2026-07-31 23:53:49

A great deal of the discussion of the so-called benefits or problems with AI comes down to the theoretical jobs that are (or are not) lost as a result of things LLMs can (or cannot do), or the equally theoretical productivity benefits that’ll come from using LLMs in place of (or in conjunction with) humans.

Anthropic’s Economic Index and OpenAI’s Economic Research Exchange are marketing operations that exist to propagate the (wrongheaded) belief that LLMs are either leading or will soon lead to massive economic or productivity shifts, even though little or no actual evidence exists to show that this is the case, other than the occasional story about LLMs make people worse or slower at their jobs or single lines in studies that are used (incorrectly) to prove that “AI is making it harder to find a job for young people.” In fact, Anthropic’s Head of Economics recently said there was “no material increase in the unemployment rate to date.”

These conversations materially detract from the actual harms or effects of AI, and exist only to make you scared that AI will take your job. They do not have any vested interest in expressing the actual economic effects of AI, which are, at this point, a simmering cauldron of different speculative bets on whether or not LLMs — a definitively niche technology — will create or become general-purpose software (per Roger MacNamee) that scales into the next Google Search, iPhone, or Microsoft 365.

As I’ve argued again and again, the AI industry’s revenues are, outside of Anthropic and OpenAI, incredibly small. Even in Exponential View’s deliberately-pro-industry analysis, there’s only around $110 billion in trailing twelve-month revenues across the entire industry, including OpenAI and Anthropic’s cloud spend.

For those counting at home, that’s $12 billion less than the $122 billion OpenAI raised in March, and a full $145 billion less than all AI startups raised combined in the first quarter of 2026.

Anthropic and OpenAI want you to talk about the theoretical so that you don’t focus on the tangible — their hundreds of billions of dollars’ worth of commitments, said commitments effects on the remaining performance obligations of hyperscalers and chip manufacturers, and the sheer scale of venture capital’s investment in AI, which (as I’ve argued in the past) largely allows for massive on-paper gains with little or no hope of liquidity.

To put this bluntly, I believe the entire conversation around AI’s theoretical relationship to jobs to be masturbatory and a conscious attempt to avoid having a messy conversation about the scale of the actions taken based on the flimsily-founded promises of AI labs and hyperscalers.

Today’s piece will dig into the true scale of the money needed to make AI make sense, by which I mean how much OpenAI and Anthropic will need to meet their commitments, how much money hyperscalers will need to pay off their investments, venture capital’s true exposure to the AI bubble, and what will have to go right for the bubble not to be, well, a bubble.

I’ll also make the case that the longer the bubble continues to inflate, the harder the basic economic puzzle of AI becomes to solve, as creating and deploying infrastructure becomes vastly more expensive — meaning that in order to achieve profitability, hyperscalers and neoclouds need to charge significantly more for compute than before, and the only two real potential customers are ones that cannot pay for it.

This will be a more more-pointed newsletter than usual, focusing on hard numbers and harder truths.

Let’s get it on.

2026-07-29 00:29:37

If you liked this piece, you should subscribe to my premium newsletter. It’s $70 a year, or $7 a month, and in return you get a weekly newsletter that’s usually anywhere from 5,000 to 18,000 words, including vast, detailed analyses of NVIDIA, Anthropic and OpenAI’s finances, and the AI bubble writ large. My Hater's Guides To the SaaSpocalypse, Private Credit and Private Equity are essential to understanding our current financial system, and my guide to how OpenAI Kills Oracle pairs nicely with my Hater's Guide To Oracle, as well as the Hater’s Guide To Oracle (Part 2).

Subscribing to premium is both great value and makes it possible to write these large, deeply-researched free pieces every week.

Soundtrack: Queens of the Stone Age — Infinity

Two years ago, NVIDIA CEO Jensen Huang said that “the more you buy, the more you save,” referring to its new (at the time) Blackwell GPUs that would “reduce LLM inference operating cost and energy by up to 25x.” Two years later, those supposed gains have been pared back to 10x, based on case studies with private inference providers that do not share their margins and are most-decidedly not profitable, and absolutely nobody seems to mind that NVIDIA overstated the gains on Blackwell (in a vacuum, in specific circumstances) by 150%, partly because these numbers are utterly meaningless, and partly because the media in most cases ardently refuses to criticize this company.

