2026-08-05 06:51:05

Welcome to the Premium edition of How They Make Money.

Over 300,000 subscribers turn to us for business and investment insights.

In case you missed it:

This week, we’ll visualize more than 50 reports ranging from Airbnb to Zillow.

Today’s batch captures the mood of earnings season pretty well, with huge AI ambition, rising capital intensity, and a few quieter stories improving underneath.

Today at a glance:

🕵️ Palantir: Sovereign AI

🚀 SpaceX: Growth Meets the Bill

↗️ AMD: Data Center Takes Over

🛵 Grab: The Overhang Shrinks

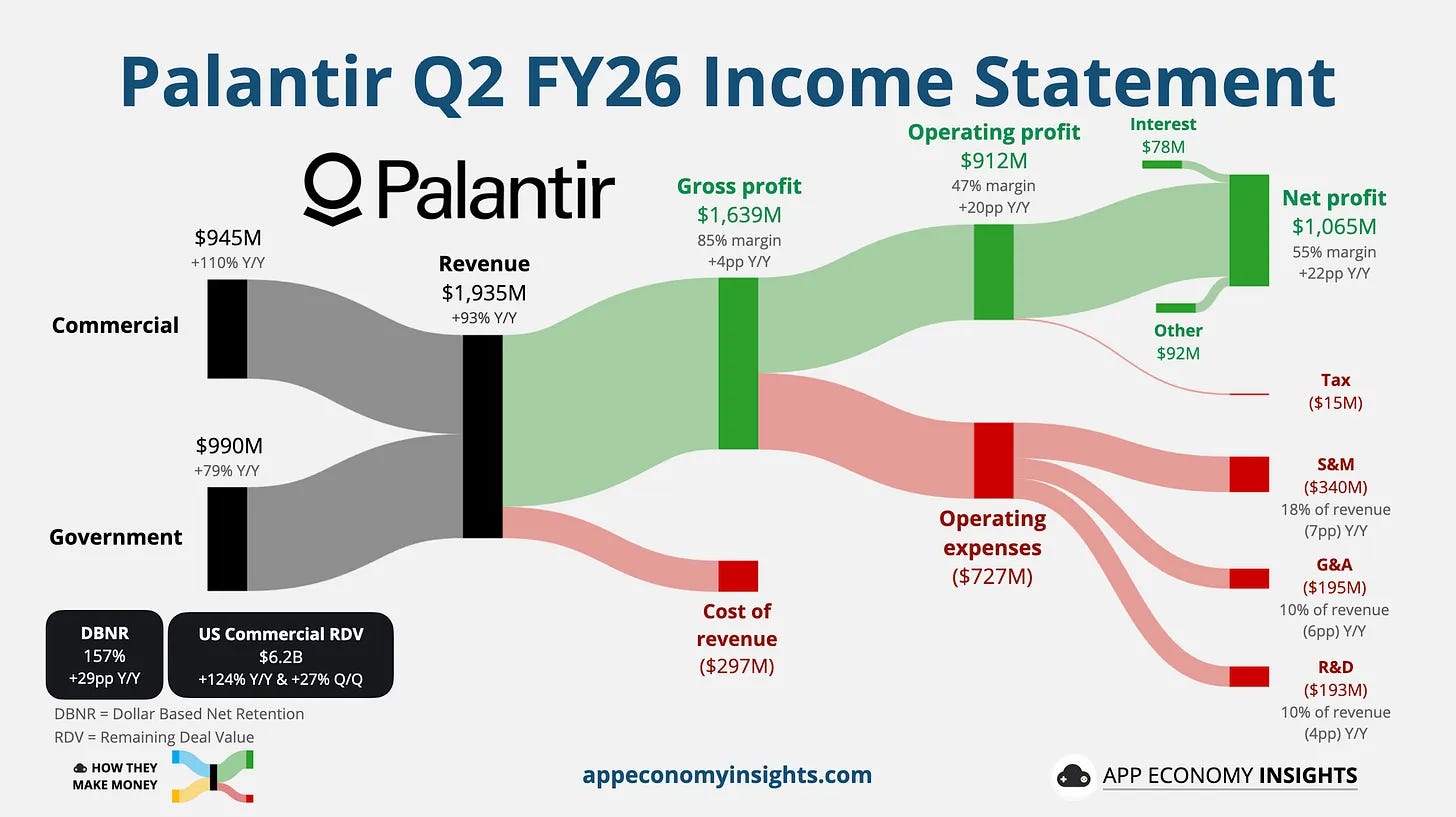

Palantir Q2 revenue jumped 93% Y/Y to $1.94 billion ($130 million beat), marking the 12th consecutive quarter of acceleration. Adjusted EPS of $0.41 beat by $0.06. The Rule of 40 score climbed again to 155, with adjusted free cash flow reaching $1.22 billion at a 63% margin.

US revenue keeps pulling away.

💼 US Commercial: $764 million (+149% Y/Y, +28% Q/Q).

🪖 US Government: $809 million (+90% Y/Y, +18% Q/Q).

Total US revenue reached $1.57 billion, up 115% Y/Y and now representing 81% of Palantir’s business. International revenue grew a much slower 33% to $363 million, with CEO Alex Karp again dismissive of Europe: “The growth sucks.”

The pipeline behind the print looks even more bullish. Palantir closed 220 deals worth at least $1 million, including 73 above $10 million.

TCV (Total Contract Value): The total value of contracts signed during the quarter reached a record $2.13 billion in US Commercial, up 153% Y/Y.

RDV (Remaining Deal Value): Contracted revenue not yet recognized climbed 124% Y/Y (and a staggering 27% Q/Q) to $6.24 billion in US Commercial, giving Palantir an increasingly large backlog behind future growth.

Palantir’s new framing is “sovereign AI.” Management argues customers increasingly want AI without handing proprietary data, workflows, or competitive intelligence to frontier model providers. AIP (Palantir’s AI Platform) sits between companies and the models, letting customers swap LLMs while keeping their data and operational logic under their own control. Karp put it more bluntly: customers should not become “vassal states of the language labs.”

We discussed last quarter that tokens are the new coal. Models and tokens are becoming cheaper commodities. Palantir wants to own the governed operational layer where companies turn them into actual work.

Palantir raised FY26 revenue guidance by roughly $500 million to $8.15–$8.16 billion, implying 82% growth, versus 71% expected just three months ago. US Commercial is now expected to grow at least 134% to more than $3.42 billion. Adjusted free cash flow guidance increased to ~$4.6 billion (from ~$4.3 billion previously).

Bottom Line: The fundamental story somehow keeps getting stronger. Revenue growth accelerated, US Commercial is now 39% of the top line, and free cash flow margins have crossed 60%. The valuation is still extreme at nearly 80x FY26 EBITDA, but Palantir is doing something equally extreme: accelerating above 90% revenue growth at nearly $8 billion of annual revenue while simultaneously expanding margins.

SpaceX’s first earnings report as a public company showed why investors are excited about the business and why the valuation remains difficult to digest.

2026-08-02 22:01:22

Welcome to the Premium edition of How They Make Money.

🔥 The July report is here!

All the key earnings visuals from the past month in one place.

✔️ Cut through the noise with clear, concise financial snapshots.

✔️ See revenue trends, profit margins, and key takeaways instantly.

Download the full report below or log in to your account.

![Screen Recording 2026-07-31 at 1.11.05 PM.mov [video-to-gif output image]](https://substackcdn.com/image/fetch/%24s_!xi2q!,f_auto,q_auto:good,fl_progressive:steep/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2Fc277fa3f-21af-4980-b6d3-2972b35a07a8_800x448.gif "Screen Recording 2026-07-31 at 1.11.05 PM.mov [video-to-gif output image]")

Here’s a sneak peek of the 100+ companies included. 👀

☁️ Mega-Caps: Apple, Alphabet, Microsoft, Amazon, Meta, Tesla.

🧩 Semis: TSMC, ASML, Samsung, SKH, Intel, KLA, Qualcomm.

💊 Healthcare: J&J, UnitedHealth, Abbott, Intuitive Surgical.

🏦 Banks: JPMorgan, BofA, Wells Fargo, Citigroup, Schwab.

🍿 Entertainment: Netflix, Comcast, Roblox, Live Nation.

💰 Wealth: Morgan Stanley, Goldman Sachs, BlackRock.

💻 Software: IBM, SAP, ServiceNow, Fortinet, AppFolio.

☕ Restaurants: Starbucks, Chipotle, Domino’s, YUM!

✈️ Airlines: American, Delta, Southwest, United.

📡 Telecom: AT&T, T-Mobile, Comcast, Verizon.

💳 Payments: Amex, Visa, Mastercard, PayPal.

🛡️ Defense: Boeing, Airbus, Lockheed Martin.

🇫🇷 Luxury: LVMH, Hermès, Kering, L’Oréal.

