2026-05-29 23:00:42

Welcome to HackerNoon’s Projects of the Week, where we spotlight standout projects from the Proof of Usefulness Hackathon, HackerNoon’s competition designed to measure what actually matters: real utility over hype. \n \n Each week, we’ll highlight projects that demonstrate clear usefulness, technical execution, and real-world impact - backed by data, not buzzwords.

This week, we’re excited to share three projects that have proven their utility by solving concrete problems for real users: Yaeum, XColdPro, and EquipmentStack.

\

:::tip Want to see your own project spotlighted here?

Join the Proof of Usefulness Hackathon to get on our radar.

:::

Yaeum is an innovative language learning app that allows fans of K-pop and K-drama to learn Korean directly from their favorite content using generative AI and machine learning.

Search for a Korean song, drama, or movie, and Yaeum will provide an in-depth analysis of the text, sentence by sentence, and set up a personalized vocabulary list to make memorizing new words easy. To achieve this, Yaeum taps into several open sources third party apis and uses generative AI and machine learning to analyze the texts and provide grammatical explanations as well as vocabulary.

Proof of Usefulness score: +74 / 1000

\

\

:::tip See Yaeum’s full Proof of Usefulness report

Read their story on HackerNoon

:::

XColdPro is a patent-pending, hardware-agnostic cold storage software designed to protect both cryptocurrency keys and the host machine holding them, solving critical issues around digital asset inheritance and OS-level threat defense.

XColdPro leverages Python and Electron to deliver a cross-platform experience, secured by robust AES-256-GCM encryption and PBKDF2 with 500K iterations. The tech stack is uniquely built to operate in a fully air-gapped, no-cloud environment, while utilizing scheduled task watchdog architecture and OS-level behavioral monitoring to seamlessly integrate threat intelligence.

Proof of Usefulness score: +52 / 1000

\

\

:::tip See XColdPro’s full Proof of Usefulness report

Read their story on HackerNoon

:::

EquipmentStack is a newly launched, niche content platform focused on detailed athlete equipment specifications. The platform helps enthusiasts find exactly what the pros use, diving into the labor-intensive data gathering that earned them their recent Proof of Usefulness score.

To build and manage its extensive content repository, EquipmentStack utilized WordPress as its foundational technology. Choosing WordPress allowed it to rapidly deploy a custom, SEO-friendly site that is perfectly suited for managing a highly structured database of gear and athletes without unnecessary technical overhead.

While the project is in its infancy with no verifiable user traction yet, the live site demonstrates high-quality, labor-intensive data gathering that offers genuine utility to enthusiasts.

Proof of Usefulness score: +35 / 1000

\

:::tip See EquipmentStack’s full Proof of Usefulness report

Read their story on HackerNoon

:::

It's our answer to a web drowning in vaporware and empty promises. We evaluate projects based on: \n ▪️ Real user adoption \n ▪️ Sustainable revenue \n ▪️ Technical stability \n ▪️ Genuine utility

Test your project’s usefulness and submit your report on Hackernoon before August 10, 2026, to compete for over $150,000 in cash prizes and software credits.

Projects score from -100 to +1000. Top scorers compete for $20K in cash and $130K+ in software credits.

You’ll be in good company. The hackathon is backed by teams who ship production software for a living - Bright Data, Neo4j, Storyblok, Algolia, and HackerNoon.

\

\

1. Get your free Proof of Usefulness score instantly \n 2. Your submission becomes a HackerNoon article (published within days) \n 3. Compete for monthly prizes \n 4. All participants get rewards

Complete guide on how to submit here.

:::tip 👉 Submit Your Project Now!

:::

\ That’s all for now.

Until next time, Hackers!

2026-05-29 22:59:59

AI is not a great equalizer. It is a great amplifier. It amplifies what you already are — for better and for worse.

2026-05-29 22:29:59

Now remember how PCA collapses data with 100 dimensions into a single dimension, wouldn't it be cool if this dimension was interpretable. For example, let's say the 100 columns were like stress, smoking frequency, alcohol ml etc etc.. you see where I am going with this, the final dimension would be something like cardiac arrest or premature demise. On that cheery note, let's figure out how PCA can actually be used to label this reduced dimension.

2026-05-29 22:16:00

For most people, the US immigration system feels like a black box. You submit documents, you wait and you hope. The rules shift without warning. The timelines stretch. The costs climb. And if something goes wrong, figuring out why can take months and thousands of dollars in legal fees.

Swatilina Barik decided that did not have to be the case.

A seasoned practitioner with 10+ years of hands-on experience inside immigration strategy, Barik has spent considerable time watching the same problems repeat themselves. Applicants arriving underprepared. Petitions filed with gaps that could have been caught early. Strategies chosen not because they were the best fit but because they were the most familiar. She did not see a system that needed a few upgrades. She saw one that needed to be rethought entirely.

That rethinking led to Visa Architect.

US immigration is not a single pathway. It is a sprawling web of visa categories, eligibility criteria, processing timelines and adjudication patterns that shift depending on country of origin, employer size, job role and a dozen other variables. Navigating it well has always required deep expertise and deep expertise has always been expensive.

Visa Architect changes that equation. The platform uses artificial intelligence to do what the best immigration strategists do but at a scale and speed that was not previously possible. It analyzes an applicant's profile, maps it against relevant visa categories, identifies potential weaknesses in a petition before it is filed and models how different approaches might play out given current adjudication trends.

The result is not just faster processing. It is smarter decision-making from the very beginning of the immigration journey.

There is no shortage of technology companies trying to automate legal processes. What makes Barik's approach different is where she started. She did not come to immigration as an outsider looking to apply a general-purpose AI tool to a new market. She came as someone who had already spent years inside the system, learning what actually trips applications up and what actually gets them approved.

That practical knowledge is embedded in Visa Architect in ways that a purely data-driven approach would miss. The platform understands not just the rules but the context around the rules. It reflects the kind of judgment that experienced practitioners develop over years and makes it accessible to a much wider range of users.

The impact of Visa Architect reaches across the immigration ecosystem.

For individual applicants, it means entering the process with a clearer picture of where they stand. They can understand which visa pathway is genuinely the strongest fit for their circumstances rather than defaulting to whatever their employer used for the last hire. They can see potential red flags in their documentation before a case officer does. They can make informed choices rather than hoping for the best.

For businesses, particularly smaller companies that lack dedicated immigration teams, it means access to a level of strategic analysis that was previously out of reach. A startup sponsoring its first international employee no longer has to navigate the process blind.

For immigration attorneys, Visa Architect is not a replacement. It is a resource. It handles the research-heavy analytical work that consumes hours of preparation time, freeing practitioners to focus on the judgment calls, the nuanced arguments and the client relationships where human expertise is irreplaceable.

What Barik is building points to something larger than a single platform. It reflects a fundamental shift in how AI can and should be applied to high-stakes professional fields.

For years the dominant approach was to automate simple tasks and leave complex ones to humans. What Visa Architect demonstrates is that AI built on deep domain knowledge can take on genuinely complex work, not by replacing human judgment but by expanding who has access to informed guidance in the first place.

The US immigration system is not going to get simpler. Policy changes, backlogs and evolving adjudication standards are a permanent feature of the landscape. But the tools people use to navigate that landscape are changing. Swatilina Barik is building some of the most important ones. \n

:::tip This story was distributed as a release by Sanya Kapoor under HackerNoon’s Business Blogging Program.

:::

\

2026-05-29 22:00:59

How are you, hacker?

🪐Want to know what's trending right now?:

The Techbeat by HackerNoon has got you covered with fresh content from our trending stories of the day! Set email preference here.

## What is Predictive Software Quality? Software Operations in the AI Era  By @playerzero [ 8 Min read ]

PlayerZero explains how predictive software quality helps enterprises prevent defects, reduce firefighting, and scale reliable software development with AI. Read More.

By @playerzero [ 8 Min read ]

PlayerZero explains how predictive software quality helps enterprises prevent defects, reduce firefighting, and scale reliable software development with AI. Read More.

By @scylladb [ 4 Min read ] New research reveals why companies ignore database risks until costs, latency, or outages force migrations—and what warning signs to watch. Read More.

By @tsivarev [ 7 Min read ] Where AI helps in ecosystem design, where it fails, and why human judgment must stay in the loop for trust, grants, reputation, and governance. Read More.

By @modulate [ 10 Min read ] Deepfake vishing surged 1600% in 2025. Most detection tools analyze text, not audio — and miss what matters. Here's how voice-native detection actually works. Read More.

By @webintelligencehub [ 7 Min read ] IP pool size is a marketing number. Learn which metrics matter when evaluating proxy providers, and what to look for on their websites before you spend a dollar Read More.

By @zbruceli [ 21 Min read ] Inside the biological tricks that let three-pound brains outlearn trillion-parameter machines — and the radical new architectures trying to close the gap Read More.