Blackwell being “10x better” than Hopper does not appear to have made any AI startups profitable (or even more profitable), it does not appear to have lowered anyone’s costs in a way that we can measure using dollars and cents, and as a result, I feel very little when I’m told that Vera Rubin provides “up to 10x more tokens per megawatt,” especially as that was with DeepSeek R-1, a year-and-a-half-old open source model.

Nevertheless, all of this is immaterial to the larger problem that none of this appears to have resulted in anything tangible other than horrendously-overstuffed balance sheets and spuriously-puffed stock prices.

Hyperscalers will have sunk over $1.3 trillion dollars into generative AI by the end of 2026, and have plans to spend a trillion dollars more next year. On a very rational level, nothing that large language models (LLMs) have done, do or will do in the future can or will ever bring in the more than $2 trillion (or more) in brand new revenue that will be required to make any of this worth it.

To be more specific, between March 2022 and July 2026, Meta, Google, Amazon, and Microsoft added over $850 billion in property, plant, and equipment (PP&E), nearly tripling their PP&E from $498 billion or so, and in a period where they spent over $1 trillion in capital expenditures.

In that same four year period, none of them have disclosed their actual revenues from AI or AI-related services, and, as of their latest quarters, capital expenditures now represent 24.4% of Amazon’s, 33.7% of Meta’s, 37.3% of Microsoft’s, and an astonishing 43.4% of Google’s revenue, a number that’s steadily increased over the last three years.

They’ve also added over $307 billion in on-balance sheet debt, leaving them with a total of $557 billion, doubled from $250 billion or so in March 2022. I mention on-balance sheet because Nikkei reports that Meta, Google, Amazon and Microsoft have over $1.35 trillion in off-balance sheet debt — either data centers/GPUs yet to be delivered, or debt raised via SPVs that shift the actual “ownership” of them over to another party as a means of making them look less-indebted than they really are.

To be clear, it’s totally fine accountancy-wise to not include leases or commitments yet-to-commence, but it’s very important to know how big an anvil hyperscalers are conjuring above their heads. Google, for example, has $811 billion in contracted future spending commitments as of its latest quarter, increasing by a dramatic $661 billion ($478 billion or so in the latest quarter) in the last 6 months, and Meta has over $237 billion in non-cancellable contractual commitments.

Over $167 billion of that on-balance sheet debt has been raised in bonds across Google, Meta, and Amazon, with its $25 billion bond sale from July receiving (per Bloomberg) a cool reception, with “demand [settling] at 1.6 times the deal’s size…[and to] put that in perspective, US high-grade corporate deals have seen orders average around four times their size this year.”

For some further perspective, per Freedom Broker’s Saken Ismailov, there was around $100 billion of demand for $20bn of Google’s three to fourty-year-long bonds (5x) and around £9.5 billion of demand for its £1 billion 100-year bond sale (9.5x).

As of last week, Google’s century bond has already lost 10% of its value.

This is a problem, as all four are certain to become repeat visitors to the bond markets. Herman Chan of Bloomberg Intelligence estimates that hyperscalers will need to raise $1.5 trillion in investment-grade debt in the next five years just to keep up with their trillions in estimated capital expenditures.

To make matters worse, hyperscaler bonds are, to quote Bloomberg, “...underperforming on almost every metric,” and are “in the red on average,” though that includes Oracle, whose credit just got downgraded to a single rung above junk by S&P Global.

Sidenote: As an aside, whenever you hear bonds are measured in something called “spreads,” it’s how much more an investor would expect to get paid above the current US treasury bond rate in “basis points,” with 100bps referring to 1%.

The thing is, when treasury rates go up, bond prices go down, even though you’re still getting paid on the coupon (the yield, IE: the money it pays regularly) and the payoff at the end of the bond’s life. As a result, spreads exist to tell you how much more or less it pays than an equivalent US treasury bond, or a similar ultra-low-risk government bond.

