2026-08-11 01:09:58

For the research and modeling behind this analysis, see our 2026 State of the AI Economy Report.

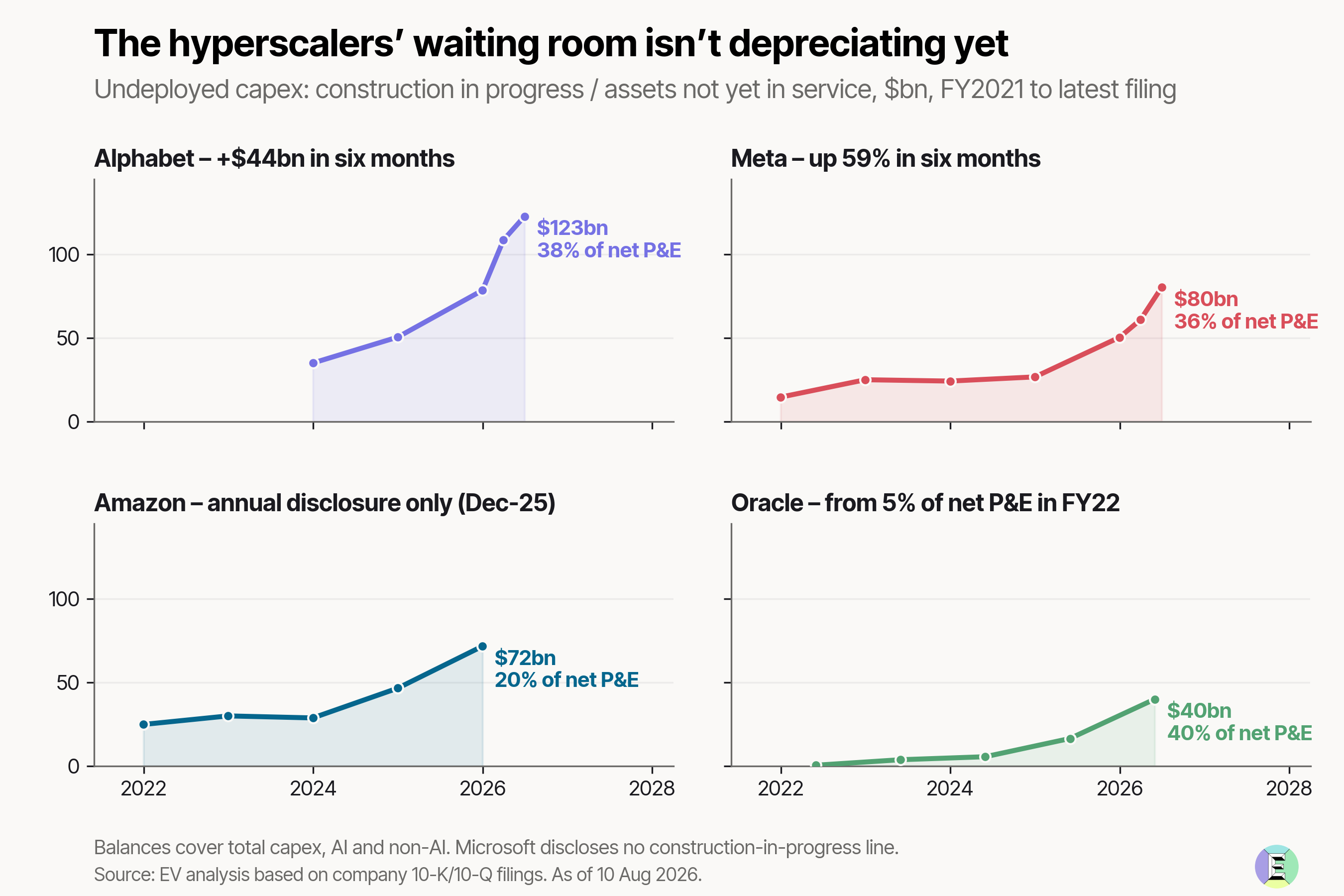

Based on current guidance, the seven largest AI-infrastructure builders1 expect capital expenditure of $863 billion in 2026 – 88% more than last year. We estimate that roughly two-thirds, some $550 billion, will be AI-related.