By @akashi-ghost [ 11 Min read ] AI is not alien or fake intelligence. It is accumulated human thought, culture, code, bias, and memory reflected back through machines. Read More.

By @macpaw [ 5 Min read ] MacPaw Research explains why macOS is severely underrepresented in public AI datasets and introduces GUIrilla, a framework for scalable Mac UI exploration. Read More.

By @arthurlazdin [ 6 Min read ] UB isn't a dark corner of C. It's what happens when a program steps outside its computational model — and the compiler, a perfect executor, follows the math. Read More.

By @syedahmershah [ 8 Min read ] I put Nous Research's hot new Hermes Agent framework through 5 brutal, multi-step tasks to see if it actually self-improves or just fails silently. Read More.

By @kumar96 [ 7 Min read ] Creating third-party integration is not a problem in OutSystems. It talks about web services, OAuth, and other security in APIs Read More.

By @joseh [ 4 Min read ] Kenshi and Kintaro are just a few of the characters that should be in Mortal Kombat 3. Read More.

By @mattleads [ 15 Min read ] A practical, working demonstration of 7 advanced Doctrine ORM strategies to eliminate the N+1 query problem in Symfony applications. Read More.

By @bennydoda [ 5 Min read ] AI agents will move so fast in establishing decentralised ecosystems for trading that regulators won't know where to start Read More.

By @notllmhallucination [ 12 Min read ] A review of context and memory issues in LLMs against the methods of AI startups to solve these in biological or biology-mimicking ways. Read More.

By @efimovov_5guqm5 [ 7 Min read ] MCP servers connect Claude Code to external tools. Use scopes correctly, keep credentials in env vars, and run mcp-scan on every new server. Read More.

By @huckler [ 7 Min read ] My system monitor with its own 9-layer AI between €3.8/h retail shifts. 55 GitHub stars, 260 downloads, 10 months solo. Here's everything it does. PC Workman. Read More.

By @qatech [ 7 Min read ] Learn how AI-generated code is shifting software QA toward continuous verification, agentic testing, and context-aware product quality systems. Read More.

By @vladlensk1y [ 4 Min read ] How I use AGENTS.md and a GitHub Action to catch low-effort AI-generated PRs before wasting maintainer review time. Read More.

By @apilayer [ 4 Min read ]

Discover 7 of the best SERP APIs for SEO and market research in 2026. Read More.

🧑💻 What happened in your world this week? It's been said that writing can help consolidate technical knowledge, establish credibility, and contribute to emerging community standards. Feeling stuck? We got you covered ⬇️⬇️⬇️

ANSWER THESE GREATEST INTERVIEW QUESTIONS OF ALL TIME

We hope you enjoy this worth of free reading material. Feel free to forward this email to a nerdy friend who'll love you for it.

See you on Planet Internet! With love,

The HackerNoon Team ✌️

.gif)

2026-05-29 22:00:46

Where founders share what they learn on the go. Read founder-related content: everything from challenges, success stories, leadership tips, to experiments.

In this interview we speak with Alex Busarov the co-founder of Taelpay about Taelpay ecosystem a blockchain application developed by the team while operating in China. Tael consists of over

50,000 users in 500 cities, hundreds of products protected with NFC chips and

blockchain, all in cooperation with a long list of participating companies like Rakuten,

Nestlé, New Zealand Cherry Corp,and many more. The Tael ecosystem is anchored by

the Tael token which acts as a reward, loyalty, and marketing incentive for

participants in the ecosystem. Now lets delve straight into the interview!

In this interview we speak with Alex Busarov the co-founder of Taelpay about Taelpay ecosystem a blockchain application developed by the team while operating in China. Tael consists of over

50,000 users in 500 cities, hundreds of products protected with NFC chips and

blockchain, all in cooperation with a long list of participating companies like Rakuten,

Nestlé, New Zealand Cherry Corp,and many more. The Tael ecosystem is anchored by

the Tael token which acts as a reward, loyalty, and marketing incentive for

participants in the ecosystem. Now lets delve straight into the interview!

Why Even Track Your Habits?

Why Even Track Your Habits?

It might be surprising to some, but even non-technical startup founders have been behind great tech products like Tinder and AirBnB without the usual background

It might be surprising to some, but even non-technical startup founders have been behind great tech products like Tinder and AirBnB without the usual background

A successful pitch starts with a well-thought-out pitch deck. And the "Why now" section is arguably one of the most important aspects of that deck.

A successful pitch starts with a well-thought-out pitch deck. And the "Why now" section is arguably one of the most important aspects of that deck.

An exit strategy is often developed at an early stage and outlined in a business plan so that investors understand how they will receive a return of investments

An exit strategy is often developed at an early stage and outlined in a business plan so that investors understand how they will receive a return of investments

OpenAI cofounder and chief scientist Ilya Stuskever talks about ChatGPT and the promise of models like GPT-4

OpenAI cofounder and chief scientist Ilya Stuskever talks about ChatGPT and the promise of models like GPT-4

Entrepreneurship definitely is one of the most misconceived terminologies of the era. It seems like a mountain of tasks to start a business. When we think of all the time, money, and risks involved, it’ just seems so inaccessible to a regular man or woman.

Entrepreneurship definitely is one of the most misconceived terminologies of the era. It seems like a mountain of tasks to start a business. When we think of all the time, money, and risks involved, it’ just seems so inaccessible to a regular man or woman.

In this Slogging thread, we talk to Jay Wey the Co-founder of Ubiik and social media influencer behind jayandsharon.

In this Slogging thread, we talk to Jay Wey the Co-founder of Ubiik and social media influencer behind jayandsharon.

A biological marvel, the human itself known as homo sapiens. In the Latin language, it stands for a wise man. A wise man that survived about 200,000 years of evolution and extinction. There are many perspectives towards its survival and today I would like to share my perspective, slightly vague but different. There is a concept of what drives you that has become popular within the last decade. Certain presumptions about the driving force are based upon raw emotional aspects such as passion and rage. I find to myself that these aspects are reactions to our stubbornness to keep on going on but the negative aspect is that these reactions are short-lived and eventually man settles with peace. I would like to share a certain experience in a short period of my life that has produced results beyond my expectations. It is a small story of how I created my IoT Device converted into a product and made a company out of it.

A biological marvel, the human itself known as homo sapiens. In the Latin language, it stands for a wise man. A wise man that survived about 200,000 years of evolution and extinction. There are many perspectives towards its survival and today I would like to share my perspective, slightly vague but different. There is a concept of what drives you that has become popular within the last decade. Certain presumptions about the driving force are based upon raw emotional aspects such as passion and rage. I find to myself that these aspects are reactions to our stubbornness to keep on going on but the negative aspect is that these reactions are short-lived and eventually man settles with peace. I would like to share a certain experience in a short period of my life that has produced results beyond my expectations. It is a small story of how I created my IoT Device converted into a product and made a company out of it.

We skipped last year, but this year SparkLabs Group is back with our fourth

rankings and report of the Top Ten Startup Ecosystems in the World.

We skipped last year, but this year SparkLabs Group is back with our fourth

rankings and report of the Top Ten Startup Ecosystems in the World.

In the venture capital ecosystem, there's a persistent allure for formulas, models, and hard data that investors routinely rely upon…

In the venture capital ecosystem, there's a persistent allure for formulas, models, and hard data that investors routinely rely upon…

It's possible for a solo developer to build a profitable microstartup to pay the bills and live life on their own terms.

It's possible for a solo developer to build a profitable microstartup to pay the bills and live life on their own terms.

Startup founders, here's how to get featured on HackerNoon! This startup founder interview template is based on David Smooke’s ten founder questions.

Startup founders, here's how to get featured on HackerNoon! This startup founder interview template is based on David Smooke’s ten founder questions.

a Newsletter and Reached The

Top of the Fitness Industry](https://hackernoon.com/how-fitt-insider-started-with-a-newsletter-and-reached-the-top-of-the-fitness-industry)

When it comes to building a successful business, the journey of Anthony Vennare, co-founder of Fitt Insider, offers invaluable insights. From leveraging persona

When it comes to building a successful business, the journey of Anthony Vennare, co-founder of Fitt Insider, offers invaluable insights. From leveraging persona

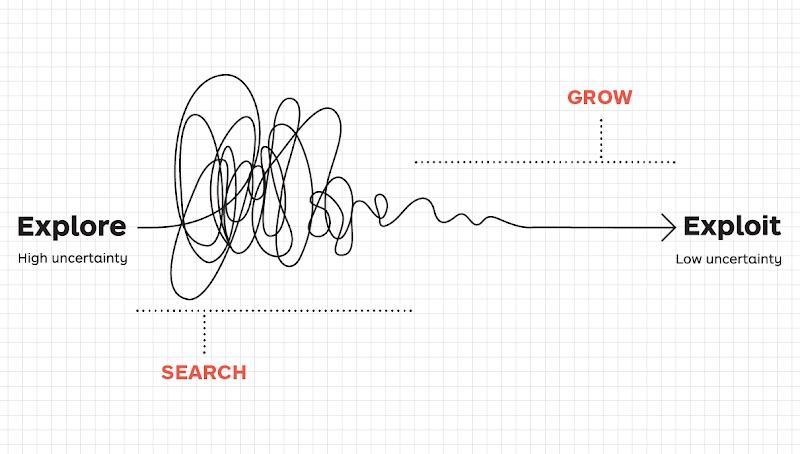

Startups need to strike a balance between seeking new opportunities and maximizing the existing ones.