Bonds are also generally raised in tranches, in different currencies, at different lengths, which makes their prices less useful than you’d think. Furthermore, bonds can be resold to third-parties, and often for cheaper than the original purchase price — which is something that would happen if people started to get worried about the company not being able to pay back its debts.

Let’s give you a (hypothetical) example. US Treasuries are 5%, and a hyperscaler raises $10 billion in bonds at 6.5%.

The “spread” here would be 150bps — which suggests that investors think they’re mostly safe. In general, 150-300bps is worth keeping an eye on, 300bps+ is worrying, and 700bps+ is a company that the market is concerned about repayment. For example, a high-credit company's bonds would have an average OAS of 20-80bps, or an investment grade (like Amazon at 118bps) would have between 80-150bps.

And, well, then there's the rest.

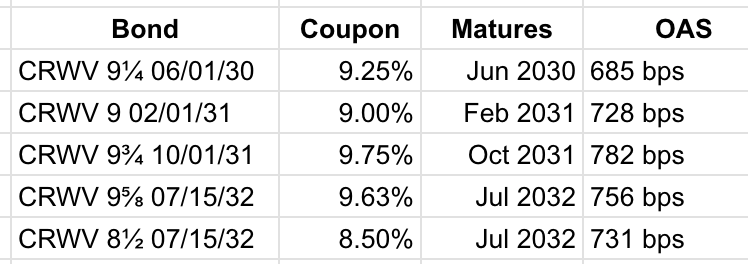

For example, CoreWeave’s $1.25 billion in bonds raised in June 2026 currently sit at an option-adjusted spread of 756bps, despite being issued somewhere around 540bps on the day of issuance. Put another way, bondholders have dumped the shit out of them in the last month and have material concerns that CoreWeave won’t pay. To make matters worse, the average for its bond/credit rating (Ba3) is 200-400bps, meaning the market is really, really concerned about whether CoreWeave pays its bondholders.

All of this is a way of telling, in realtime, how much riskier a bond might be than the rock-solid guarantee of the US government (or whatever currency it was raised in). When I say “option-adjusted spread,” that’s a forward-looking model that strips out things like if a company can recall (IE: buy back a bond early) a bond to give you a generalized spread that tells you how the market feels about a particular bond.

Things can muddle a little bit depending on the company, or should I say one company in particular.

EDITOR'S NOTE: To be clear, this is an edit to the piece, because I wanted to clarify some stuff and the article I previously linked got things wrong.

Also, thank you to eagle-eyed premium subscriber Clayton for noticing!

So, SpaceX's "investment-grade" bonds (issued in late June) are rated BBB - the lowest level possible - and have an average OAS of around 270bps, with the widest spread sitting at 346 (for its 30-year dated bond). I previously linked to a piece that said it was "trading like junk," and I was completely right in that assessment, but didn't give you, the reader, the juice to understand why.

As of writing, the average spread of Bloomberg's Corporate High Yield Index - which, to be clear, is made up of junk bonds in most cases many rating levels lower than SpaceX - is around 282bps. In other words, Musk's "investment-grade" bonds are trading like junk!

As complex as all of this sounds, it’s all pretty simple: hyperscalers have borrowed a bunch of money to fund AI, to the point that it’s pushing them into cash-flow negative territory, and every time they raise more money, bondholders become more worried about them paying it back, especially given that both Amazon and Google have now gone cash-flow negative as of their latest quarters.

Or, put more-simply, the more they raise, the more it costs.

Then there’s the other, more-obvious problem — the more they buy, the more they spend.

As I wrote in the Hater’s Guide To The Memory Crisis, the sheer scale of Microsoft, Google, Meta and Amazon’s spend on AI data centers has led to a massive supply chain crisis and price-gouging from the triopoly of Micron, SK Hynix and Samsung, with Micron alone bumping prices for DRAM by 60% in its last quarter, shooting up the price of every single kind of RAM possible, at a rate increased by the amount of GPUs and servers that hyperscalers buy.