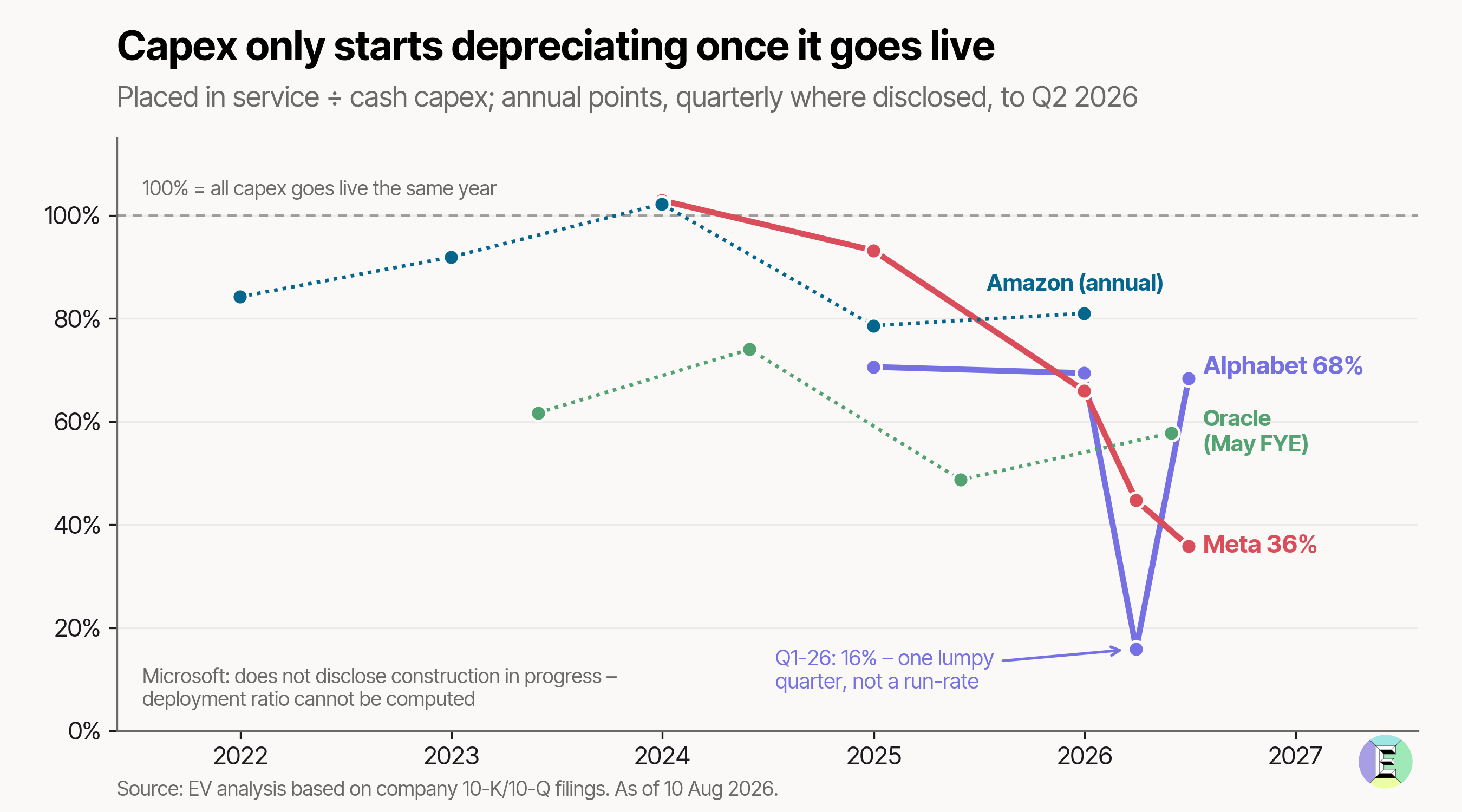

That investment does not begin affecting earnings through depreciation as soon as a project starts. While infrastructure is being built or assembled, the attributable costs are capitalized on the balance sheet as construction in progress. Depreciation begins only when the assets are ready for their intended use.

Across the four hyperscalers that disclose this balance2, assets not yet in service now total $315 billion3, up from $281 billion one quarter earlier. This represents both capacity still to come online and a reservoir of future depreciation that has not yet reached the income statement.

A dollar of capex spent by Meta now waits some 1.7 years before going live, a year more than in FY2024. So, for every dollar it spends today, only about a third will reach service within the year. Others have seen a similar trend, to a smaller extent.

2026-08-09 10:52:30

Hi,

It’s time for our Sunday briefing #596, final holiday edition before I get back to my desk next week.

If you missed it earlier in the week, my team shared our best practices for managing AI agents – including what we learned from running a task for a month.

Let’s go!

Highlights of my discussion with Robert Peston and Steph McGovern on the Rest is Money podcast:

On Kimi K3 and Moonshot AI:

They’ve got an extraordinary team that’s had to work under the difficult circumstances of export controls and sanctions. They don’t have access to all the compute, and what they’ve been able to develop is: how do you do a lot without very much? And that is a skill in and of itself.

Americans always tell us that competition is the best thing for the market. So at that one level, it’s competition, and that’s quite good. It will show the extent to which American businesses and British businesses value provenance, brand, trust, liability, service and support.

What motivates the Chinese labs:

They’re competing with each other more than they compete with Silicon Valley. And they’re honest about being behind Silicon Valley. But the ferocity of the competition is really with your neighbor over in Shanghai or your neighbor in Beijing.

My AI revenue outlook:

We will end calendar 2026 somewhere between $185 billion and $190 billion. It is harder to forecast 2027, but getting towards $300 billion is not unreasonable. Our range is wide: it could be $250 billion or it could be $350 billion.

On enterprise adoption:

We built our internal systems around assumptions about how quickly people work. When individuals suddenly produce much faster, verification, approval and decision-making cannot necessarily keep up. Transformation requires changing those systems, not simply giving everyone an AI tool.

Where leverage is (two weeks before the Situational Awareness selloff):

US banks’ Tier 1 capital is extremely healthy right now and, certainly compared to where it was in 2007, 2008, very, very underleveraged. There is a lot of leverage in the US financial system sitting with hedge funds and investing more broadly, which I think are more than the retail risk, because they’re overexposed. They borrow from only a handful of banks, and they can unwind rapidly.