Startups need to strike a balance between seeking new opportunities and maximizing the existing ones.

Ten stories of Ukrainian founders on leading Web3 companies during the war and bear market: relocation, working under sirens, distress, and raising capital.

Ten stories of Ukrainian founders on leading Web3 companies during the war and bear market: relocation, working under sirens, distress, and raising capital.

What's Your Background, and How Did That Lead You to Your Current Role?

What's Your Background, and How Did That Lead You to Your Current Role?

MeMemes is a mobile app that uses AI to transform people into over 30 famous meme images.

MeMemes is a mobile app that uses AI to transform people into over 30 famous meme images.

How to build a start-up or product MVP without coding

How to build a start-up or product MVP without coding

Yusuf Sevim discusses MetaTime's revolutionary journey to fuse the real and digital using cutting-edge blockchain tech, emphasizing speed and security.

Yusuf Sevim discusses MetaTime's revolutionary journey to fuse the real and digital using cutting-edge blockchain tech, emphasizing speed and security.

Discover how Ukrainian tech talent is driving global innovation through success stories like GitLab, Revolut, Grammarly, Wise, and Moss.

Discover how Ukrainian tech talent is driving global innovation through success stories like GitLab, Revolut, Grammarly, Wise, and Moss.

After starting two companies, I’ve learned that sales is by far the most important skill for a founder.

After starting two companies, I’ve learned that sales is by far the most important skill for a founder.

Startups usually focus on building their product first, and don’t even try to generate leads or interest until an MVP is ready. Some will just launch on ProductHunt hoping for some lead flow. But in the best case, they will get eyeballs for two days, and then no more leads come in. And building a lead flow is not that easy.

Startups usually focus on building their product first, and don’t even try to generate leads or interest until an MVP is ready. Some will just launch on ProductHunt hoping for some lead flow. But in the best case, they will get eyeballs for two days, and then no more leads come in. And building a lead flow is not that easy.

Robin Thurston, Outside CEO, shares insights: seize opportunities, prioritize customers, embrace mobile tech, build reward mechanisms, impact society.

Robin Thurston, Outside CEO, shares insights: seize opportunities, prioritize customers, embrace mobile tech, build reward mechanisms, impact society.

This is a story about how I won ‘Pioneer’ and what I learned during this program. Pioneer is a fully remote accelerator and it’s a community where entrepreneurs/indie makers help each other improve their own businesses.

This is a story about how I won ‘Pioneer’ and what I learned during this program. Pioneer is a fully remote accelerator and it’s a community where entrepreneurs/indie makers help each other improve their own businesses.

If you are a developer who is still in school or freshly (drop) out of the college or you just have a couple of years of corporate experience and have decided to take on the entrepreneurial journey as a tech-(co)founder / CTO of a startup, this series will help you understand various aspects and the role you will have to play as a technology leader for the success of your startup.

If you are a developer who is still in school or freshly (drop) out of the college or you just have a couple of years of corporate experience and have decided to take on the entrepreneurial journey as a tech-(co)founder / CTO of a startup, this series will help you understand various aspects and the role you will have to play as a technology leader for the success of your startup.

The average consumer’s attention is now worth billions of dollars because that’s how much companies spend on their user acquisition efforts.

The average consumer’s attention is now worth billions of dollars because that’s how much companies spend on their user acquisition efforts.

The debate was deadlocked. Three members of my team at Kanary—the platform I’d built for brands to buy digital ad space—agreed with me, and three didn’t. It was 2013, and I’d spent the last year building Kanary as the company’s founder and CEO.

The debate was deadlocked. Three members of my team at Kanary—the platform I’d built for brands to buy digital ad space—agreed with me, and three didn’t. It was 2013, and I’d spent the last year building Kanary as the company’s founder and CEO.

Mark Gainey talks about the early challenges of creating Strava and how him and his co-founder built a healthy, profitable business.

Mark Gainey talks about the early challenges of creating Strava and how him and his co-founder built a healthy, profitable business.

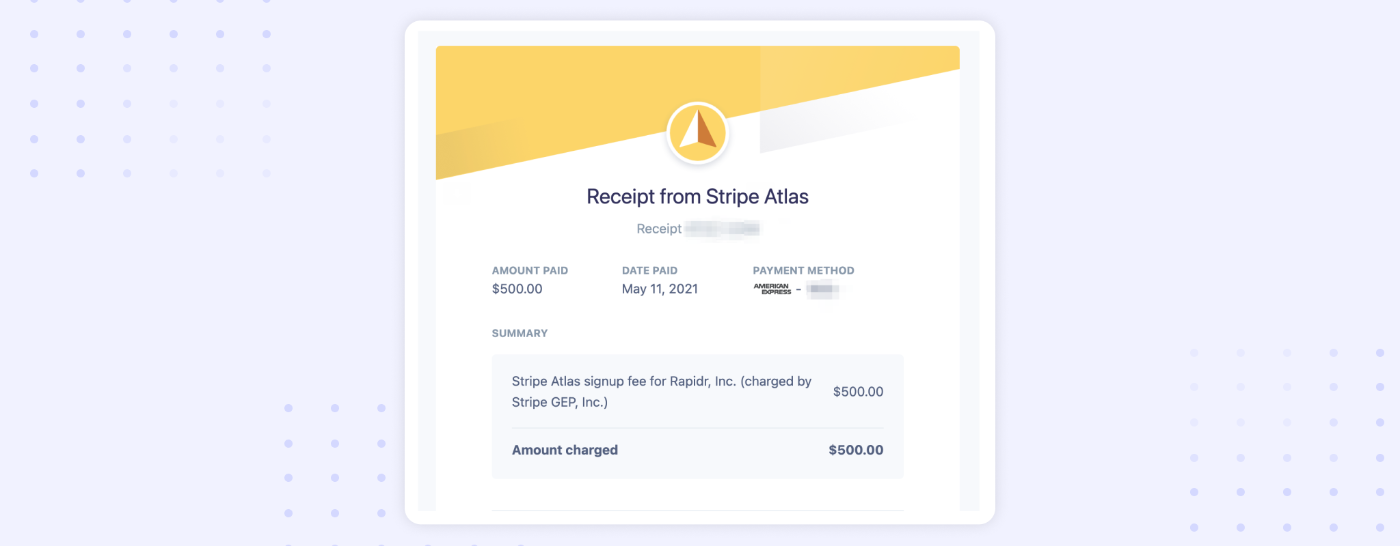

Here’s our end-to-end experience: how we incorporated Rapidr, Inc., a C-Corp with Stripe Atlas, and got set up with a business bank account, mailing address.

Here’s our end-to-end experience: how we incorporated Rapidr, Inc., a C-Corp with Stripe Atlas, and got set up with a business bank account, mailing address.

In this post, you will find nine essential metrics that you should know about and measure. Your KPIs can change as your startup grows.

In this post, you will find nine essential metrics that you should know about and measure. Your KPIs can change as your startup grows.

Didactic's crowdfunding will change the crowdfunding space.

Didactic's crowdfunding will change the crowdfunding space.

This article explores the impressive achievements of these ambitious entrepreneurs and their innovative business ideas.

This article explores the impressive achievements of these ambitious entrepreneurs and their innovative business ideas.

Source: Zuza Gałczyńska, Unsplash

Source: Zuza Gałczyńska, Unsplash

When starting your own business, it may be challenging to choose between an LLC and a Corporation. Here is some information that may make the decision a little less taxing.

Learn fifteen+ types of projects you can turn in your next side hustle or full-time arrangement to leverage your JavaScript skills in a scalable way.

Learn fifteen+ types of projects you can turn in your next side hustle or full-time arrangement to leverage your JavaScript skills in a scalable way.

This long-form article is an informal introduction to Notion for entrepreneurs, founders and startup executives. It covers the basics and explains what makes this company truly special. It’s a 17 minute read full of film and pop culture references because why not. Also, this is my first blog post on the internet.

This long-form article is an informal introduction to Notion for entrepreneurs, founders and startup executives. It covers the basics and explains what makes this company truly special. It’s a 17 minute read full of film and pop culture references because why not. Also, this is my first blog post on the internet.

Photo Credit, Giphy.com/HackerNoon, where we have 1.7M impressions since creating our account in October.