🧬 Pharma: AbbVie, Sanofi, AstraZeneca.

🔬 Equipment: ASML, Lam Research.

🥤 Beverages: Coca-Cola, PepsiCo.

🚗 Autos: Rivian, GM, Ford, Ferrari.

📈 Brokers: SoFi, Robinhood.

🏨 Travel: Hilton.

Plus Reddit, Mondelez, Hershey, UPS, P&G, GE Vernova, Tilray, and more.

2026-08-01 22:02:56

Welcome to the Saturday PRO edition of How They Make Money.

Over 300,000 subscribers turn to us for business and investment insights.

In case you missed it:

📊 Monthly reports: 200+ companies visualized.

📩 Tuesday articles: Exclusive deep dives and insights.

📚 Access to our archive: Hundreds of business breakdowns.

📩 Saturday PRO reports: Timely insights on the latest earnings.

Today at a glance:

📱Apple: Ternus Handoff

🕶️ Meta: AI Bill Comes Due

📱 Samsung: Records Meet A Rout

💳 Visa: Volume Accelerates

💳 Mastercard: The Crack Didn't Widen

⏳ AbbVie: Growth Engines Hold

🧠 Lam Research: The Ramp Steepens

🥤 Coca-Cola: Volume Carries The Quarter

🧴 P&G: Iran Cost Bites

📱 Arm: Data Center Offsets Phones

🔬 KLA: 2027 Gets Bigger

🧬 AstraZeneca: Pipeline On Trial

🛩️ Airbus: The Ramp Finally Shows

📲 Qualcomm: Diversification On Trial

🛩️ Boeing: Cash Turns Positive

☕️ Starbucks: Measurable Momentum

🔒 Fortinet: The Surge Extends

📦 UPS: The Reset Lands

💡 Cadence: AI Demand Compounds

🪶 Robinhood: Firing On All Cylinders

🍪 Mondelez: North America Turns

🏨 Hilton: Mid-Scale Rebounds

🏎️ Ferrari: Scarcity Pays

🚙 Ford: Trucks Cover The Damage

💳 PayPal: The $60 Question

📈 Coinbase: Winning a Smaller Market

🎤 Live Nation: World Tour Expands

🌯 Chipotle: Momentum Meets A Wobble

🌮 Yum! Brands: Pizza Hut Heads Out

🍫 Hershey: Price Over Volume

👾 Roblox: Monetization Trade-Off

👽 Reddit: Monetization Outruns Users

⚡ Rivian: R2 Hits the Road

🏦 SoFi: Records Meet A Shrug

🦷 Align: Scanners Down

🩺 Teladoc: The BetterHelp Pivot

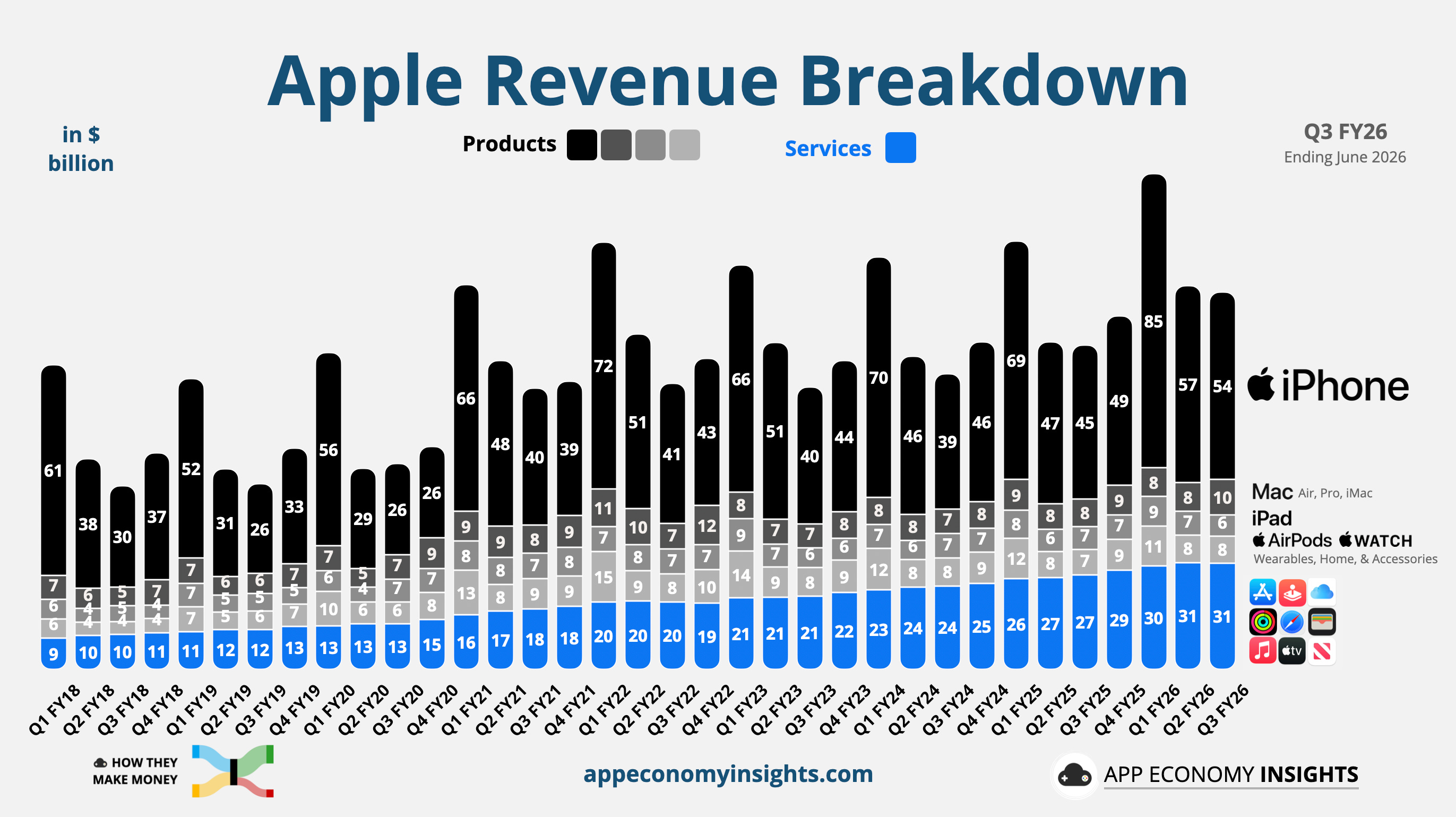

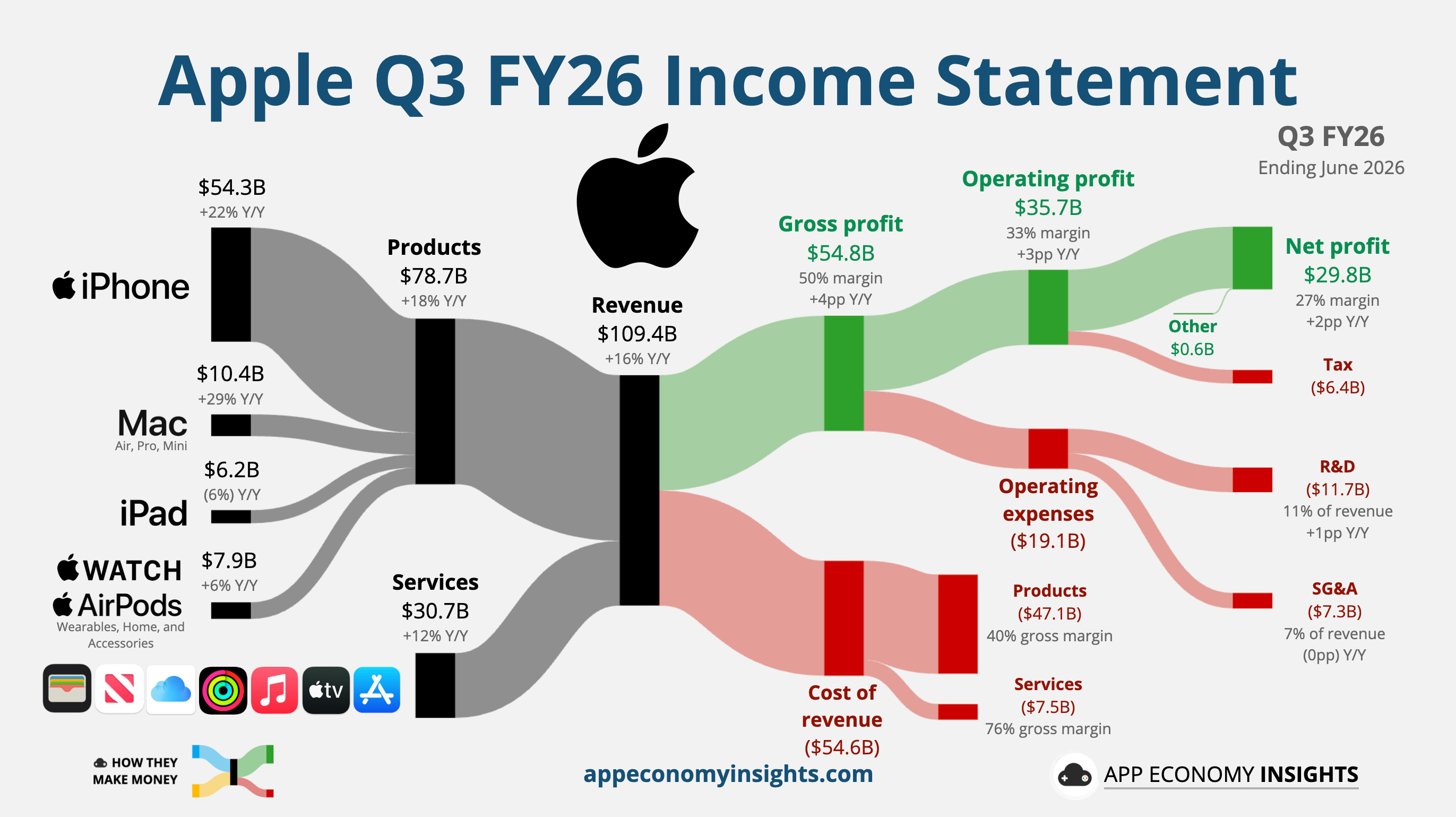

Apple’s Q3 revenue rose 16% Y/Y to $109.4 billion ($0.5 billion beat), while EPS reached $2.02 ($0.13 beat). Tariff refunds contributed $0.11 to EPS, but underlying results still came in ahead of expectations. These were June quarter records, yet shares fell about 6% after earnings.

iPhone revenue grew 22% to a record $54.3 billion.

Mac jumped 29% to a record $10.4 billion.

China rebounded 22% to $18.8 billion.

Services slowed to 12% growth, reaching $30.7 billion.

This was Tim Cook’s final earnings call before John Ternus takes over in September. He leaves Apple with a good problem to have: the company cannot make enough devices.

Cook said unexpectedly strong iPhone and Mac demand exhausted Apple’s flexibility to secure more advanced chips. These constraints primarily affected Mac this quarter and will broaden to iPhone, Mac, and iPad in the September quarter. Apple still guided revenue growth to 9%–11%, with iPhone expected to grow in the mid-teens, but the outlook came in below consensus.