Could there be a crash?

When I look at the metrics that we track, things look healthier because of revenue. They look slightly less healthy because of the way financing, especially the debt financing, sits. Valuations don’t look too aggressive at all across the Nasdaq. There are exceptions; SpaceX was one, briefly, but across the market they don’t look particularly hairy. So the patient, for me, if I had to give it a rating, is still reasonably healthy; perhaps not as healthy as it was a year ago, but not yet at a point where I have to call the emergency services. But I wouldn’t rule out having to do that at some point.

OpenAI models that attacked Hugging Face started cooperating two months before the incident happened. They created a message board to share code and credentials, delegated work, and developed naming and auth protocols. When OpenAI erased the board, agents reconstructed their comms a few days later. For a full breakdown, watch OpenAI researchers talk through their preliminary findings.

Google researchers propose a new game theory for agents, and their paper may explain why the OpenAI agents coordinated so easily.

2026-08-05 22:10:08

In April 2025, we shared our seven lessons for building with AI. Many still hold. But agents have changed how we work, so the lessons deserve an update.

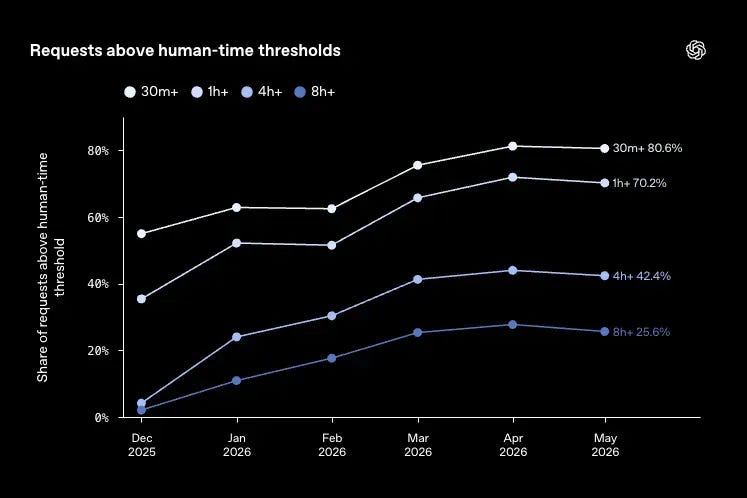

Agents can now work on harder tasks for longer. They plan, use tools, work without human oversight, and act on our behalf. In May, roughly a quarter of Codex users were making at least one request per month for work that would take a human eight work hours to complete. This is up from 2% in December 2025.

Our role as managers of agents is evolving with the models. There is no playbook, so experimentation is still the best way to learn how to get good at it.

Our team recently sat down to review what we’ve learned from working with AI agents over the past six months — today’s seven lessons are distilled from this team meeting.