To give you a sense of how memory hungry AI is, single 72-GPU GB300 NVL72 AI server has over 20 terabytes of high-bandwidth memory (used almost exclusively in GPUs and other AI chips), and 17 terabytes of the LPDDR5X RAM used in mobile devices, and a gigawatt data center has thousands of those NVL72 servers (or something similar). Moreover, that high-bandwidth memory that AI GPUs use requires more wafer space during manufacturing — further reducing the amount of manufacturing capacity for other kinds of memory.

This naturally creates a vicious cycle. The more AI servers that hyperscalers buy, the more demand they create for RAM and high-bandwidth memory, which increases the price of RAM and HBM, which makes the AI servers more expensive, which means hyperscalers need more money, and because AI has yet to provide meaningful improvements in revenue or cashflow, they’re forced to raise more debt.

The more they raise that debt, the more expensive that debt becomes, and the more of that debt they use, the more of it they need, because the more they spend, the more the stuff they’re buying costs, which means they need more debt.

And, to be clear, I’m talking about some of the best-capitalized companies in the world with some of the best credit in the world. Things get magnitudes harder and more expensive for a neocloud like CoreWeave (or a counterparty), or a data center SPV, or anyone that isn’t backstopped by a hyperscaler, like Google’s backstop of Cipher Mining’s data center for Anthropic.

Are you beginning to see the problem yet?

You can dance around making whatever noises you want about future GPUs or cadres of data centers magically giving somebody the margins you crave, but it appears that using AI only seems to be getting more expensive for hyperscalers, the companies that rent the GPUs, and basically anyone running a business using AI models.

Spare me your anecdata! Every AI startup is unprofitable, and every time somebody describes an AI company “getting profitable” it’s during some mythology-adjacent rain dance about mythical 90% gross margins on inference, or, in the case of the data center providers, after they’ve amortized billions (or tens of billions) of dollars’ worth of GPUs.

The problem is that the longer this goes on, the more expensive it gets, and the more extreme the payoff has to be. A trillion dollars of capex and the near-entire capitulation of the media and finance class cannot be justified by “some incremental improvements somewhere that nobody can really understand and an incredibly unprofitable way to let people write software that sometimes is faster but never in a way anyone can capture.”

Every wibbly-wobbly, fan fiction-adjacent analyst note or Twitter screed claiming that we’re in some sort of CPU or GPU supercycle never seems to reconcile with the reality that money doesn’t really seem to come out the other end when you buy something from NVIDIA unless you’re Anthropic or OpenAI. Data center operators have yet to show substantive proof of a sustainable business model renting out GPUs, let alone profits that would justify taking on billions in debt, and the payoff date seems to exist somewhere between “fuck knows” and “never.”

Take CoreWeave, the perennially debt-raising no IT loads refused neocloud, which has raised over $23 billion in the past two years with bond spreads that communicate a near-existential anxiety about the future of the company. Their previously-mentioned $1.25 billion bond raise — raised a little over a month ago — is now trading over 200bps higher than issuance when it was already at a 9.625% yield, which genuinely brings into question how future debt raises will go considering it’s guiding $31 billion to $35 billion in capex for a year and still has yet to build most of the capacity it needs to fulfil its massive backlog.

In fact, CoreWeave’s bond spreads look like a dog’s arsehole after eating a Thanksgiving turkey:

And because it hasn’t built it yet, that means it hasn’t bought all the stuff, and the longer it takes to buy the stuff, the more expensive it’ll get.

That’s also before you consider talent shortages, transformer shortages, electrical grade steel shortages, and generator shortages, which means you’re paying more money for the same thing (or less), likely having to accept whatever quality of material or talent you can get, all while battling to secure power as local authorities begin forcing data center builders to pay their fair share. This just happened in the Midwest, with local regulators in Port Washington, Wisconsin demanding Oracle puts up a $7 billion guarantee (costing it $100 million a year) to protect taxpayers if the power behind its Stargate data center doesn’t get built, largely due to that S&P credit downgrade…associated with it building so many data centers for OpenAI.