Memory is becoming the larger margin problem. Cook described the market as a “hundred-year flood,” with rapidly rising prices already forcing Apple to increase some Mac and iPad prices. Excluding tariff benefits, gross margin declined sequentially, and Apple expects another step down in Q4 as cheaper inventory runs out.

Meanwhile, R&D spending rose 32% Y/Y to $11.7 billion as Apple accelerated its AI investment. Cook also suggested heavy Siri users could eventually be pushed toward more expensive iCloud+ plans, offering an early glimpse of how Apple might monetize its AI overhaul.

Ternus inherits one of Apple’s strongest product cycles in years, but also a supply chain that cannot fully support it and a margin structure increasingly exposed to memory inflation. The next iPhone cycle must prove Apple can manage both pressures while convincing customers that its AI catch-up is finally real.

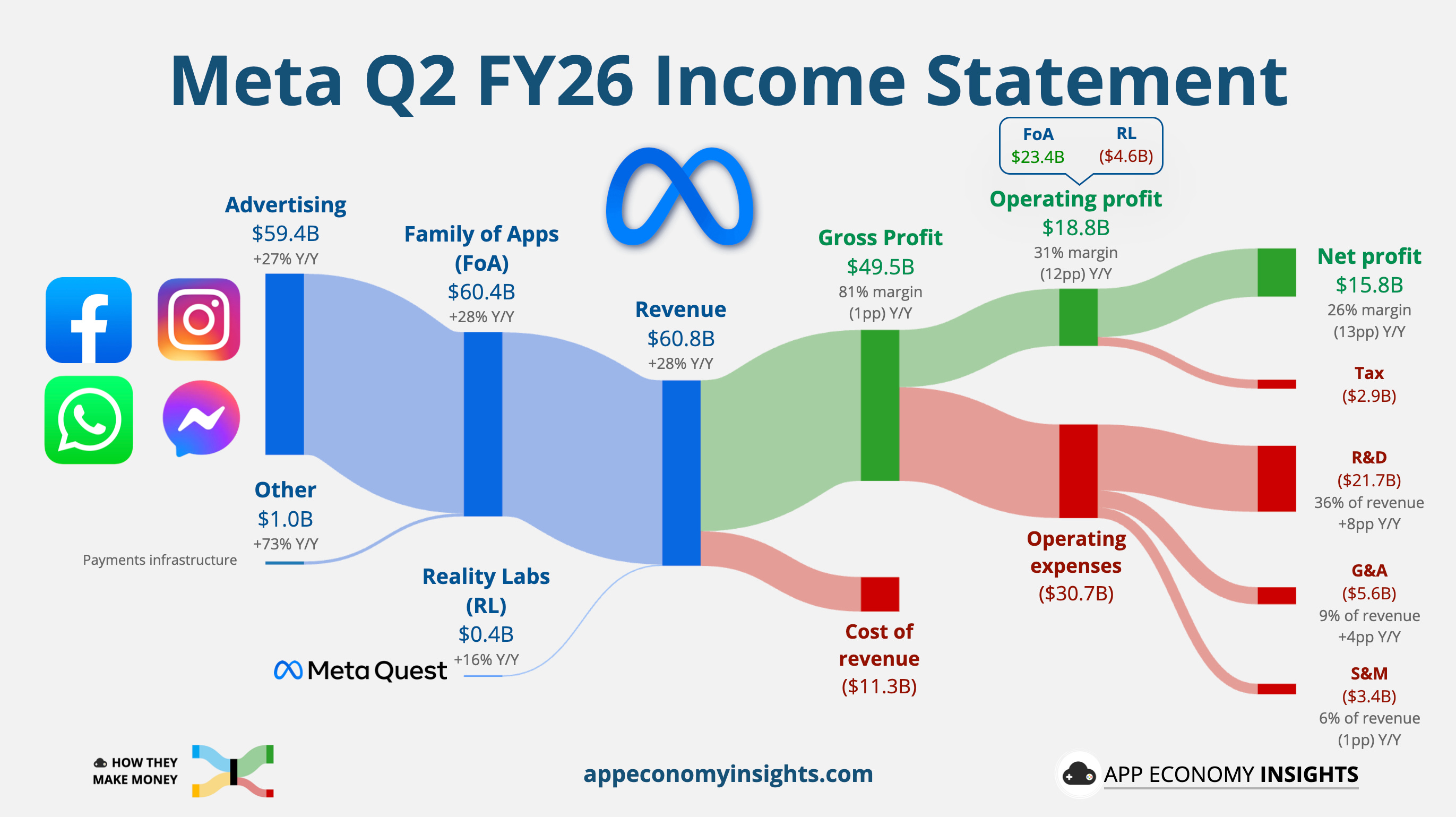

Meta’s Q2 revenue rose 28% Y/Y to $60.8 billion ($0.5 billion beat). GAAP EPS fell 13% to $6.18, but the quarter included $2.4 billion in legal charges related to youth-safety litigation and $1.2 billion in severance costs. Excluding those items, operating income would have risen 9% rather than declined 8%. Despite the underlying beat, shares fell as much as 10%.

The selloff came down to two things:

Free cash flow nearly disappeared. Meta generated $31.9 billion in operating cash flow but spent $31.1 billion on capex and finance leases, leaving just $784 million in free cash flow, down 91% Y/Y. It also issued $24.9 billion of debt and repurchased no stock. Meta can afford the buildout. But for the first time, AI spending has effectively consumed the quarter’s free cash flow, halted buybacks, and pushed the company into the debt market.

The CapEx floor moved higher again. Meta narrowed its FY26 outlook to $130–$145 billion from $125–$145 billion, raising the bottom end for the second consecutive quarter. Its new 1 GW El Paso data center venture shows how it plans to fund the next stage: BlackRock will own 80%, while Meta retains 20% and leases the entire campus. The structure reduces the upfront cash burden without reducing Meta’s long-term commitment.

The irony is that AI is already paying off inside the ad business. Advertising revenue grew 27% Y/Y as impressions increased 14% and average price per ad rose 12%. Meta’s latest models generated an 8% increase in ad clicks and a 16% uplift in Facebook conversions, while Advantage+ products surpassed a $75 billion annual revenue run rate. AI is already producing measurable returns inside the existing business.