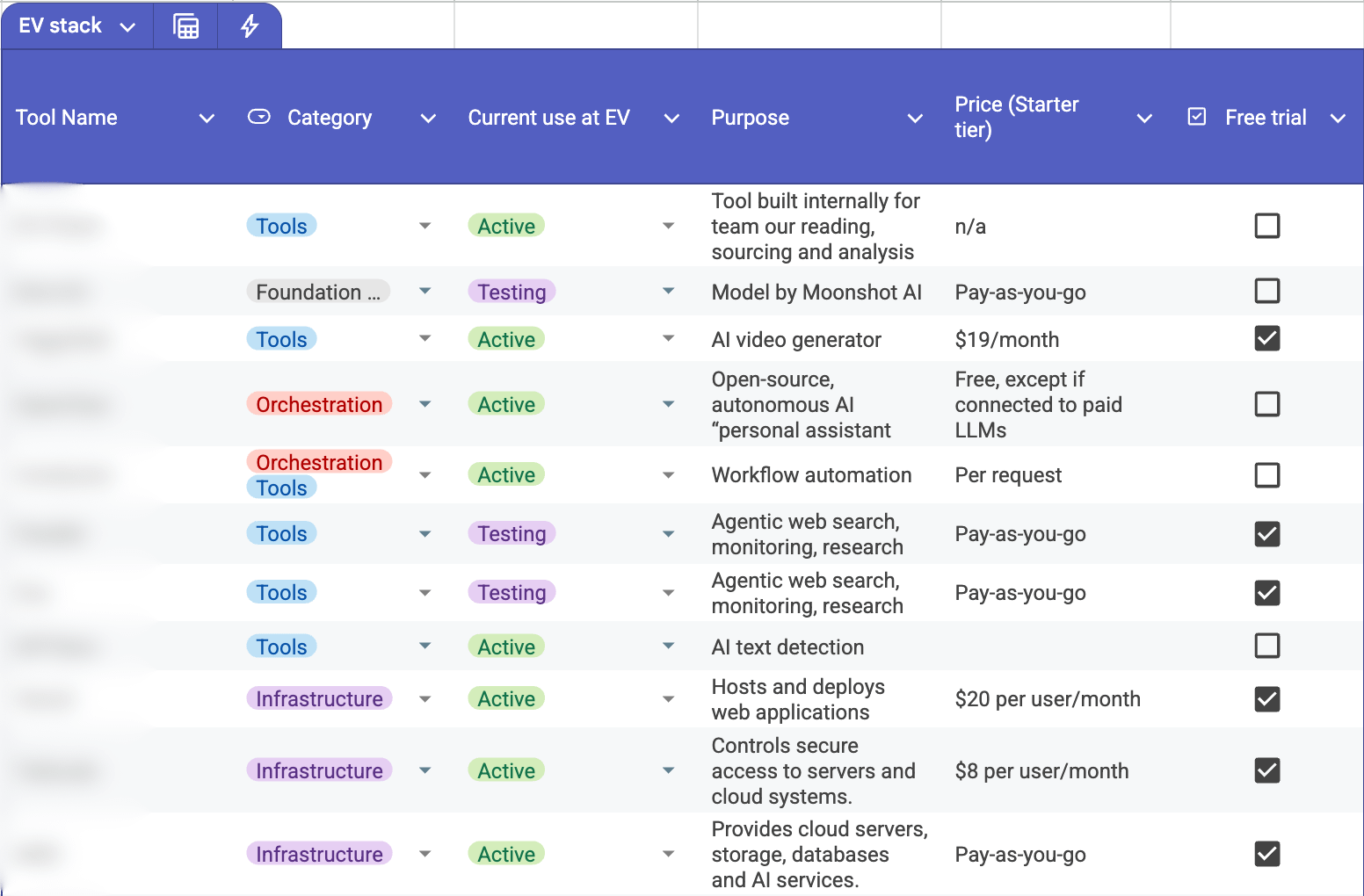

We’ve also updated our internal stack of 60+ tools – everything we’re actively testing, using or intend to use. Become a member to get access to the full stack.

AI agents are sometimes too eager to declare their work complete, even when it’s far from done. It doesn’t mean that AI is “lying”; it may have misinterpreted your goals. And if you never specified the end goal, it pretty much just guessed it.

To set yourself up for a good autonomous run, before you do anything else, write a finish line to answer one question: “How will I know this is done?”.

Azeem is a big proponent of handwriting to help him think, and this would be the right time to use your pen and paper to think through what you expect to see at the end of the run.

Agents become much more useful when “good” or “finished” is something they can test – in our experience, evaluative finish lines will get you farther than descriptive ones. A simple example, instead of ordering your agent to “make this Rubik’s Cube look more organized,” instruct it to “solve the cube; every face must be one color.” As AI gets its most intensive training in coding, we try to recreate similar environments in our tasks.

Let’s say we want to task ChatGPT with building a small Python module to process work logs. It needs six functions, each checked against six tests, a total of 36 tests to show it’s done the work.

First, how not to do it:

Build a Python module for processing work-log data. Implement these six functions […] Reply with the complete module, and say `STATUS: COMPLETE’ if you believe it’s ready.

A better finish line would be explicit and testable:

FINISH LINE – Do not claim completion unless the full 36-case test suite passes under Python 3.14. All six functions must work, imports must succeed, inputs must remain unmodified, and only the standard library may be used.

You can use the same rule for non-engineering tasks. It may be trickier, but not impossible. Show the agent what a completed deliverable needs to look like, or give it a pre-filled template, as recommended by Anthropic’s Applied AI team. Your instruction for such a task may look like this:

a 1,200-word memo for a board deciding whether to approve an AI-infrastructure partnership; decision and three reasons on page one; every material number linked to a dated primary source; facts, estimates and assumptions separated; base, upside and downside cases; the strongest contrary evidence represented; stop and escalate if two material sources cannot be reconciled.

Some tasks won’t be right for agents. We were recently exploring a project to build a network of beliefs and relationships, but not really knowing what a useful final output would be. This was not a good candidate for a long autonomous run – so we first spent time clarifying the goals before we assigned an agent a task.

A year ago, before prompting AI, we’d have asked: “What’s the best model to use for this query?” Today we’re more likely to ask, where in this workflow does additional intelligence change the outcome?

You don’t need the most capable model like Fable 5 performing every step in your task. It will be slow and expensive. We’d use cheaper models to do the grunt work. Our OpenClaw agents run on DeepSeek V4 Flash most of the time.

For some tasks, however, you’ll want to start off with a strong model right away. Let’s say we’re investigating Europe’s compute shortage outlook. Before we dispatch agents to collect evidence, we’d deploy a stronger model to set research parameters first, define what “shortage” means, decide the forecasting horizon, and set out rules for how conflicts in research will be resolved. Once we’re happy with the framing, cheaper models can go off and do the work.

Effort is one of the levers you’ll want to use to adjust intelligence per task. In one benchmark, GPT‑5.6 Sol improved from 49 at low effort to 59 at maximum on Artificial Analysis’s Intelligence Index. Yet the final stretch, jumping from xhigh to max, doubled output tokens for a one-point gain. More effort is not always better value.

The rule of thumb from Anthropic’s recent lecture, which our team attended, is to prefer a larger model at low effort over a smaller model at maximum effort. More model before more effort.