Photo Credit, Giphy.com/HackerNoon, where we have 1.7M impressions since creating our account in October.

We all from time to time come across an idea for a Startup. A company that can be a million or billion or maybe trillion-dollar worth. A company that can be next Tesla or Amazon, but sadly, 99.99999% of us don’t take the next step. That idea remains just a fragment of our memory.

We all from time to time come across an idea for a Startup. A company that can be a million or billion or maybe trillion-dollar worth. A company that can be next Tesla or Amazon, but sadly, 99.99999% of us don’t take the next step. That idea remains just a fragment of our memory.

A serial founder who sold a startup to Apple and worked on infrastructure projects at Google, Harmony.one founder & CEO Stephen Tse has raised an $18M seed round and assembled one of the top engineering teams to build a next-generation high-performance blockchain protocol.

A serial founder who sold a startup to Apple and worked on infrastructure projects at Google, Harmony.one founder & CEO Stephen Tse has raised an $18M seed round and assembled one of the top engineering teams to build a next-generation high-performance blockchain protocol.

Zoom has been in news a lot lately. It has gone from being an enterprise solution to a household name pretty fast.

Zoom has been in news a lot lately. It has gone from being an enterprise solution to a household name pretty fast.

Jessica Livingston's book "Founders at work" (2007, 32 stories) inspired thousands of founders to start their startups.

Jessica Livingston's book "Founders at work" (2007, 32 stories) inspired thousands of founders to start their startups.

My process in building things that can invent opportunities for our business and career

My process in building things that can invent opportunities for our business and career

What a character. This interview began with Zoom breaking and we when we started a new Zoom call, McAfee pretended to talk without making sounds just to fuck with me. Then we hit record:

What a character. This interview began with Zoom breaking and we when we started a new Zoom call, McAfee pretended to talk without making sounds just to fuck with me. Then we hit record:

You’re a non-technical entrepreneur and you have a business-driven vision for your startup. As an entrepreneur, you don’t need to be a technical expert. However, you do need to know the basic concepts because many tech decisions are business decisions.

You’re a non-technical entrepreneur and you have a business-driven vision for your startup. As an entrepreneur, you don’t need to be a technical expert. However, you do need to know the basic concepts because many tech decisions are business decisions.

What's your background, and what are you working on?

What's your background, and what are you working on?

On managing remote teams and creating an atmosphere similar to your office: Recently, I did a webinar with TIE and fellow women founders on Managing remote teams. A lot of you asked for the extensive list of tools that I mentioned in the webinar. So, here it is!

On managing remote teams and creating an atmosphere similar to your office: Recently, I did a webinar with TIE and fellow women founders on Managing remote teams. A lot of you asked for the extensive list of tools that I mentioned in the webinar. So, here it is!

Michael Gaizutis is the Founder of RNO1 – Experience Design Agency for Tech & Web3 Brands of the Future.

Michael Gaizutis is the Founder of RNO1 – Experience Design Agency for Tech & Web3 Brands of the Future.

Burnout is a scary thing. It creeps in when you least expect it. And it usually takes longer than usual for you to realize it’s even happening. Let’s back up a few months.

Burnout is a scary thing. It creeps in when you least expect it. And it usually takes longer than usual for you to realize it’s even happening. Let’s back up a few months.

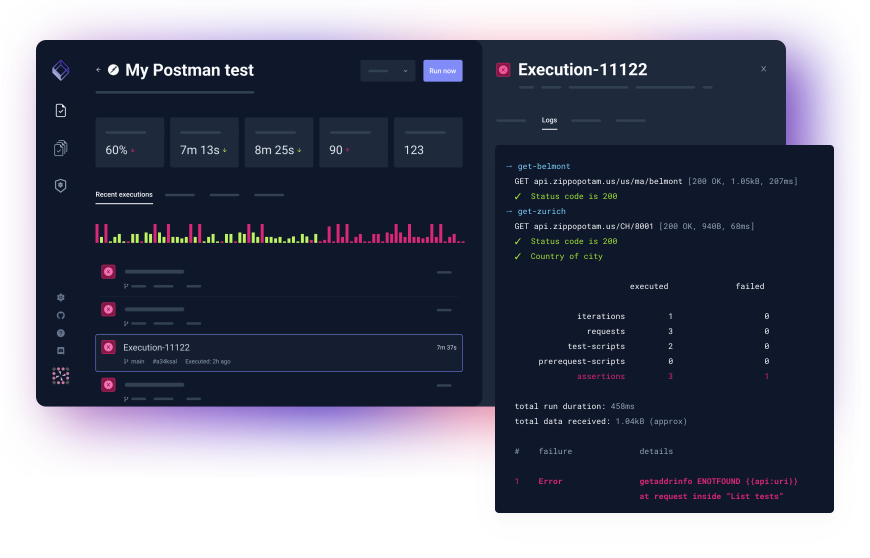

More background information on the Cloud Native Testing Tool, Testkube.

More background information on the Cloud Native Testing Tool, Testkube.

Can you remember when you used to gather in person with your team to define your roadmap and reassess your company’s collective priorities? Every quarter, our team at Pillar VC convenes for a strategic planning session to decide how we’ll invest our time and energy in the months ahead; last week, we held this meeting for the first time over Zoom. While we’ve only been working remotely for a few weeks, it feels like the world around us has changed at lightning speed.

Can you remember when you used to gather in person with your team to define your roadmap and reassess your company’s collective priorities? Every quarter, our team at Pillar VC convenes for a strategic planning session to decide how we’ll invest our time and energy in the months ahead; last week, we held this meeting for the first time over Zoom. While we’ve only been working remotely for a few weeks, it feels like the world around us has changed at lightning speed.

I sent the following note to the Sift team today. I’m also sharing it here in case it’s useful to others.

I sent the following note to the Sift team today. I’m also sharing it here in case it’s useful to others.

It is hard to imagine that one small company can completely transform the way we shop. But that is exactly what Flipkart has done. In 2007, e-commerce was still considered a niche business and most Indians did their shopping offline. Internet was taking over the world and Steve Jobs had just launched the world’s first iPhone in 2007 which was about to disrupt the entire smartphone industry in the years to come.

It is hard to imagine that one small company can completely transform the way we shop. But that is exactly what Flipkart has done. In 2007, e-commerce was still considered a niche business and most Indians did their shopping offline. Internet was taking over the world and Steve Jobs had just launched the world’s first iPhone in 2007 which was about to disrupt the entire smartphone industry in the years to come.

Bill Ottman is the co-creator and CEO of Minds, a free and open source social network with crypto rewards. They continue to make waves as an alternative to the incumbent social network business model of surveillance capitalism. Bill has also been a guest on the Joe Rogan podcast. Today, he kindly took the time to answer some questions for Hacker Noon.

Bill Ottman is the co-creator and CEO of Minds, a free and open source social network with crypto rewards. They continue to make waves as an alternative to the incumbent social network business model of surveillance capitalism. Bill has also been a guest on the Joe Rogan podcast. Today, he kindly took the time to answer some questions for Hacker Noon.

In January 2020, we met with about 45 companies. This enabled us to refine our vision (3 pivots in that month), understand our go-to-market, and start to build a list of potential clients. Once we felt confident about the product, we entered into full implementation mode.

In January 2020, we met with about 45 companies. This enabled us to refine our vision (3 pivots in that month), understand our go-to-market, and start to build a list of potential clients. Once we felt confident about the product, we entered into full implementation mode.

Welcome to the first edition of Product Stories. The first product that I have chosen is Reddit — a company that thousands of startups have tried to emulate but always failed to do so. Let’s look at why that is and what’s so special about Reddit.

Welcome to the first edition of Product Stories. The first product that I have chosen is Reddit — a company that thousands of startups have tried to emulate but always failed to do so. Let’s look at why that is and what’s so special about Reddit.

What's your background?

What's your background?

So, my dear startup founders, do you know what your minions are doing while you aren't looking?

So, my dear startup founders, do you know what your minions are doing while you aren't looking?

A conversation with Joy Pathak, Evinco Winery DAO co-founder, about NFTs and how they are set to change the food and beverages industry.

A conversation with Joy Pathak, Evinco Winery DAO co-founder, about NFTs and how they are set to change the food and beverages industry.