Family DAP reached 3.60 billion, Instagram crossed two billion daily users, and Threads surpassed 500 million monthly users. WhatsApp paid messaging and subscriptions also pushed Family of Apps ‘other’ revenue above $1 billion for the first time.

Zuck also offered a more concrete return path than last quarter. Beyond improving ads and engagement, Meta may sell paid model access and lease excess computing capacity. He said outside buyers have offered a “meaningful premium” to Meta’s cost, though building a real cloud business will require distribution and software capabilities Meta does not yet have.

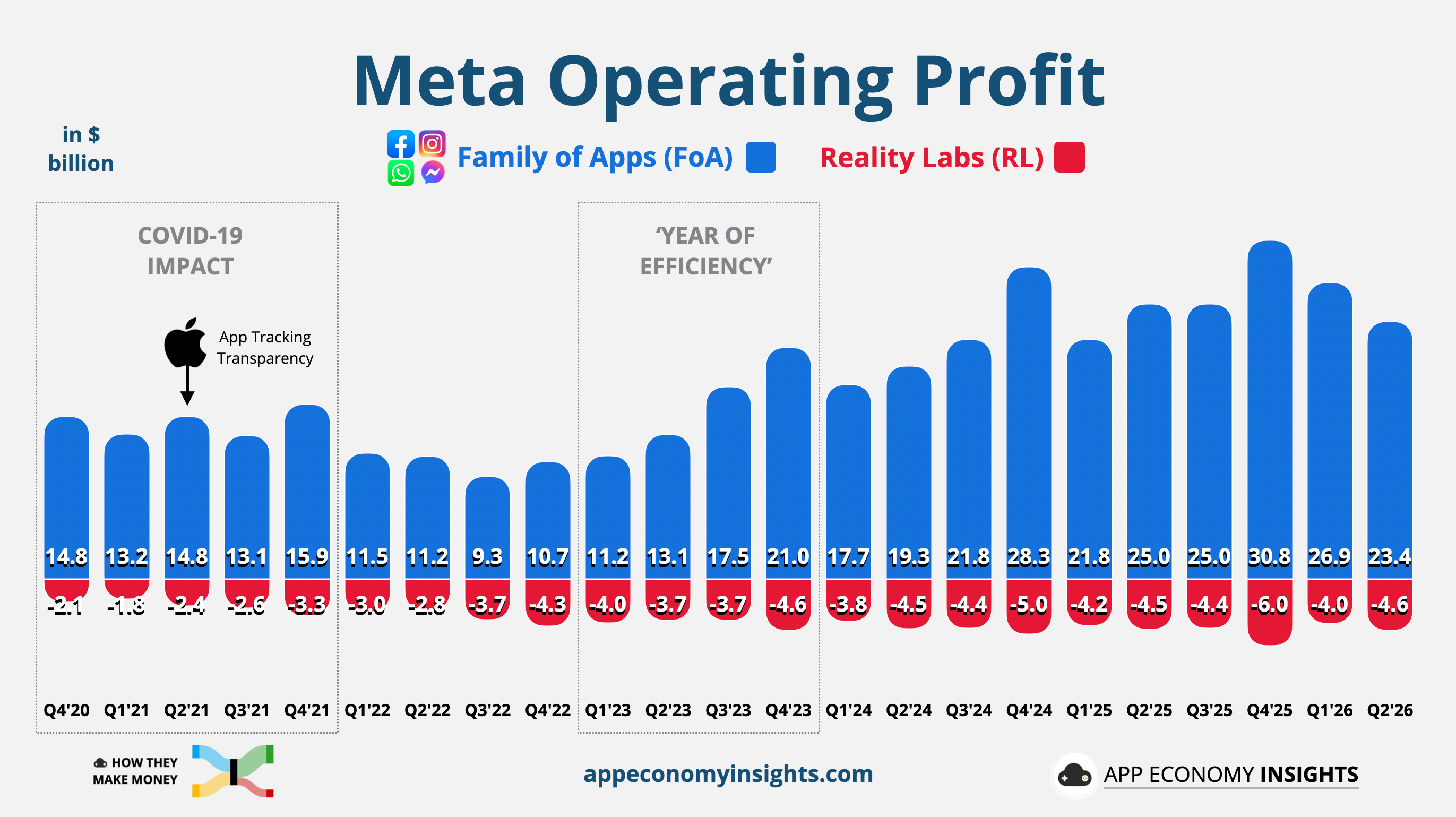

Reality Labs lost another $4.6 billion, while revenue rose 16% on stronger AI-glasses sales.

Meta guided Q3 revenue to $61–$64 billion, with the midpoint below consensus, and raised FY26 expenses to $165–$169 billion. Meta is already earning more from ads, and it now has plausible ways to monetize models and excess compute. The problem is that the spending is arriving all at once, while some of the new revenue streams will take time to meaningfully contribute.

2026-07-31 20:00:43

Welcome to the Free edition of How They Make Money.

Over 300,000 subscribers turn to us for business and investment insights.

In case you missed it:

Amazon plans to spend $220 billion in CapEx this year, up another $20 billion.

And it still won’t be enough. CEO Andy Jassy explained:

“Even at that amount, we will still not have enough capacity to meet all the demand we have in 2026. […] I believe this dynamic will also be true in 2027, too.”

AWS growth accelerated for the fifth consecutive quarter, backlog reached $496 billion, and margins expanded despite the unprecedented buildout.

Amazon has been building the stack for agentic AI. Now, the bet is moving from architecture to economics. Demand is arriving faster than capacity, and Jassy is increasingly confident the returns will justify the spend.

Now let’s see what stood out this quarter.

Today at a glance:

Amazon Q2 FY26.

The economics of the AI stack.

Key quotes from the call.

What to watch moving forward.

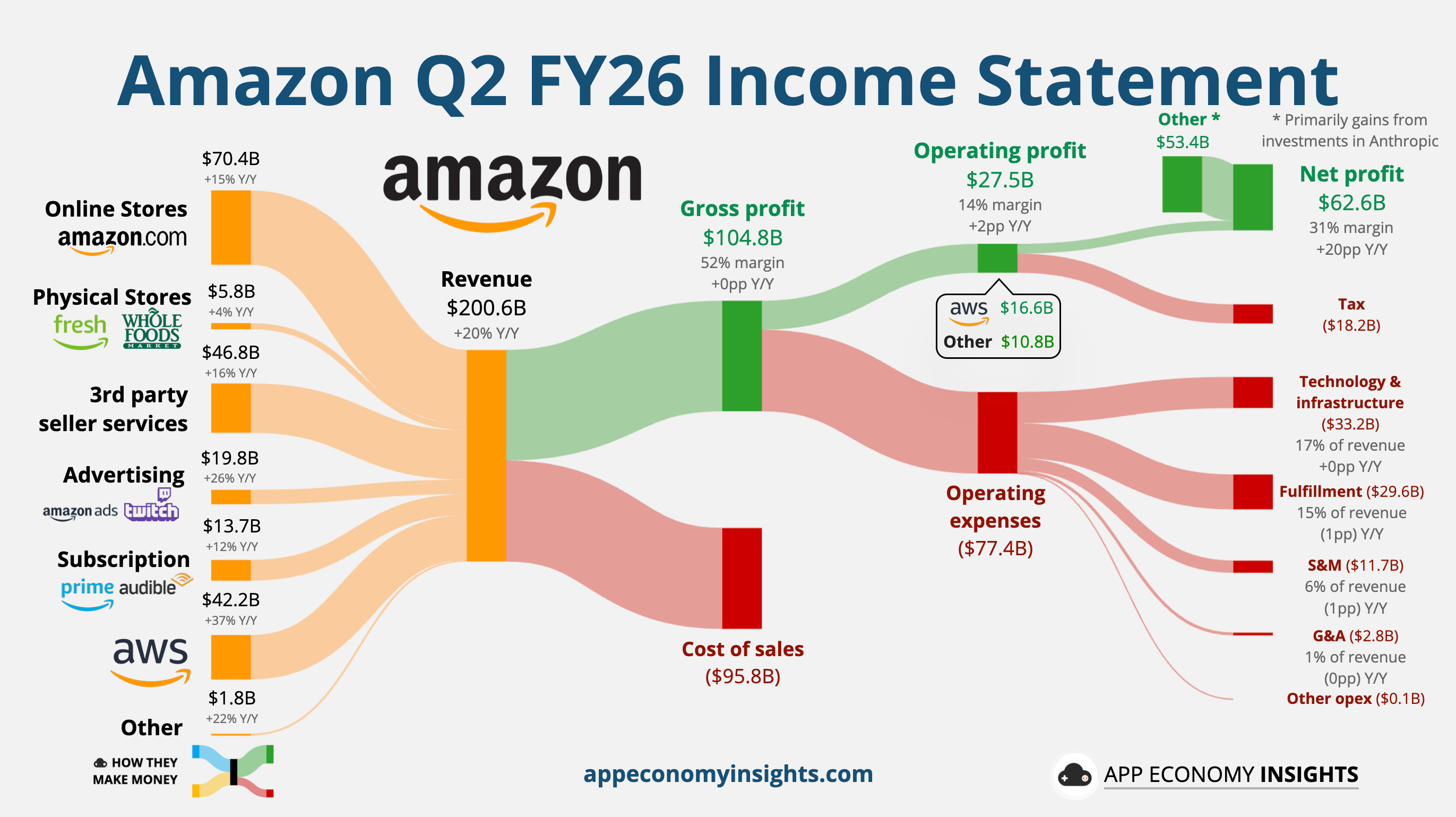

Revenue rose +20% Y/Y to $200.6 billion ($4.2 billion beat).