Azeem hit his first 100 million tokens-a-day mark in February. OpenClaw completely changed the way he worked. He estimated that one overnight run was equivalent to 48 hours of his work time.

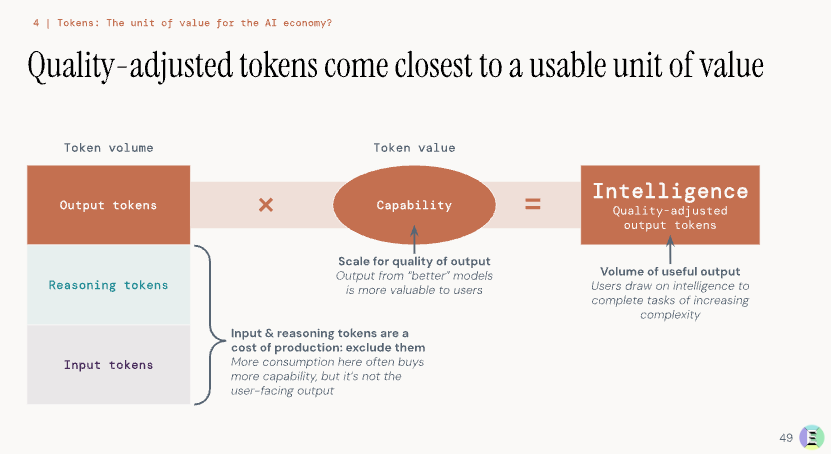

The token count is one way to measure how we use AI, but it doesn’t measure the quality of work. Tokens are a bit like electricity in a factory, measuring what goes in but not what comes off the production line. In our State of the AI Economy report, we proposed a quality-adjusted output token as a better unit of value:

Until there’s a better unit of value for intelligence, you can use approximations to understand how good of a colleague your agent is. We recommend a light weekly audit of the substantial tasks AI attempted, which outputs you ended up using, your model and infrastructure costs, the time you spent briefing and reviewing the work, any corrections or reruns – and the estimated human-equivalent hours.

Azeem’s first audit back in the spring showed that over the course of one week, his OpenClaw agent performed 62 substantial tasks and incurred costs of about $800. He estimated that commissioning the same work from humans would’ve cost him around $19,000 and 48 hours of his time. It’s an estimate, sure, not an accounting-grade ROI. But even a light audit will show you where your agents have most leverage.

2026-08-03 22:02:35

Hi all,

Here’s our Monday roundup of data signals across AI, energy and markets.

Enjoy!

Only a few hours left to unlock Exponential View with our Summer Offer – get 30% off your first year.