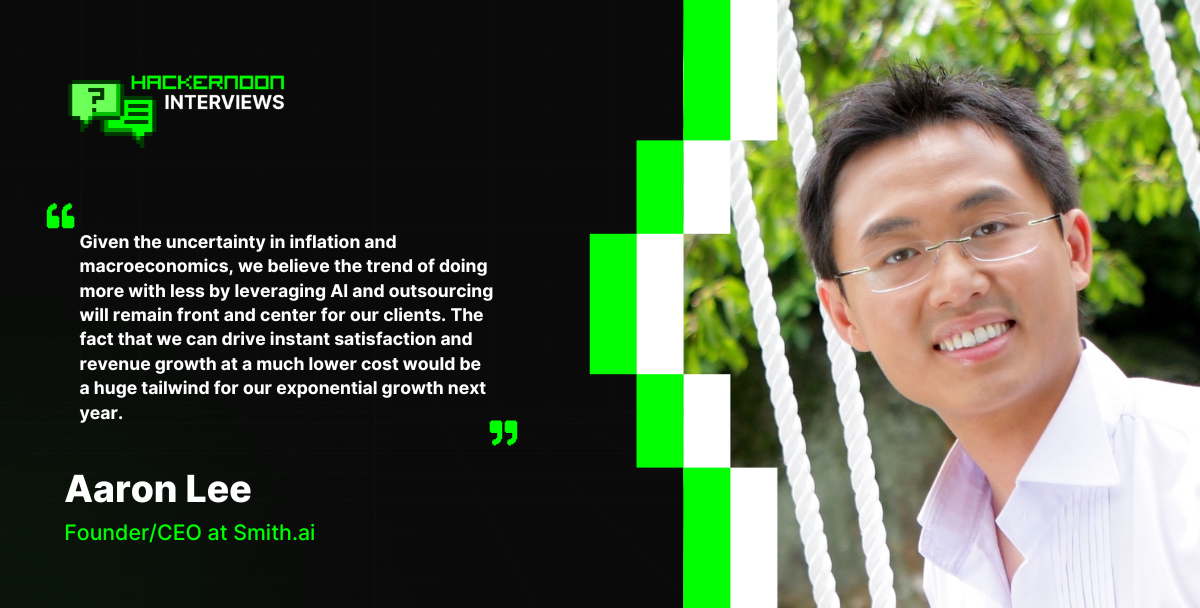

Discover how Smith.ai combines AI and human expertise to revolutionize 24/7 customer engagement for SMBs, driving growth through advanced virtual receptionists.

Discover how Smith.ai combines AI and human expertise to revolutionize 24/7 customer engagement for SMBs, driving growth through advanced virtual receptionists.

What is “The White Tiger?" If you’re asking startup founders, the answer is - not just another Netflix movie, but a unique collection of great business lessons.

What is “The White Tiger?" If you’re asking startup founders, the answer is - not just another Netflix movie, but a unique collection of great business lessons.

The headspace of the owner is key, especially when they're hands-on in running their business, putting their all into it

The headspace of the owner is key, especially when they're hands-on in running their business, putting their all into it

Colette Wyatt is a Chief Technology Officer at Evolve, an award-winning UK-based software house with an R&D Centre in Ukraine. She's also a Co-Founder and COO of e-bate, a revolutionary platform for rebates management, which attracted £950,000 last year from Mercia Asset Management, the MEIF Proof of Concept & Early Stage Fund, and part of the Midlands Engine Investment Fund.

Colette Wyatt is a Chief Technology Officer at Evolve, an award-winning UK-based software house with an R&D Centre in Ukraine. She's also a Co-Founder and COO of e-bate, a revolutionary platform for rebates management, which attracted £950,000 last year from Mercia Asset Management, the MEIF Proof of Concept & Early Stage Fund, and part of the Midlands Engine Investment Fund.

Lingke Wang and the Ethos team have recently raised over $46 million in order to simplify and modernize the archaic life insurance industry.

Lingke Wang and the Ethos team have recently raised over $46 million in order to simplify and modernize the archaic life insurance industry.

Peter Kolmisoppi explains why The Pirate Bay is still alive and some websites aren't.

Peter Kolmisoppi explains why The Pirate Bay is still alive and some websites aren't.

The six Archetypes of Founder Madness: Imperial Individualist, Naively Confident, Strategic Contrarian, Frontier Explorer, Mad Scientist, and Global Catalyst.

The six Archetypes of Founder Madness: Imperial Individualist, Naively Confident, Strategic Contrarian, Frontier Explorer, Mad Scientist, and Global Catalyst.

Luke Sophinos tells the story of Mark Leonard.

Luke Sophinos tells the story of Mark Leonard.

Raise money without giving up a piece of your company

Raise money without giving up a piece of your company

Ten years after founding The Information, the tech journalist–CEO contemplates everything she wishes she’d known from the start.

Ten years after founding The Information, the tech journalist–CEO contemplates everything she wishes she’d known from the start.

I was 24 years old. A baby.

I was 24 years old. A baby.

Please welcome our weekly sponsor Paperform to Hacker Noon! I stumbled upon Paperform when their founder Dean McPherson contributed a number of in the trenches startup founder stories, like Stop Thinking About Scaling — For Developers Working on Crazy New Startup Ideas, to Hacker Noon. Today, we’re going to catch up on the state of this startup — and find out what makes Dean & his cofounder Dionysia McPherson do what they do.

Please welcome our weekly sponsor Paperform to Hacker Noon! I stumbled upon Paperform when their founder Dean McPherson contributed a number of in the trenches startup founder stories, like Stop Thinking About Scaling — For Developers Working on Crazy New Startup Ideas, to Hacker Noon. Today, we’re going to catch up on the state of this startup — and find out what makes Dean & his cofounder Dionysia McPherson do what they do.

Community commerce is transforming growth by turning customers into advocates. Learn how brands drive trust, retention, and revenue through community.

Community commerce is transforming growth by turning customers into advocates. Learn how brands drive trust, retention, and revenue through community.

What if startup founders learning mixed martial arts - or mixed martial arts fighters found a startup. Takeaways of traversed startup journey and sports.

What if startup founders learning mixed martial arts - or mixed martial arts fighters found a startup. Takeaways of traversed startup journey and sports.

Most organizations consider customer service an overhead while it is an opportunity. It allows you to drive continued value from the customer even after a sale.

Most organizations consider customer service an overhead while it is an opportunity. It allows you to drive continued value from the customer even after a sale.

Licenseware is the first open app ecosystem for software license management. Reduce software costs and manage licensing risks, PAYIG, completely modular.

Licenseware is the first open app ecosystem for software license management. Reduce software costs and manage licensing risks, PAYIG, completely modular.

First time founders build out of passion. They face a problem and try to solve for themselves, making assumptions that everyone has the same problem.

First time founders build out of passion. They face a problem and try to solve for themselves, making assumptions that everyone has the same problem.

Read for opinions on growing a robust community in any niche, adapting your product to the metaverse, the power of outsourcing and the future of AI.

Read for opinions on growing a robust community in any niche, adapting your product to the metaverse, the power of outsourcing and the future of AI.

No-Code Report is a weekly no-code newsletter, built using no-code tools like Webflow, Airtable, and Zapier. Working at a no-code analytics firm, I wanted to learn about insights in the field more broadly, so I spoke with No-Code Report's founder, Parker Thompson, on the state of the industry and its future.

No-Code Report is a weekly no-code newsletter, built using no-code tools like Webflow, Airtable, and Zapier. Working at a no-code analytics firm, I wanted to learn about insights in the field more broadly, so I spoke with No-Code Report's founder, Parker Thompson, on the state of the industry and its future.

Growth hacking once drove startup traction, but customer trust now powers sustainable growth. Learn how trust, retention, and community drive startup success.

Growth hacking once drove startup traction, but customer trust now powers sustainable growth. Learn how trust, retention, and community drive startup success.

I am 36 years old and have long felt disconnected from the world. Not so much the natural world — that I’ve been lovingly drawn to and constantly in awe of as far back as I can remember.

I am 36 years old and have long felt disconnected from the world. Not so much the natural world — that I’ve been lovingly drawn to and constantly in awe of as far back as I can remember.

Seth Flora is the owner of LEO Digital Marketing. In his spare time, he helps founders create business plans, form strategies, and more.

Seth Flora is the owner of LEO Digital Marketing. In his spare time, he helps founders create business plans, form strategies, and more.

Over the past 7 years I have worked in large IT companies in the Russian Federation, EU, and in the USA. Here's what I wish I knew before I started each project

Over the past 7 years I have worked in large IT companies in the Russian Federation, EU, and in the USA. Here's what I wish I knew before I started each project

Roughly a decade ago I decided to move away from my corporate job in investment banking in London to pursue something I always knew I wanted: to become an entrepreneur.

Roughly a decade ago I decided to move away from my corporate job in investment banking in London to pursue something I always knew I wanted: to become an entrepreneur.

Four fundraising tips from Rousseau Kazi of Threads.com

Four fundraising tips from Rousseau Kazi of Threads.com

For parents of toddlers and babies, finding the right daycare can be a huge challenge. Jessica Chang saw this as an opportunity.

For parents of toddlers and babies, finding the right daycare can be a huge challenge. Jessica Chang saw this as an opportunity.

This map is a visual overview of every company that helps you get an investment for your startup, from pitch decks to captable management.

This map is a visual overview of every company that helps you get an investment for your startup, from pitch decks to captable management.

myPluto helps small teams, young entrepreneurs and ,aspiring product managers to navigate the development of their first product in a structured manner.

myPluto helps small teams, young entrepreneurs and ,aspiring product managers to navigate the development of their first product in a structured manner.