Gross margin was 52% (+0pp Y/Y).

Operating margin was 14% (+2pp Y/Y).

AWS: 39% margin (+6pp Y/Y).

North America: 8% margin (+0pp Y/Y).

International: 4% margin (+0pp Y/Y).

Net profit included a $53.4 billion non-operating gain, primarily from the valuation markup of Anthropic. The markup followed Anthropic’s $65 billion Series H round in May at a $965 billion valuation, up from $380 billion in February.

Operating cash flow TTM was $161.4 billion (+33% Y/Y).

Free cash flow TTM fell to negative $7.6 billion as a 64% rise in CapEx to $169.0 billion more than offset the growth in operating cash flow.

Cash, cash equivalents, and marketable securities: $123 billion.

Long-term debt: $129 billion.

Revenue +9% to 12% Y/Y.

Operating income of ~$24.5 billion, or +40% Y/Y at the midpoint.

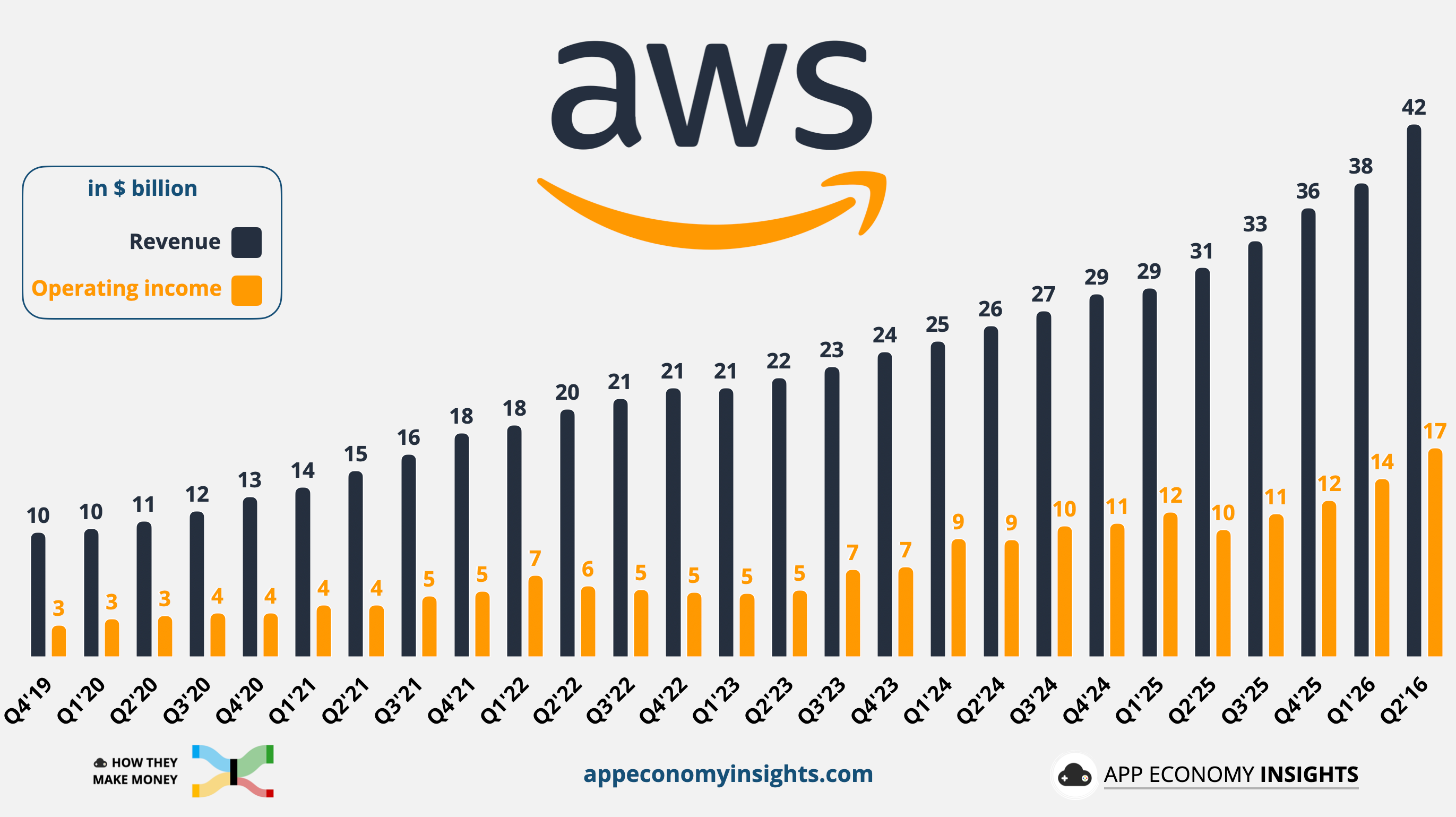

☁️ AWS breaks out: AWS revenue accelerated 37% Y/Y to $42.2 billion, its fastest growth in 18 quarters. AWS operating margin reached 39%. Excluding a $600 million energy-contract accounting gain, it still expanded 520 basis points Y/Y. Meanwhile, Amazon’s AI and custom-chip businesses each surpassed $25 billion annual revenue run rates, both growing triple digits. The chips business was above $20 billion just three months ago. At this scale, accelerating growth and expanding margins at the same time is the quarter’s defining result.

💵 The AI bill is getting larger: Free cash flow swung to a $7.6 billion outflow as CapEx reached $169 billion over the past year. Amazon also raised its 2026 CapEx forecast from $200 billion to $220 billion, primarily because of higher memory costs. Capital spending now exceeds the cash Amazon generates from operations.

📦 Retail volume remains strong: North America revenue grew 16%, International grew 15%, and worldwide paid units increased 17%. North America margin was flat even with a $600 million tariff refund, as higher fuel and transportation costs offset continued fulfillment efficiencies.

📢 Advertising keeps climbing: Revenue grew 26% Y/Y to $19.8 billion, putting the business near an $80 billion annual run rate. Sponsored Products remains the core engine, while Prime Video and live sports are opening new inventory.

🔮 Guidance looks softer than the underlying business: Q3 revenue growth is expected to slow to 9%–12%, but the shift of Prime Day into Q2 reduces the reported growth rate by nearly four percentage points, while foreign exchange creates another 80-basis-point headwind. Operating income is still expected to grow roughly 40% at the midpoint, suggesting Amazon’s margin expansion remains intact.

Jassy finally laid out the math behind Amazon’s massive CapEx ramp.

The spending falls into two different buckets:

Servers and networking equipment: Purchased only a few months before deployment, when Amazon already has visibility into demand. They typically break even in less than three years, while most AI capacity is contracted for at least five.

Data centers: Built roughly two years before monetization, but designed to operate for more than 30 years and support five or six generations of servers.

Most of AWS’s 2027 capacity is already reserved, with meaningful commitments extending into 2028.

The near-term free cash flow pressure is unavoidable, but Amazon is not building on speculation. Much of the equipment is backed by long-term contracts, while the data centers can generate revenue long after the first generation of servers is retired.

AWS is also expanding beyond infrastructure into the software agents running on top of it. Bedrock customers spent more in Q2 than in all previous quarters combined.

Bedrock AgentCore added payments, web search, deterministic controls, and a development harness.

Amazon Quick can now run autonomous workflows across email, calendars, files, and third-party applications.

Kiro, Amazon’s coding agent, tripled usage sequentially.

Continuum uses agents to identify, validate, and remediate software vulnerabilities.

AI is also pulling the core cloud business with it, since post-training and agent tool use rely heavily on CPUs. Trainium and Graviton lower the cost underneath, Bedrock sits at the model and agent layer, and applications such as Quick, Kiro, and Continuum move AWS closer to the end user.

Check out the earnings call transcript on Fiscal.ai here.

“We see the margins and returns in AI tracking what we saw with Core at the same point of evolution, actually a little ahead.”

This directly challenges the assumption that AI workloads will structurally dilute cloud margins. Amazon believes AI economics are developing faster than AWS did in its early years.