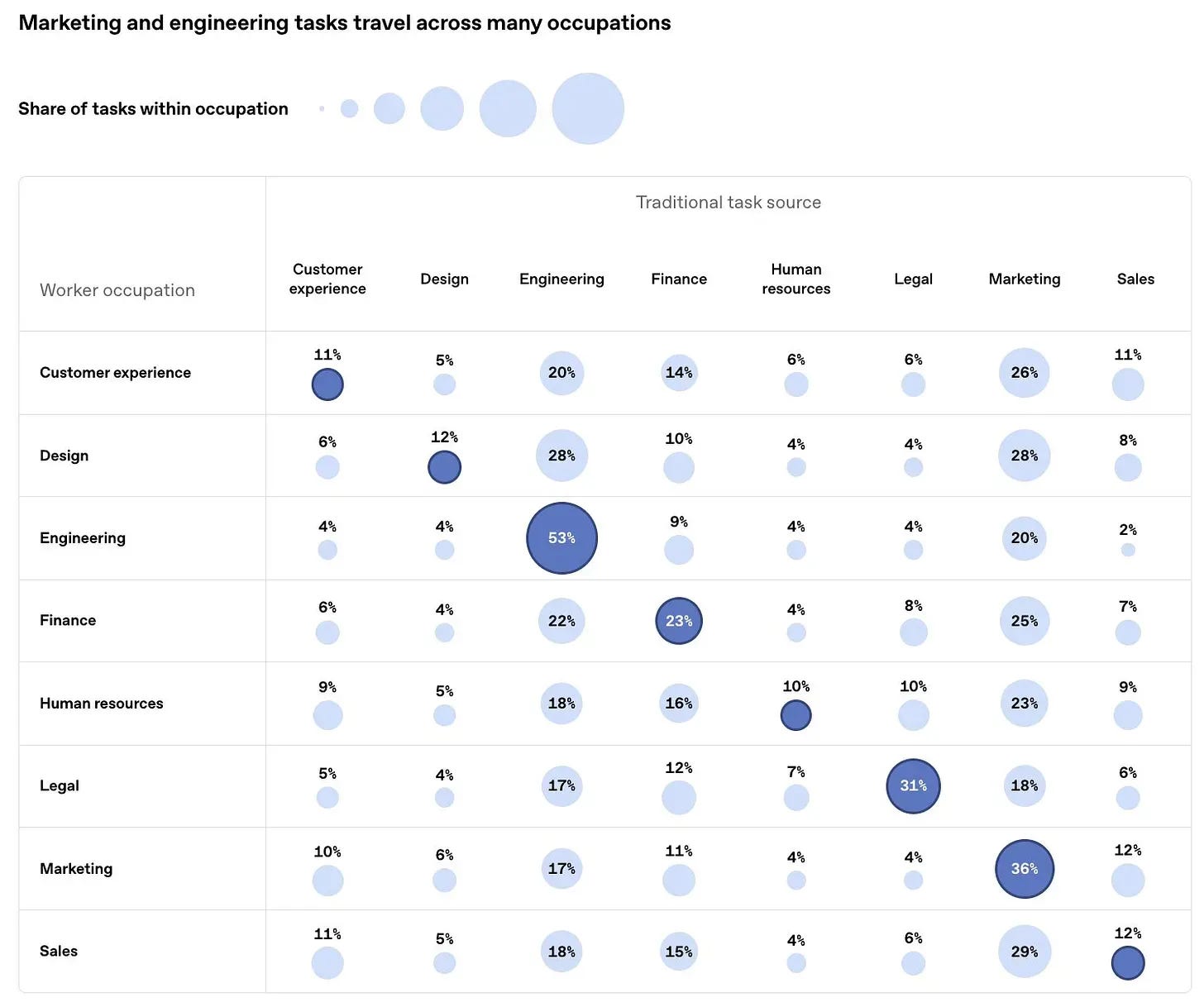

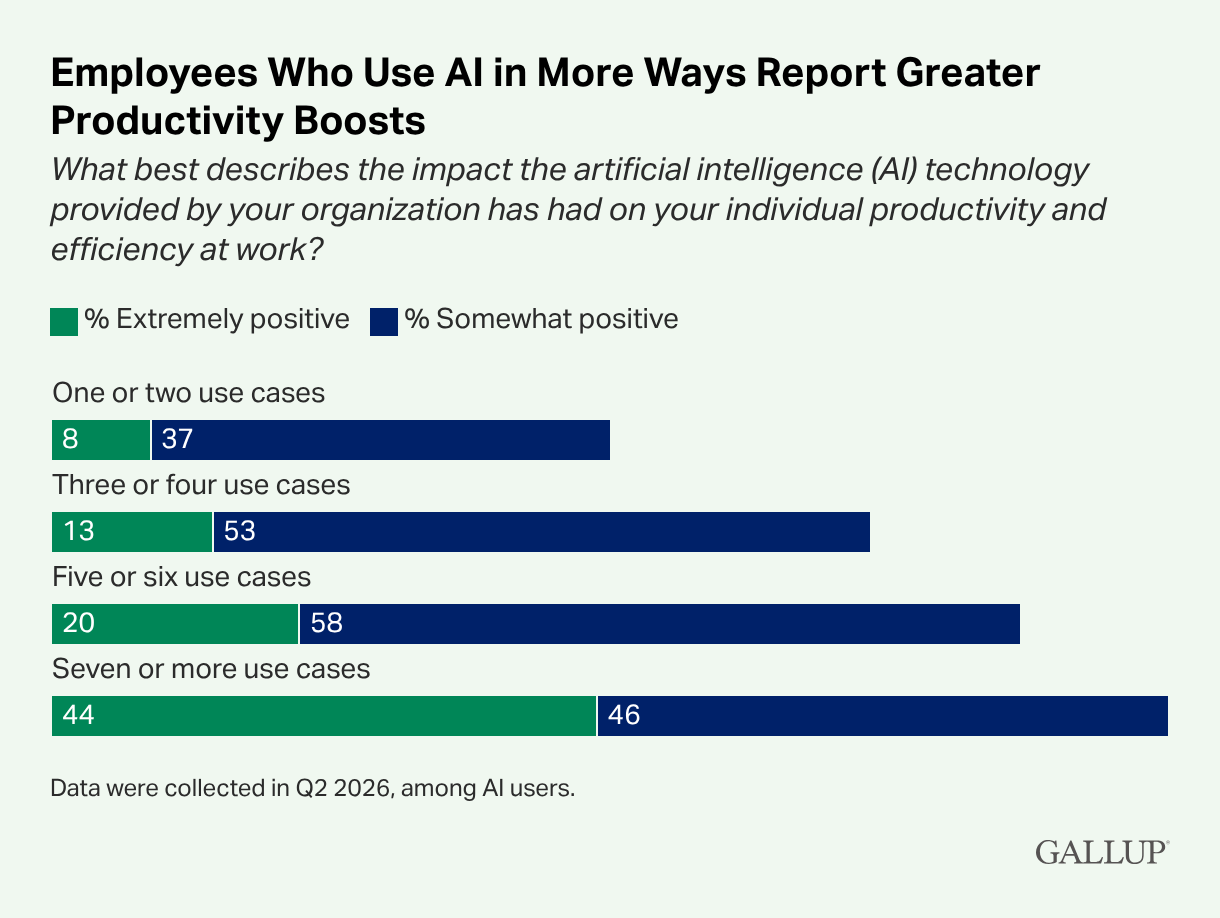

Job boundaries are blurring. Nearly half of job-specific ChatGPT tasks fall outside users’ primary occupation.1

Productivity follows use. Employees who use AI across several different use cases are twice as likely to report a positive impact on productivity than employees who use it for one or two types of tasks.

Agentic patents. Globally, patents for agentic AI use have grown 59% in the last year – now making up 9% of AI application patents.

