than $250,000.

Now Mark Zuckerberg is in the process of buying a property in Florida, triggering speculation that he’s unhappy about the proposed new tax on California billionaires. You think? The Meta CEO has benefited enormously from taxpayer-funded investments in education and infrastructure in the Golden State. If he wants to peace out to Florida, fine, but when he sells tens of billions of dollars in stock, he shouldn’t be able to escape tax on the massive wealth he accrued while living in California.

Billionaires can run, but they shouldn’t be able to hide.

We don’t need a revolution. We need a functioning IRS, capital gains taxed as income, and the death of the carried-interest loophole. The guillotine isn’t coming, the 1040 is. At a minimum, let’s stop pretending the system is broken by accident. It’s working exactly as designed — for those at the very top.

Life is so rich,

P.S. Kara Swisher and I are coming to Minneapolis. Catch the first ever Resist and Unsubscribe LIVE event, on March 8 at 7 p.m. at the Pantages Theater. Tickets are available here, with proceeds to benefit the Immigrant Law Center of Minnesota.

The post The Epstein Tax appeared first on No Mercy / No Malice.