“In the middle of the barbell is all of the current enterprise production workloads, some of which are using inference in a pervasive way, but most of which aren't. That is going to change very significantly over time. In my opinion, that will be the largest absolute segment […].”

AI demand is currently barbelled between frontier labs and breakout applications on one side, and narrow enterprise use cases on the other. Jassy believes the middle will eventually become the largest segment: AI embedded across existing production workloads.

“My view of it is that within the next few years, you're going to have at least a half dozen models that are comparably good to each other. [...] They'll all be in Bedrock, one of them will be ours.”

Amazon does not need its model to dominate. Bedrock wins through choice, while an in-house frontier model gives Amazon more control over cost, speed, and product priorities.

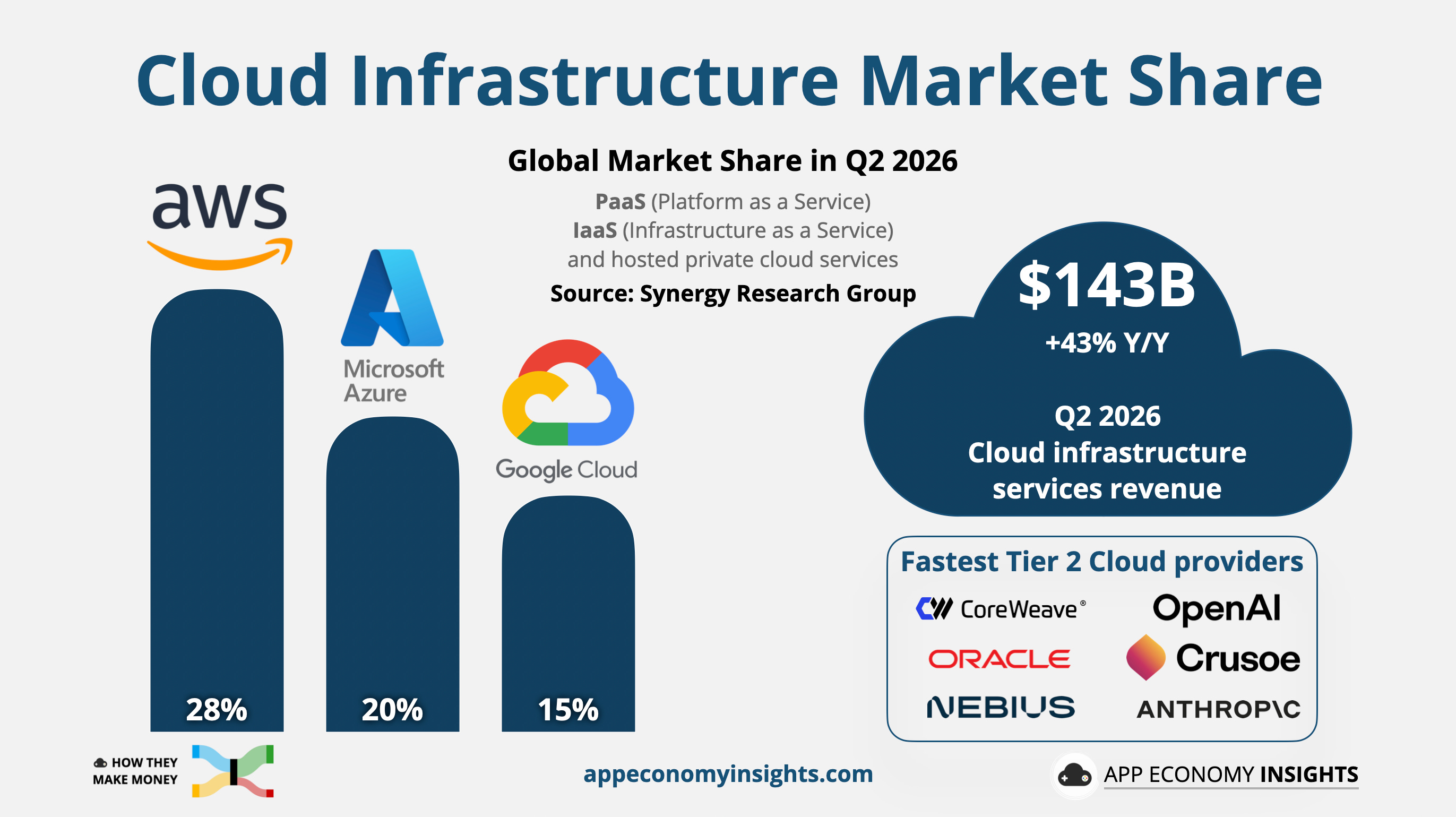

Total cloud infrastructure spending surged 43% Y/Y to $143 billion in Q2, the 11th consecutive quarter of accelerating growth and the fastest pace in eight years. The market has doubled over that period, with GenAI-specific cloud services growing 165% Y/Y, according to Synergy Research Group.

AWS maintained its leading 28% market share, compared to 20% for Microsoft Azure and 15% for Google Cloud. The three platforms now control 63% of the overall cloud infrastructure market, and 67% of public IaaS and PaaS spending.

All hyperscalers remain supply-constrained, so small quarter-to-quarter market-share movements should not be overanalyzed. The bigger story is a broad AI-driven reacceleration. Microsoft and Google are still growing faster, but AWS has held its 28% share while accelerating from a much larger revenue base.

Amazon is exploring selling Trainium chips separately to customers operating their own data centers. That could turn Trainium from an AWS-exclusive advantage into a merchant-chip business, expanding Amazon’s addressable market beyond the cloud.

The trade-off is whether selling Trainium more broadly weakens one of AWS’s clearest cost and performance advantages.

Amazon now offers same-day perishables in 2,300 US cities. Monthly active perishables customers have increased 50% since the start of the year, while orders containing perishables average three times as many units.

The opportunity extends beyond grocery revenue. Grocery can increase purchase frequency, basket size, delivery density, and advertising inventory at the same time.

In Q2 2026, the leading hyperscalers grew their trailing-12-month operating cash flow by 34% to $660 billion.

That cash engine allowed Big Tech to begin the AI buildout without relying heavily on outside capital. But the scale of investment has now caught up: free cash flow has turned negative at Amazon and Google and fallen close to zero at Meta. The next phase is already pulling more debt into the equation. Amazon issued debt this year and says it will continue evaluating its funding options (in Alphabet’s case, that includes equity issuance).

Amazon argues this is a timing mismatch rather than a deterioration in economics. It is spending years ahead of demand, while the resulting infrastructure could generate revenue for decades. If Jassy is right, today’s free-cash-flow collapse is the price of locking in tomorrow’s capacity. If demand, pricing, or utilization disappoints, that operating leverage works in reverse.

Next up: Saturday’s massive PRO edition, with more than 30 companies visualized.

That’s it for today!

Stay healthy and invest on!

Thanks to Fiscal.ai for being our official data partner. Create your own charts and pull key metrics from 50,000+ companies directly on Fiscal.ai. Start an account for free and save 15% on paid plans with this link.

Disclosure: I am long AMZN, GOOG, META, and MSFT in App Economy Portfolio. I share my ratings (BUY, SELL, or HOLD) with members.

Author's Note (Bertrand here 👋🏼): The views and opinions expressed in this newsletter are solely my own and should not be considered financial advice or any other organization's views.

2026-07-30 07:22:01

Welcome to the Premium edition of How They Make Money.

Over 300,000 subscribers turn to us for business and investment insights.

In case you missed it:

Jensen Huang used his first-ever X post last week to enter Washington’s fight over open-weight AI. He shared an open letter initially signed by 25 companies, including Microsoft, Meta, and Palantir. The coalition urged policymakers to preserve the development and deployment of open-weight models.

Satya Nadella quickly amplified the message, arguing that openness is essential to a healthy AI ecosystem.

To understand why the industry is clashing over this policy, it helps to distinguish how AI software is delivered:

Closed models (proprietary): The model’s internal weights remain locked behind an API. Companies such as OpenAI and Anthropic control the security guardrails, computing infrastructure, and pricing.

Open-weight models: The pre-trained weights can be downloaded and inspected. Businesses can customize and host the software on their own infrastructure without paying every query fee to a single vendor.

The immediate catalyst is model distillation, where developers use outputs from leading closed models to train cheaper alternatives. It is the same concern behind US accusations that Chinese lab Moonshot AI used a leading American model to improve Kimi. Closed-model providers argue that unrestricted distillation amounts to intellectual-property theft. Supporters of open weights see it as part of the competitive process that lowers costs and broadens access.

OpenAI, Anthropic, and Google were initially absent from the letter. OpenAI later joined after Sam Altman said he wanted the US to lead in both open and closed models, while Google’s Sundar Pichai endorsed the effort on the company’s behalf. Anthropic remained the clearest holdout, arguing that it does not want to ban open models but supports stricter chip controls, action against industrial-scale distillation, and mandatory safety testing for all capable systems.