Here is how a role most people had never heard of became the career opportunity everyone's talking about.

Here is how a role most people had never heard of became the career opportunity everyone's talking about.

One of the most common frustrations among business professionals is performance metrics. Performance metrics are how employers value the contributions made by their employees and how employees clarify the expectations of their employer. It’s a simple tool that when used with intentionality can be a powerful asset for a company, but when used wrong can be one of the fastest ways to lose top talent and discourage your workforce.

One of the most common frustrations among business professionals is performance metrics. Performance metrics are how employers value the contributions made by their employees and how employees clarify the expectations of their employer. It’s a simple tool that when used with intentionality can be a powerful asset for a company, but when used wrong can be one of the fastest ways to lose top talent and discourage your workforce.

Founders and CEOs have a lot of tasks and responsibilities. Coaching the team, becoming a mentor for newcomers, and preparing for the end of the world.

Founders and CEOs have a lot of tasks and responsibilities. Coaching the team, becoming a mentor for newcomers, and preparing for the end of the world.

Choosing lean, scalable, and adaptable tools is the smart play.

Choosing lean, scalable, and adaptable tools is the smart play.

More than half of America’s cutting-edge companies valued at $1 billion or more were established by foreign-born founders.

More than half of America’s cutting-edge companies valued at $1 billion or more were established by foreign-born founders.

Tips and resources for applying to Y Combinator

Tips and resources for applying to Y Combinator

In this interview, we spoke to the company’s Co-CEO and Co-Founder, Ashwin Rathod about its innovation.

In this interview, we spoke to the company’s Co-CEO and Co-Founder, Ashwin Rathod about its innovation.

Airbyte, the open-source data integration platform, shares how they performed on their OKRs for Q1 2021, and what their new OKRs for Q2 2021 are.

Airbyte, the open-source data integration platform, shares how they performed on their OKRs for Q1 2021, and what their new OKRs for Q2 2021 are.

Juan Gonzalez (@Kaelon @JuanDotCo) describes how WordPress, like every founder-led enterprise, is approaching a predictably dangerous period.

Juan Gonzalez (@Kaelon @JuanDotCo) describes how WordPress, like every founder-led enterprise, is approaching a predictably dangerous period.

It’s been roughly two months now since the Coronavirus turned our lives upside down. From practising social distancing and getting used to a life confined within four walls. To constant washing of hands and wearing masks and other Personal Protective Equipment (PPE) just to buy a loaf of bread. All the while watching strangers, friends and loved ones getting sick, COVID-19 is truly something none of us saw coming — well besides Bill Gates.

It’s been roughly two months now since the Coronavirus turned our lives upside down. From practising social distancing and getting used to a life confined within four walls. To constant washing of hands and wearing masks and other Personal Protective Equipment (PPE) just to buy a loaf of bread. All the while watching strangers, friends and loved ones getting sick, COVID-19 is truly something none of us saw coming — well besides Bill Gates.

Anyone familiar with our project, Digitex Futures, will know that it’s been a long and eventful journey to get here. But we’ve stayed the course. Even during the worst bear market imaginable when many other projects had to throw in the towel, we’ve managed to survive.

Anyone familiar with our project, Digitex Futures, will know that it’s been a long and eventful journey to get here. But we’ve stayed the course. Even during the worst bear market imaginable when many other projects had to throw in the towel, we’ve managed to survive.

Startup interview with Antoni Zolciak of Aleph Zero, a public blockchain with enhanced privacy features. We combine academic excellence with business know-how.

Startup interview with Antoni Zolciak of Aleph Zero, a public blockchain with enhanced privacy features. We combine academic excellence with business know-how.

Pilot's annual founder survey report found that a quarter of founders are self-funding.

Pilot's annual founder survey report found that a quarter of founders are self-funding.

March 13, 2020. I’ll remember this day as Charcoal Grey Friday in honor of my Costco sweatpants (thanks mother-in-law) and it being the hardest day of my career at GrowthHit.

March 13, 2020. I’ll remember this day as Charcoal Grey Friday in honor of my Costco sweatpants (thanks mother-in-law) and it being the hardest day of my career at GrowthHit.

Genesis Mining CEO Marco Streng studied mathematics at the Ludwig-Maximilian University of Munich before

co-founding Genesis Mining in 2013 and becoming a passionate advocate for blockchain

technology and cryptocurrency.

Genesis Mining CEO Marco Streng studied mathematics at the Ludwig-Maximilian University of Munich before

co-founding Genesis Mining in 2013 and becoming a passionate advocate for blockchain

technology and cryptocurrency.

If you want to start your business but don't know where to get capital, you need to find out who the investors are and why they are ready to sponsor startups.

If you want to start your business but don't know where to get capital, you need to find out who the investors are and why they are ready to sponsor startups.

From raising money outside of Silicon Valley to pivoting after hitting a fundraising wall, to dealing with tornados and pandemics - Jammber founder Marcus Cobb shares his top tips for startup founders.

From raising money outside of Silicon Valley to pivoting after hitting a fundraising wall, to dealing with tornados and pandemics - Jammber founder Marcus Cobb shares his top tips for startup founders.

Apple Entrepreneur Camp taught key lessons—app inclusivity, user-centered approach, product page optimization, app review preparation, and user rewards.

Apple Entrepreneur Camp taught key lessons—app inclusivity, user-centered approach, product page optimization, app review preparation, and user rewards.

“No” is often equated with being mean but “no” isn’t about shutting projects and people down. Here's how to say no in a corporate setting without sounding rude.

“No” is often equated with being mean but “no” isn’t about shutting projects and people down. Here's how to say no in a corporate setting without sounding rude.

If you’re getting your startup up and running, then you know that it takes a lot of effort and time. It also takes a lot of resources. No matter the size of the business, you are investing resources in it, and we’re not just talking about financial resources. Startup owners are also prepared to invest their time, energy, and emotions in something they truly believe in.

If you’re getting your startup up and running, then you know that it takes a lot of effort and time. It also takes a lot of resources. No matter the size of the business, you are investing resources in it, and we’re not just talking about financial resources. Startup owners are also prepared to invest their time, energy, and emotions in something they truly believe in.

Startup interview with Viktor Kochetov, CEO of Kyrrex.

Startup interview with Viktor Kochetov, CEO of Kyrrex.

People have a wide range of different "tools" that can give them cheap and fast relief of anxiety or other psychological conditions.

People have a wide range of different "tools" that can give them cheap and fast relief of anxiety or other psychological conditions.

A first-time CEO shares what went right, what went wrong, and the governance mistakes every startup founder should avoid before it’s too late.

A first-time CEO shares what went right, what went wrong, and the governance mistakes every startup founder should avoid before it’s too late.

Andrew Masanto is a two-time web3 unicorn founder, having started and popularized two of the top 100 cryptocurrencies (Hedera and Reserve).

Andrew Masanto is a two-time web3 unicorn founder, having started and popularized two of the top 100 cryptocurrencies (Hedera and Reserve).

In this interview, we speak with Malik Drabla, the co-founder of Adrenaline - an AI project to help coders make the best of their code.

In this interview, we speak with Malik Drabla, the co-founder of Adrenaline - an AI project to help coders make the best of their code.

Hacker Noon Non-Technical Founder Podcast- Episode 53 Zack Hurley

Hacker Noon Non-Technical Founder Podcast- Episode 53 Zack Hurley

If you’re a crypto startup dealing with stubborn institutions, you’re not alone!

If you’re a crypto startup dealing with stubborn institutions, you’re not alone!

I have been speaking to Coworking spaces, Incubators and Accelerators across London and it has become apparent that there is a common problem arising from non-technical startup founders. This transcends the culture, this impacts more than just female or minority-led startups.

I have been speaking to Coworking spaces, Incubators and Accelerators across London and it has become apparent that there is a common problem arising from non-technical startup founders. This transcends the culture, this impacts more than just female or minority-led startups.

A few years ago, Matthew Klein and his brother Andrew saw that the retail landscape was changing and that companies needed more agility than ever.

A few years ago, Matthew Klein and his brother Andrew saw that the retail landscape was changing and that companies needed more agility than ever.

My "Tough Love" Talk To Founders Who Are Struggling To Raise Capital

My "Tough Love" Talk To Founders Who Are Struggling To Raise Capital

Bringing Dishonest Crypto Journalists Lies to Light - The Story of Danny De Hek and Sultan KassamBringing Dishonest Crypto Journalists Lies to Light - The Story

Bringing Dishonest Crypto Journalists Lies to Light - The Story of Danny De Hek and Sultan KassamBringing Dishonest Crypto Journalists Lies to Light - The Story

Eowyn emphasizes security in the crypto realm amidst rising cybersecurity threats.

Eowyn emphasizes security in the crypto realm amidst rising cybersecurity threats.