Nobody seems to want to discuss that every data center we’re describing is 2 to 3 years in the future, and the market is becoming increasingly impatient and showing signs of non-compliance with the greater AI narrative. The theoretical payoff for anyone buying a GPU in the last 12 months is that sometime in the year 2030 you will, in theory, make somewhere between 30% and 40% gross margins, assuming that you have had near-constant utilization of your GPU infrastructure from an industry where effectively every customer is either an unprofitable AI lab or a hyperscaler trying to keep their theoretical future compute off their balance sheet.

How does any of this work? Has anyone worked that out yet? Because it isn’t working right now, the only reason that any of you think it’s working is because CoreWeave (which lost $740 million last quarter) and Nebius ($399 million in revenue, $8.45 billion in debt) haven’t had trouble raising debt.

Be real with me: do any of you seriously believe CoreWeave exists in 2030?

Remember: its largest customer is OpenAI, either through Microsoft (70% of its revenue), Google (for OpenAI), or its own payments that are paid net 360.

In fact, why stop there — do you think OpenAI will be around in 2030?

I’m not asking these questions to be a dick or because I’m a hater, but more out of a genuine sense of curiosity. Over the weekend, the Wall Street Journal reported that NVIDIA was in talks with OpenAI to guarantee $250 billion in financing for a 10GW data center (allegedly) being built by SoftBank affiliate SB Energy, by which I mean NVIDIA would guarantee the compute payments (as it has with CoreWeave and Lambda but at a much bigger scale) so that SB Energy can raise debt to buy the chips from NVIDIA to rent to OpenAI:

Nvidia’s backing would allow the data-center developer, which is owned by Japanese billionaire Masayoshi Son’s investment firm SoftBank, to raise debt at more favorable terms than it could if OpenAI had no financial backer, since OpenAI has no investment-grade credit rating as an unprofitable private company. The AI company has been in advanced talks to lease the site for several weeks, people familiar with the matter said.

What’s even crazier is that the $250 billion guarantee would only cover lease payments and construction costs, and, per The Journal, NVIDIA is also discussing a deal to finance the $350 billion in GPUs to go inside it. It is unclear how that would happen, who would fund it, how it would get funded, or really anything about the deal.

This is the final boss of circular financing. SoftBank, which owns over $100 billion (on paper) in OpenAI stock, is using its affiliate SB Energy (which OpenAI and SoftBank invested in in May) to raise debt to build a 10GW data center — likely costing more than $500 billion in chips and construction — by getting a backstop from NVIDIA (which invested $30 billion in OpenAI and cited it as a material indirect customer in its 10K), which will also make upwards of $350 billion in revenue from the deal.

If/when this deal closes, SoftBank (which owns more than 15% of SB Energy) will use the contract signed with OpenAI as a way to take SB Energy public, giving both it and OpenAI a massive equity gain, all while feeding revenue from one investment to another investment, at least in theory.

Will any of this happen? God no. SB Energy is a confusing and murky business. SoftBank sold 85% of its shares to Toyota to form a company called Terras Energy in 2023, and it’s unclear if the new SB Energy has anything to do with the old one. Even if it did, neither company named SB Energy has ever actually built a data center, and to my knowledge, nobody has gotten close to building a 10GW data center.

Then there’s the problem of the debt itself. It’s unlikely that SB Energy raises all this money at once, which means that it’s going to fall into the same problem as hyperscalers are facing — that the more debt that AI data centers raise, the more expensive it becomes to raise debt for AI data centers.

That, and the debt markets are already showing their distaste. Back in May, SB Energy (via an SPV called SE Cosmos LLC) raised $999 million in 144A bonds (private debt sold exclusively to qualified institutional buyers) rated BB- (junk) by Fitch and BB+ by S&P Global to buy a former 3M campus and turn it into a 70MW data center, and it only got that with a guaranty from SoftBank Group.

Since issuance, its (option-adjusted) spread has grown from 351bps to 536bps, and that’s for a relatively low amount of debt for a relatively-straightforward data center.