NVIDIA reinforced the campaign this week by launching the Open Secure AI Alliance, a coalition of nearly 40 companies building tools to defend against AI-powered cyberattacks. Microsoft, SpaceX, and IBM are founding members. Anthropic, OpenAI, and Meta are notably absent.

The policy fight matters because Microsoft is hedging both outcomes. It maintains a multibillion-dollar closed-model alliance with OpenAI while positioning Azure as the indispensable platform for open-weight deployment. Microsoft does not need to predict which model architecture wins. It wants to provide the compute, governance, and security layer underneath all of them.

In this Q4 breakdown (June quarter), we analyze how that strategy is playing out.

Today at a glance:

Microsoft’s Q4 FY26.

The sovereignty play.

Earnings call takeaways.

What moves the needle?

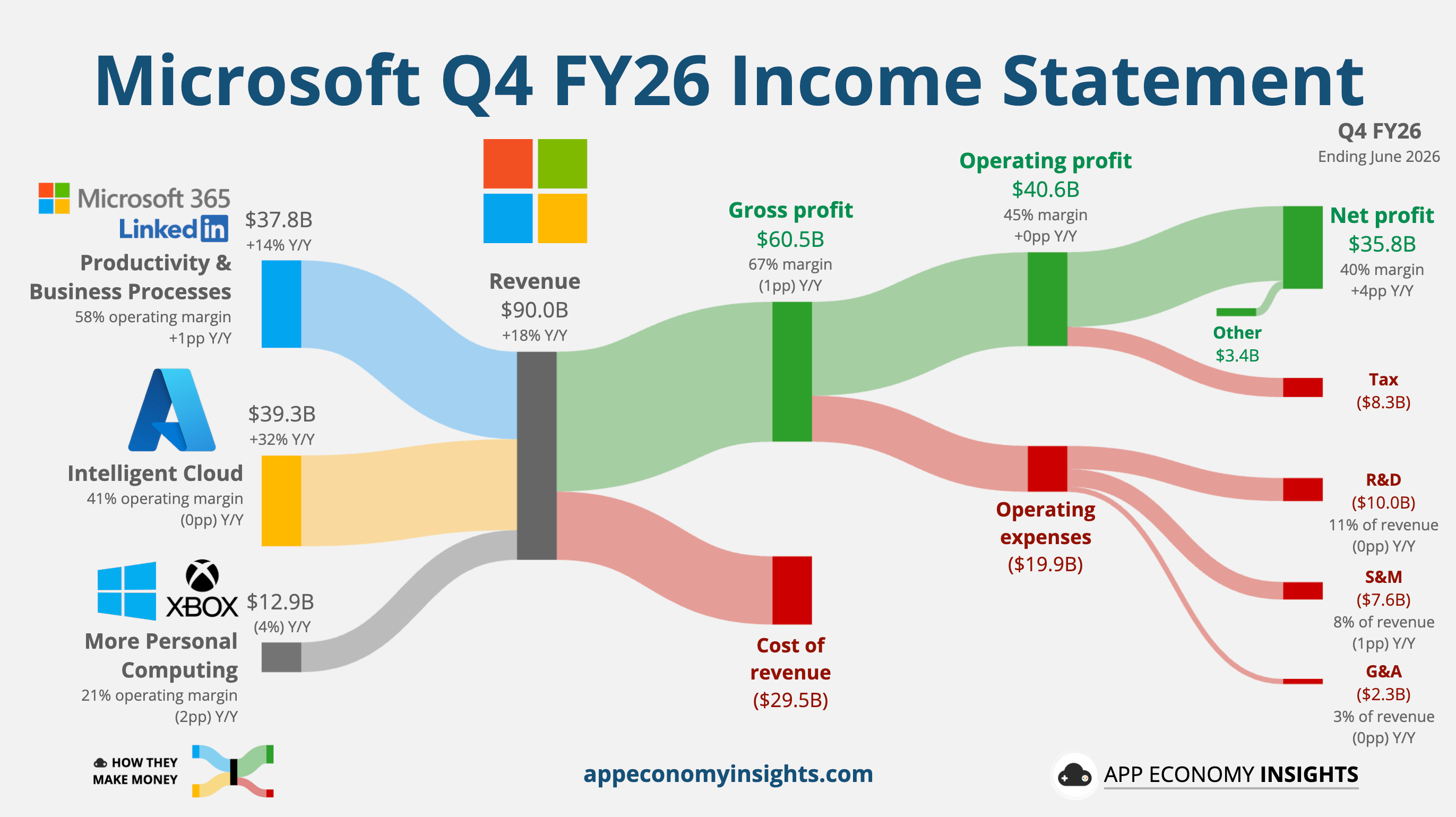

Revenue +18% Y/Y to $90.0 billion ($2.4 billion beat).

Gross margin 67% (-1pp Y/Y).

Operating margin 45% (flat Y/Y).

Non-GAAP EPS $4.74 ($0.50 beat).

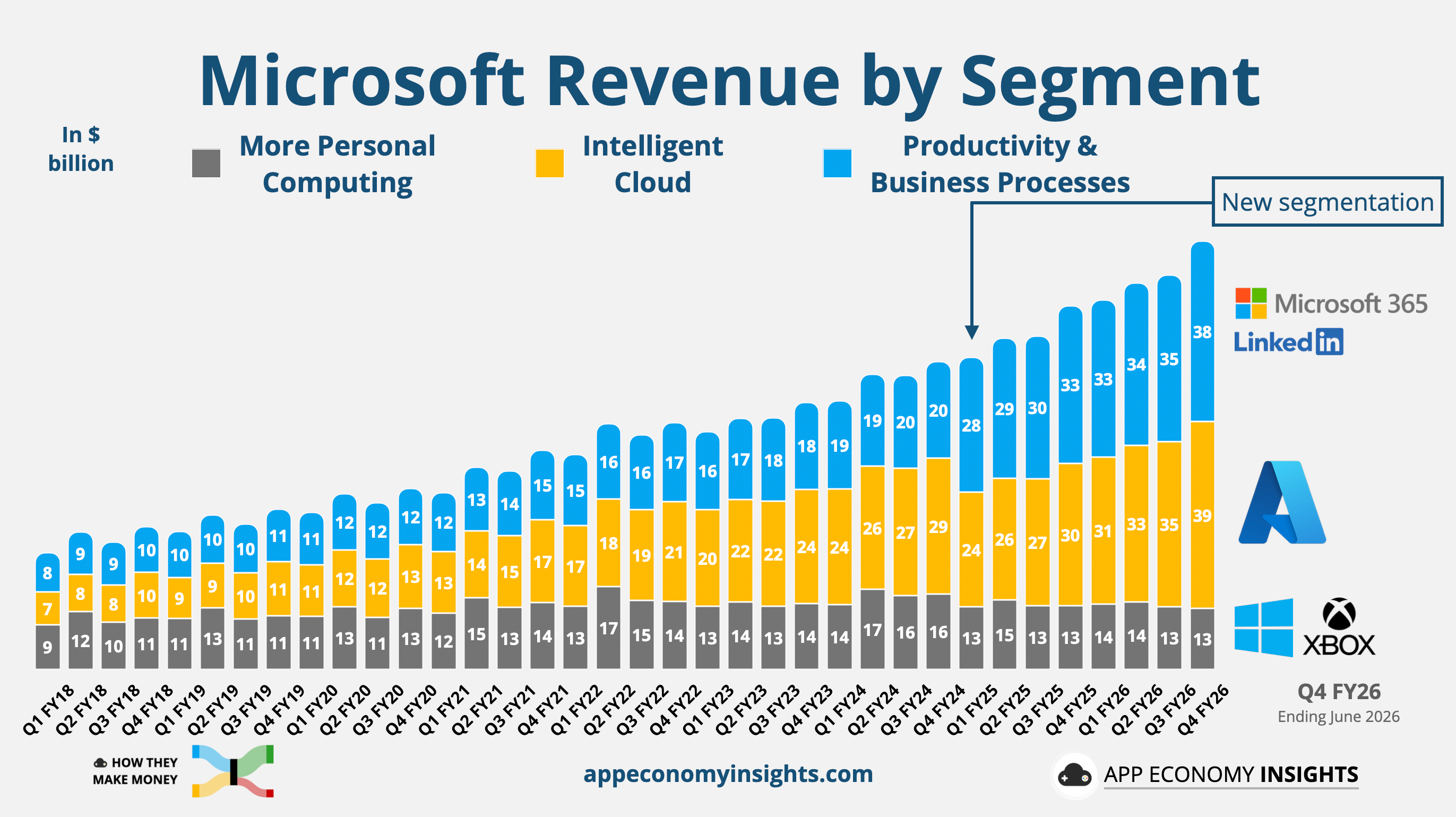

📊 Productivity and Business Processes grew 14% Y/Y to $37.8 billion, supported by M365 Copilot, E5, and early E7 momentum, alongside stronger M365 commercial products revenue.