Marc Randolph goes over the importance of building a great team.

Marc Randolph goes over the importance of building a great team.

The cryptomarket is melting. The cryptomarket meltdown is a result of the bearish sentiment in the market.

The cryptomarket is melting. The cryptomarket meltdown is a result of the bearish sentiment in the market.

"What I see is how the pandemic is exposing the inefficiency and inequality of the existing fiat system. Governments are printing money to bailout those who recklessly spent it during the good years. Banks lending government-backed money to those who don't need it instead of helping businesses in distress." - Lior Yaffe, Co-Founder, Jelrurida

"What I see is how the pandemic is exposing the inefficiency and inequality of the existing fiat system. Governments are printing money to bailout those who recklessly spent it during the good years. Banks lending government-backed money to those who don't need it instead of helping businesses in distress." - Lior Yaffe, Co-Founder, Jelrurida

Childhood friends James and Allen are making it easier for companies to build machine learning teams with AdaptiLab (Techstars Seattle ‘19).

Childhood friends James and Allen are making it easier for companies to build machine learning teams with AdaptiLab (Techstars Seattle ‘19).

You’re going to spend more time with your co-founder than with your spouse. This is why finding the right one is the one activity you CANNOT afford to rush. If you’re truly passionate about founding a company, you have only two options: compromise or keep on looking.

You’re going to spend more time with your co-founder than with your spouse. This is why finding the right one is the one activity you CANNOT afford to rush. If you’re truly passionate about founding a company, you have only two options: compromise or keep on looking.

Serial entrepreneur Andrew Hoag had a huge frustration.

Serial entrepreneur Andrew Hoag had a huge frustration.

There are a number of prominent startup examples that have been very successful in the past few decades like Facebook, Instagram, and Airbnb among others. But from these stories of success, quite a number of failure stories are left untouched. According to an estimate 9 out of 10 startups end up failing. Entrepreneurs publish post mortem online and they are quite haunting. The reasons for failure may depend upon various factors like insufficient funding, incompetent team, and lack of motivation. I have compiled a list of 10 reasons which have been the cause of startup failures.

There are a number of prominent startup examples that have been very successful in the past few decades like Facebook, Instagram, and Airbnb among others. But from these stories of success, quite a number of failure stories are left untouched. According to an estimate 9 out of 10 startups end up failing. Entrepreneurs publish post mortem online and they are quite haunting. The reasons for failure may depend upon various factors like insufficient funding, incompetent team, and lack of motivation. I have compiled a list of 10 reasons which have been the cause of startup failures.

How building in public helped the growth of my startup.

How building in public helped the growth of my startup.

What's your background, and what are you working on?

What's your background, and what are you working on?

For most companies, growth marketing is the way of the future for leveraging data and agility to scale revenue and increase customer lifetime value.

For most companies, growth marketing is the way of the future for leveraging data and agility to scale revenue and increase customer lifetime value.

Matt is the co-founder & VP of Marketing and Developer Relations at Manifold, the cloud-native marketplace company.

Matt is the co-founder & VP of Marketing and Developer Relations at Manifold, the cloud-native marketplace company.

Why I left Google to found an AI startup funded by Techstars and Peter Thiel.

Why I left Google to found an AI startup funded by Techstars and Peter Thiel.

Despite the bear market startups should not turn off their projects in the crypto industry and Web 3.0. A few tips for projects on how to start in a bear market

Despite the bear market startups should not turn off their projects in the crypto industry and Web 3.0. A few tips for projects on how to start in a bear market

The concepts behind Erlang/OTP/Elixir make it a great fit for a tool like the one I was building

The concepts behind Erlang/OTP/Elixir make it a great fit for a tool like the one I was building

I think the ICO run is past us. We will not see a crazy market like we did in 2017. Scammers are very sophisticated and are always coming up with new ways to scam.

I think the ICO run is past us. We will not see a crazy market like we did in 2017. Scammers are very sophisticated and are always coming up with new ways to scam.

True to my conviction that blockchain's enormous disruptive potential can change the status quo, I recently sat down with Bolaji to explore AgriFi and Tórónet

True to my conviction that blockchain's enormous disruptive potential can change the status quo, I recently sat down with Bolaji to explore AgriFi and Tórónet

The world of AI startups is rapidly expanding, with a multitude of new players and innovative solutions in various industries.

The world of AI startups is rapidly expanding, with a multitude of new players and innovative solutions in various industries.

A conversation with Jet Liu on how a combination of AI, Web3, and innovations in computation technology can help shape the future.

A conversation with Jet Liu on how a combination of AI, Web3, and innovations in computation technology can help shape the future.

Choosing the right set of frameworks, database, front-end tools, back-end tools to build a long lasting tech stack for your SaaS

Choosing the right set of frameworks, database, front-end tools, back-end tools to build a long lasting tech stack for your SaaS

On the Importance of Building Healthy Co-Founder Relationships, Navigating Investor Meetings, and Investing in Your Mental Health as a Founder.

On the Importance of Building Healthy Co-Founder Relationships, Navigating Investor Meetings, and Investing in Your Mental Health as a Founder.

Daniel Quoc Dung Huynh, CEO and Co-founder of Mithril Security, is launching a startup to democratize privacy-by-design AI tools.

Daniel Quoc Dung Huynh, CEO and Co-founder of Mithril Security, is launching a startup to democratize privacy-by-design AI tools.

10 Lessons I learned after making $1K as an Indie Hacker

10 Lessons I learned after making $1K as an Indie Hacker

We all have different roles to fulfill during a product’s journey. Some of us are heavily invested on the sales and marketing side while others consider the technical decisions as their day to day job. While segregation of work is important as well as useful for founders, there are a lot of things that all founders need to learn to make sure they are ahead on the curve as they take continuous decisions for the product and its growth. Here are 10 things to do right away as you start your product journey.

We all have different roles to fulfill during a product’s journey. Some of us are heavily invested on the sales and marketing side while others consider the technical decisions as their day to day job. While segregation of work is important as well as useful for founders, there are a lot of things that all founders need to learn to make sure they are ahead on the curve as they take continuous decisions for the product and its growth. Here are 10 things to do right away as you start your product journey.

When it comes to selecting the right back-end technology. It can be confusing to evaluate your project needs and a versatile fit for your back-end development. However, NodeJS can be the best fit for your product. Thus, hire NodeJS developers to build the best business solution. Some of the crucial factors include whether you should look for offshore or onshore hiring.

When it comes to selecting the right back-end technology. It can be confusing to evaluate your project needs and a versatile fit for your back-end development. However, NodeJS can be the best fit for your product. Thus, hire NodeJS developers to build the best business solution. Some of the crucial factors include whether you should look for offshore or onshore hiring.

You have built a tech startup to provide an outstanding solution, but it is not necessary that all the people will understand your idea in the beginning.

You have built a tech startup to provide an outstanding solution, but it is not necessary that all the people will understand your idea in the beginning.

Yes, we’re witnessing a crisis unfolding. Not only people get gripped by the coronavirus fear. It’s like a stroke for most businesses — some will recover, some won’t.

Yes, we’re witnessing a crisis unfolding. Not only people get gripped by the coronavirus fear. It’s like a stroke for most businesses — some will recover, some won’t.

With a new political wind blowing through Brazil, we need to ask: What impact might Lula's election have on the buzzing startup ecosystem?

With a new political wind blowing through Brazil, we need to ask: What impact might Lula's election have on the buzzing startup ecosystem?

It is important to realize that we have the ability to manufacture our own fate when we want to. - Eric Haney, Delta Force operator

It is important to realize that we have the ability to manufacture our own fate when we want to. - Eric Haney, Delta Force operator

I’ve been a full-time founder for almost a year but have been into startup culture for most of my professional career as a software engineer (~4 years).

I’ve been a full-time founder for almost a year but have been into startup culture for most of my professional career as a software engineer (~4 years).

Unsuccessful startups are all alike; every successful startup has succeeded in its own way.

Unsuccessful startups are all alike; every successful startup has succeeded in its own way.

Software Development is a route that’s proved to be very popular in the last couple of years in tech. From HTML & CSS webinars to Ruby on Rails meet ups, you can’t escape the hype. But what if coding isn’t for you? What if you want to solve problems in Tech without writing code, is there a career out there for you?

Software Development is a route that’s proved to be very popular in the last couple of years in tech. From HTML & CSS webinars to Ruby on Rails meet ups, you can’t escape the hype. But what if coding isn’t for you? What if you want to solve problems in Tech without writing code, is there a career out there for you?

Anti Danilevski, KickEX CEO and founder, talks about Top 5 Methods of Running an Effective Cryptocurrency Exchange based on his own experiences in the field.

Anti Danilevski, KickEX CEO and founder, talks about Top 5 Methods of Running an Effective Cryptocurrency Exchange based on his own experiences in the field.

What's your background, and what are you working on?