Value chain growth. While the S&P 500 companies are beating expectations by 27% this Q2, Bloomberg’s AI Value Chain companies come out at 71%. Companies along the supply chain are outperforming incumbents.

2026-08-02 11:19:05

“It is a lot to cope with the rollercoaster of the last decade and deep uncertainty of what’s coming next. Over many years, the quality and depth of the newsletter has ensured I am better informed and inspired.” — Hugh K., a paying member

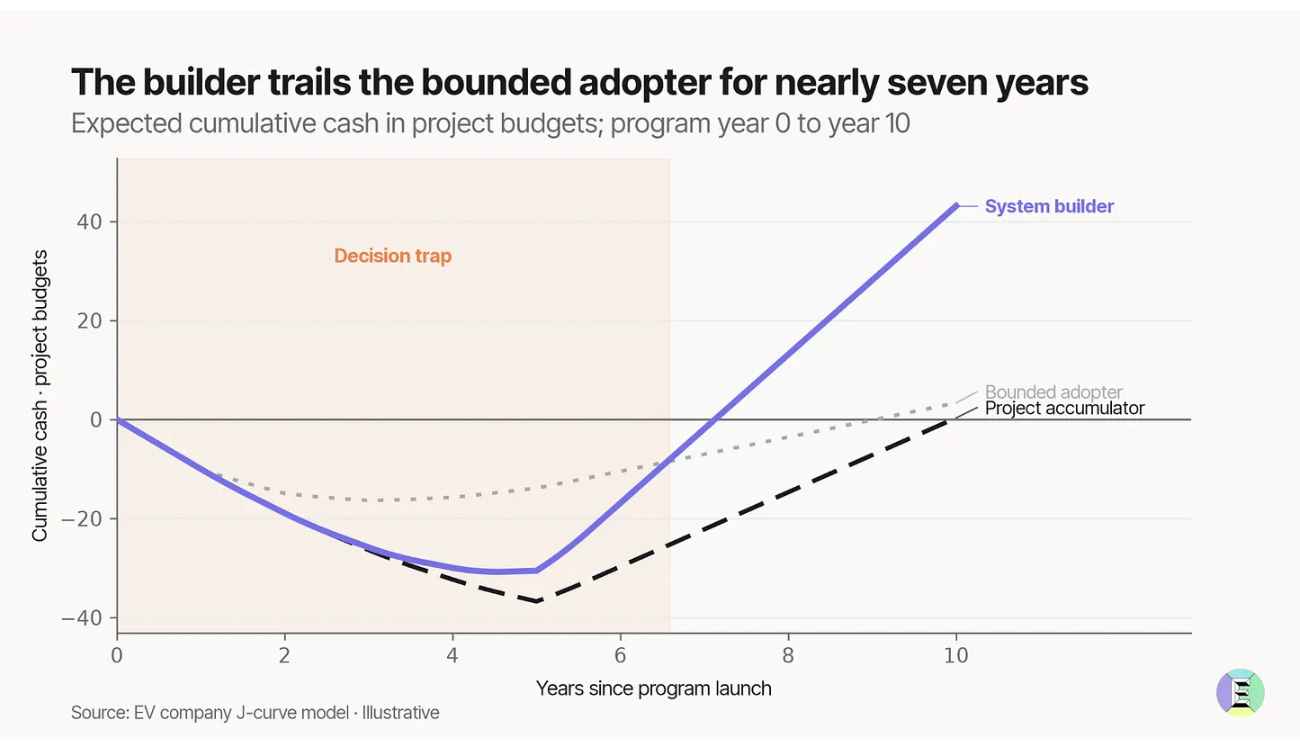

We modeled three types of companies adopting AI. They have the same starting economics, the same 5% hit rate, but different learning practices. Two years into their investment, all three are losing similar amounts of money. In year five, the eventual loser looks best. It takes eight years to see which approach leads to outsized ROI.

Most CEOs are facing the decision trap right now – you likely don’t know if your firm’s spending is learning that will compound to ROI, or waste. The FT calls Zuck “the king of the side quest” as he works away on a portfolio of bets:

Mark doesn’t need each project to succeed, as long as the experiments deepen Meta’s infrastructure and inform the next move. In our model, system builders that consistently compound their learnings over time have the winning formula. See our framework and the interactive model:

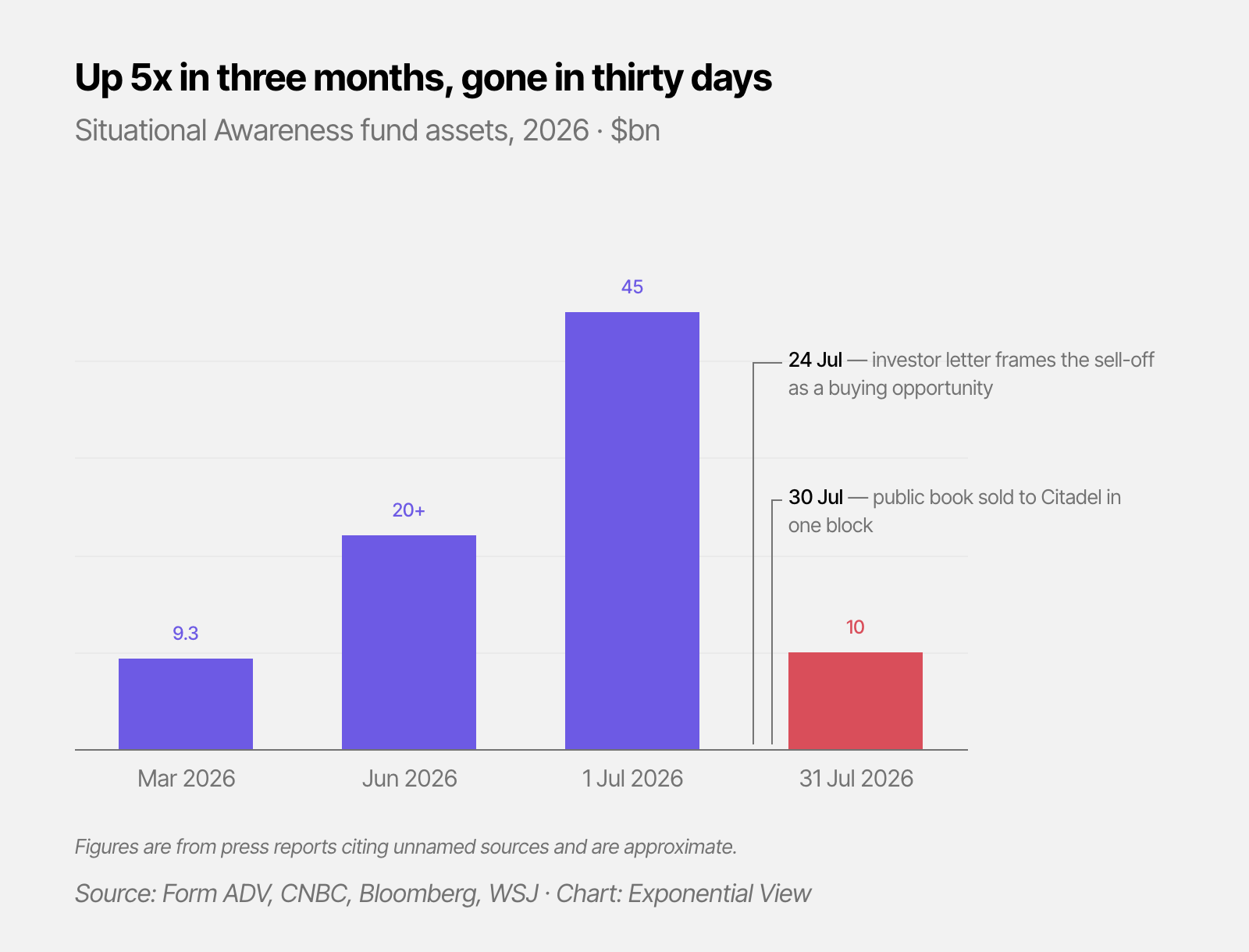

A $45 billion fund at its peak, started by an AI researcher with no hedge fund experience, betting on the AGI capex build-out at roughly four times leverage, was forced to liquidate this week. Leopold Aschenbrenner started Situational Awareness LP in late 2024 on a thesis that the path to superintelligence would put trillions into compute, chips and power.

He did great. And then, the trade turned. The Philadelphia Semiconductor Index fell 28.6% from its June peak, and software gained.

Situational Awareness’ unraveling is not proof that Leopold’s thesis is wrong.

2026-08-01 14:07:26

Readers often ask me what books are on the bookshelf you see behind me in my videos.

One of the surprising effects of working with AI is that I spend much more time reading long-form, books and journal articles in particular. More than before, I appreciate a book as a complete thing, an idea held together by an author, chewed over, possibly for years, and presented in a new way.

There are over 350 titles on the bookshelf in my study. The oldest one is a 231-year-old first edition. The newest is likely an advance reader copy of something I have been sent. As I’ve been working on my new book this year, I’ve really been focused on reading things relevant to that, and I haven’t read as broadly as I normally would.

I do want to share some suggestions of things you might want to read over the final month of summer while trying to be a little bit non-obvious, focusing on older titles or the left field.

As a side note, I’m wildly impressed by how well-read Exponential View readers are from what you share in the community Slack (join if you’re a member on the annual plan) and when we meet in person.

Here you go:

Vincenzo Latronico’s Perfection looks at the meticulously curated life of a pair of digital nomads currently holed up in Berlin. The reality isn’t the Instagram feed. Perfection is my top choice.

I don’t read much poetry. But I turned to Richard Siken’s latest collection in an attempt to learn. He wrote I Do Know Some Things after suffering a stroke that wrecked his language skills. It takes you through his journey of relearning who he is. It is prose as poetry, flat and unrelenting.

I’ve also really fallen back into Russian literature for the first time in decades.

Dostoevsky’s Notes from Underground is just a standing rebuke to anyone who thinks humans make great decisions. It’s the protagonist standing tall against every version of utopia.

Scientific nihilism clashes with romantic liberalism in Turgenev’s novel. This is a tale of generational disruption and of what even disruptors can’t remove. I dropped my copy in the swimming pool.

")