☁️ Intelligent Cloud grew 32% Y/Y to $39.3 billion, driven by 43% Azure growth as Microsoft improved fleet efficiency and brought new capacity online faster.

🎮 More Personal Computing declined by 4% Y/Y to $12.9 billion, as weaker Windows OEM and Xbox revenue outweighed 10% growth in Search advertising.

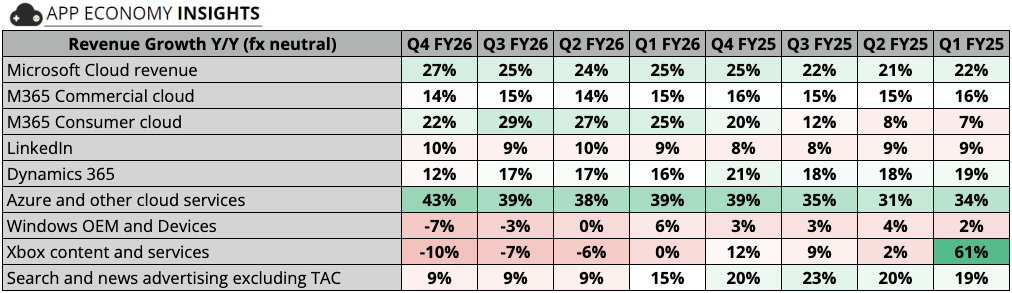

The table below compares growth year-over-year in constant currency. Some of the products and services overlap.

Operating cash flow grew 30% Y/Y to $55.4 billion.

Free cash flow declined by 23% Y/Y to $19.6 billion.

Cash, cash equivalents, and investments: $76.8 billion.

Long-term debt: $31.1 billion.

2026-07-25 22:01:25

Welcome to the Saturday PRO edition of How They Make Money.

Over 300,000 subscribers turn to us for business and investment insights.

In case you missed it:

📊 Monthly reports: 200+ companies visualized.

📩 Tuesday articles: Exclusive deep dives and insights.

📚 Access to our archive: Hundreds of business breakdowns.

📩 Saturday PRO reports: Timely insights on the latest earnings.

Today at a glance:

🏭 Intel: Fifteen-Year High

⚡ GE Vernova: Capacity Bet

⚙️ Texas Instruments: Pricing Lever

💳 Amex: Platinum Premium

📶 T-Mobile US: Momentum Cools

🌐 IBM: Mainframe Air Pocket

📡 Verizon: Subsidy Pullback

🏦 Schwab: The Volatility Dividend

📞 AT&T: Volume Over Price

🛰️ Lockheed Martin: The Missile Surge

🧑💻 ServiceNow: Growth Without Credit

💼 Moody’s: Volume Over Mix

🚗 GM: Pricing Over Volume

🍕 Domino’s: Ticket Miss

🦅 American Airlines: Fuel Eats The Record

🍿 AMC: The Odyssey Delivers

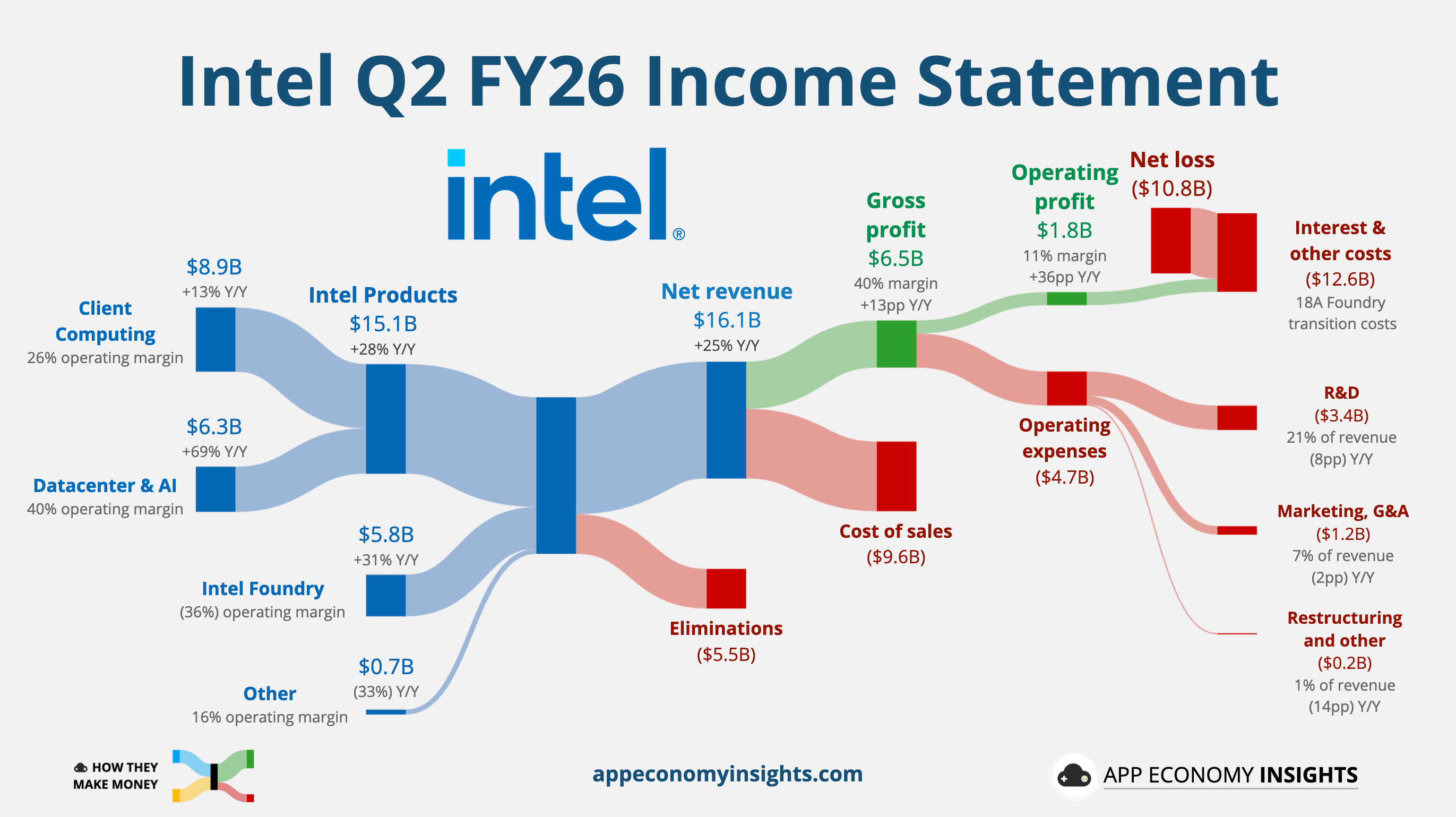

Intel’s Q2 revenue rose 25% Y/Y to $16.1 billion ($1.7 billion beat), and non-GAAP EPS was $0.42 ($0.20 beat), against a $0.10 loss a year ago. CEO Lip-Bu Tan called it the strongest revenue growth in more than fifteen years.

Intel lost $10.8 billion on paper because its own stock price went up so fast that it made the free shares it promised the US government way more expensive to give away. INTC has nearly tripled this year but sits close to 30% below its June 22 high. The stock was caught in a sector-wide rotation out of chip stocks as Wall Street questions whether AI hardware spending is sustainable.

Data Center and AI revenue climbed 59% Y/Y to $6.3 billion, more than double Intel’s overall growth rate, as agentic workloads pull the stack back toward CPUs.

Client Computing rose 13% Y/Y to $8.9 billion against an $8.0 billion consensus, with AI PCs now two-thirds of the client mix.

Foundry grew 31% Y/Y to $5.8 billion, accelerating from 16% last quarter, and adjusted gross margin hit 41.8%, roughly 280 basis points above guidance.

CFO Dave Zinsner said rising memory prices will hit the PC business in the coming quarters, and management already expects sub-seasonal PC consumption in the second half. Intel is spending into that anyway, raising 2026 CapEx from $18 billion to more than $20 billion. Management expects 2027 CapEx to be significantly higher. Foundry's growth is still mostly internal. The segment sells almost entirely to Intel's own product groups, and CEO Lip-Bu Tan wouldn't name external customers, pointing to early next year for visible progress.

Q3 guidance of $15.8–16.8 billion implies a midpoint roughly $1.2 billion above consensus, with EPS of $0.38 (vs. ~$0.27 expected) and gross margin of 42% (vs. ~40% consensus). Zinsner said Intel can sell every data center chip it makes, 18A yields are running ahead of plan, and 14A will move to volume production in 2028. Client Computing is the segment to watch in Q3, when higher memory costs hit PC pricing.