What's your background, and what are you working on?

Geoffrey Frank is the founder of Myntist, a startup that combines e-commerce and d-commerce platforms into a digital hybrid ecosystem.

Geoffrey Frank is the founder of Myntist, a startup that combines e-commerce and d-commerce platforms into a digital hybrid ecosystem.

In July, my brother and I launched our first software product after nearly 2 years of working full-time on our business. We hit a big milestone that month and generated our first $10 in software revenue.

In July, my brother and I launched our first software product after nearly 2 years of working full-time on our business. We hit a big milestone that month and generated our first $10 in software revenue.

Lose the to-do list, there is only one thing you need to focus on

Lose the to-do list, there is only one thing you need to focus on

A new breed of tech visionaries has been instrumental in driving this change and helping to deliver Web 3.0 solutions to the masses.

A new breed of tech visionaries has been instrumental in driving this change and helping to deliver Web 3.0 solutions to the masses.

Explore Sound.me's journey, an AI-driven influencer platform transforming influencer marketing with simplicity, accountability, and global reach.

I’ve always found naming things to be particularly challenging. That is because a bad name is way worse than a good name is good - naming your car the “No-Go” (as the Chevy Nova was in Spanish) is far worse than a decent name like the Passat is good. Naming is, unfortunately, a negative sum game.

I’ve always found naming things to be particularly challenging. That is because a bad name is way worse than a good name is good - naming your car the “No-Go” (as the Chevy Nova was in Spanish) is far worse than a decent name like the Passat is good. Naming is, unfortunately, a negative sum game.

David Sutter is the CEO of OpenTrade, an institutional lending platform that provides users access to a suite of on-chain credit products for tokenized real-wor

David Sutter is the CEO of OpenTrade, an institutional lending platform that provides users access to a suite of on-chain credit products for tokenized real-wor

I know what you’re thinking. “That title has to be a typo. No one could grow that fast!”. I’m here to tell you that if you work hard and pursue your dreams you too can make $10 in 2 years.

I know what you’re thinking. “That title has to be a typo. No one could grow that fast!”. I’m here to tell you that if you work hard and pursue your dreams you too can make $10 in 2 years.

I’m Alex and I’m the Founder at Adadot.

I’m Alex and I’m the Founder at Adadot.

I am speaking with James Wo, the CEO and founder of the investment firm Digital Finance Group, to discuss promising sectors within Web 3.0 for investment.

I am speaking with James Wo, the CEO and founder of the investment firm Digital Finance Group, to discuss promising sectors within Web 3.0 for investment.

Philcoin is the world’s first philanthropic blockchain super dApp, says founder Jerry Lopez.

Philcoin is the world’s first philanthropic blockchain super dApp, says founder Jerry Lopez.

That are countless blog posts that extoll the benefits and power of digital marketing. There are even more that show you exactly how to do it.

That are countless blog posts that extoll the benefits and power of digital marketing. There are even more that show you exactly how to do it.

To start with, this is a tricky topic, where I might find people in conflict with my perception but after all when isn’t conflict a promising act. Conflict by its meaning is a disagreement where one holds an entirely opposite perspective and surely does one defend it as if it was their very own life at stake. I think that is a beauty of it, perhaps lasting for a long time that is unexpected or usual. I would put it as my experience to suggest that I have seen people get excited and enthusiastic about doing something. It can be an idea or a project or anything that they either want to achieve in life or a common goal to which one puts an effort.

To start with, this is a tricky topic, where I might find people in conflict with my perception but after all when isn’t conflict a promising act. Conflict by its meaning is a disagreement where one holds an entirely opposite perspective and surely does one defend it as if it was their very own life at stake. I think that is a beauty of it, perhaps lasting for a long time that is unexpected or usual. I would put it as my experience to suggest that I have seen people get excited and enthusiastic about doing something. It can be an idea or a project or anything that they either want to achieve in life or a common goal to which one puts an effort.

Learn from our twist-filled journey and gain valuable insights. Find inspiration and guidance for your own pivotal path

Learn from our twist-filled journey and gain valuable insights. Find inspiration and guidance for your own pivotal path

A short story of a workaholic engineer switching from a developer to a product founder in 10 years.

A short story of a workaholic engineer switching from a developer to a product founder in 10 years.

Let's make the business world beautiful with brand designs.

Let's make the business world beautiful with brand designs.

Explore Patrick Brown's vision for Unity Communications, blending superior BPO services with his love for DJing.

Explore Patrick Brown's vision for Unity Communications, blending superior BPO services with his love for DJing.

Remote work is booming largely because of the lockdown. But this way of working has been around for a long time - especially among knowledge workers. During the pandemic, a lot of companies tested remote working for the first time, and most of them do not plan to go back to the office even after the lockdown. However, some holes need to be patched and things taken care of before any founder jumps into remote working permanently.

Remote work is booming largely because of the lockdown. But this way of working has been around for a long time - especially among knowledge workers. During the pandemic, a lot of companies tested remote working for the first time, and most of them do not plan to go back to the office even after the lockdown. However, some holes need to be patched and things taken care of before any founder jumps into remote working permanently.

Lessons from a founder on shaping startup culture that scales — from hiring and leadership to trust, transparency, and building a team you’re proud of.

Lessons from a founder on shaping startup culture that scales — from hiring and leadership to trust, transparency, and building a team you’re proud of.

In the beginning of June 2020, we had enough cash to sustain ourselves for 2 years, and had decided to pivot. At the time, we weren’t sure if we needed to move away from our product, on which revenues were growing very slowly, or not. We spent 6 weeks in full exploration mode to identify what our next step was.

In the beginning of June 2020, we had enough cash to sustain ourselves for 2 years, and had decided to pivot. At the time, we weren’t sure if we needed to move away from our product, on which revenues were growing very slowly, or not. We spent 6 weeks in full exploration mode to identify what our next step was.

Are you a startup founder? Consider filling out these writing prompts so readers can get to know your company better, and it's a great way for others to learn.

Are you a startup founder? Consider filling out these writing prompts so readers can get to know your company better, and it's a great way for others to learn.

Never underestimate the power of sharing what you think. Write, publish, post. Technology is built that way — brick by brick, idea by idea.

Never underestimate the power of sharing what you think. Write, publish, post. Technology is built that way — brick by brick, idea by idea.

In this interview, you are going to learn more about Carlos's blockchain career and DEGA, his brainchild.

In this interview, you are going to learn more about Carlos's blockchain career and DEGA, his brainchild.

Timeless advice to profit from your passions, capitalize on your ideas and become a better human being.

Timeless advice to profit from your passions, capitalize on your ideas and become a better human being.

5 reasons why you should do competitive analysis before building a product ?

Using competitive analysis, startup founders can get a head on in product.

5 reasons why you should do competitive analysis before building a product ?

Using competitive analysis, startup founders can get a head on in product.

One thing that has become clear in the last few years is that the soft parts of data science are becoming even more important. What do I mean by soft parts? I a

One thing that has become clear in the last few years is that the soft parts of data science are becoming even more important. What do I mean by soft parts? I a

Achieving a €260,000 with My Central European Software Engineering Leadership Venture.

Achieving a €260,000 with My Central European Software Engineering Leadership Venture.

Nicole Nguyen is the co-founder of Duelist King, the first NFT game powered by Dual Launch via OccamRazer IDO and PancakeSwap IFO.

Nicole Nguyen is the co-founder of Duelist King, the first NFT game powered by Dual Launch via OccamRazer IDO and PancakeSwap IFO.

Forter is the leading provider in e-commerce fraud prevention, protecting $130B in digital transactions annually.

Forter is the leading provider in e-commerce fraud prevention, protecting $130B in digital transactions annually.

Miki Agrawal shares her most thoughtful and inspirational quotes about life, entrepreneurship, technology, and not letting the haters win.

Miki Agrawal shares her most thoughtful and inspirational quotes about life, entrepreneurship, technology, and not letting the haters win.

Venket Naga, CEO of Serenity Shield, talks about his journey in tech, the inspiration behind the blockchain initiative and how it aims to redefine data security

Venket Naga, CEO of Serenity Shield, talks about his journey in tech, the inspiration behind the blockchain initiative and how it aims to redefine data security

Adam Knuckey, co-founder of Dolomite, shares the story of its inception, the challenges faced, and the vision for the future.

Adam Knuckey, co-founder of Dolomite, shares the story of its inception, the challenges faced, and the vision for the future.

Every decision and step we take at a startup is based on some belief. Here's how to validate those beliefs and build products like a scientist ;)

Every decision and step we take at a startup is based on some belief. Here's how to validate those beliefs and build products like a scientist ;)

Estimated Reading Time: 14 minutes

Estimated Reading Time: 14 minutes

On this episode. Jon Dahl, CEO of Mux, and Thierry Schellenbach, CEO of Stream, talk to Amy Tom about starting their API-powered platform.