Sidenote: It’s also unclear how that project gets built. Based on TD Cowen estimates, a 70MW data center would cost about $3 billion including chips and construction. The data center, per S&P Global, will be leased to “Silver Bands 3,” a company that, based on the existence of two SoftBank subsidiaries called Silver Bands 4 and 6, appears to be a subsidiary of SoftBank that is renting a data center from a subsidiary of SoftBank.

None of this appears to matter to ratings agencies.

Even with the cast-iron guarantee of mag7 findom NVIDIA, it’s hard to see how SB Energy pulls together what will likely be a succession of different $10 billion debt deals of the course of several years, especially given the above-discussed curdling of the AI data center debt markets.

I also think it’s fairly likely somewhere between nothing and very little happens as a result here, even if NVIDIA offers its backstop.

Per The Journal, phase one of the project is due to be finished sometime in 2028 and have around 800MW of power — and I must be clear that while this doesn’t seem like very much in the grand scheme of things, OpenAI’s Stargate Abilene, a 1.2GW data center that broke ground in July 2024, has energized and monetized no more than three out of eight buildings for a total of 309MW of critical IT load, or about 401MW of active power. Even if the data center has broken ground (which I don’t believe it has), it’ll be extremely difficult to meet that timeline, and at a rate of 800MW every two years, it’ll be more than a decade before it opens.

Sidenote: Hey, this kinda reminds me of something! Back in 1998, Lucent Technologies signed its largest deal ever — a $2 billion “equipment and finance agreement” — with telecommunications company Winstar, which promised to bring in “$100 million in new business over the next five years” and build a giant wireless broadband network, along with expanding Winstar’s optical networking. In practical terms, Lucent would lend money to Winstar to hand back to Lucent to buy stuff from Lucent.

In 2001, Winstar would file for bankruptcy and sue Lucent for $10 billion in damages after it failed to give it $90 million in promised funding so it could keep up with debt that was, at least in part, also owed to Lucent. Lucent was eventually forced to pay back $188 million in loans and later pay $300 million in restitution.

NVIDIA has been smart enough to not be the actual bank of last resort, choosing instead to do equity investments and give backstops. Nevertheless, the consequences might be the same. When Winstar collapsed, losses and impairments totalled 15 cents per share in Q2 2001, per The Register.

Forgive me if I feel a little dismissive, but it’s a little hard to take any of this seriously! This theoretical data center with theoretical funding built by a SoftBank affiliate to rent GPU capacity to a SoftBank investment with the backstop of an OpenAI investor that stands to make hundreds of billions of dollars is equal parts ridiculous and fantastical.

Oracle is burning its company to the ground to build data centers for OpenAI in pursuit of a $300 billion, five-year-long compute deal that was meant to begin in June 2026 and currently has 5.6% of the 7.1GW of capacity it needs to make that revenue, even with Larry Ellison throwing every dollar he has (in addition to tens of billions of debt and laying off 21,000 people) and pulling every favor imaginable.

Though it’s kind of a straggler in the cloud space, Oracle still has a ton of experience in building data centers, and if it can’t get these done within a reasonable timeframe, I struggle to see how SB Energy — a company that has, as a reminder, never built a data center before — is meant to build the largest data center campus in history, assuming it can raise the money, which it will have a great deal of trouble doing.

In any case, I won’t be surprised if a “deal” is signed, and if some sort of debt financing takes place, but it’s going to be tough for SoftBank and its various tendrils to raise the $30 billion or more for Vera Rubin chips, let alone the $14 billion for construction.

To be clear, I also don’t think this deal has very much to do with OpenAI or generative AI. SoftBank wants SB Energy to lock up the deal so that it can push it to go public and unlock some much-needed liquidity. NVIDIA wants to lock up (theoretical) hundreds of billions of dollars of revenue, and doesn’t really care if the data center gets built as long as CFO Colette Kress can find a way to book the GPU sales as revenue.

This is all a very, very bad sign for the AI industry at large. If there were real, diverse, meaningful and consistent long-term demand for generative AI or NVIDIA GPUs, NVIDIA wouldn’t have to create the world’s first circular financing within a circular financing, or need to take money from one of two different massive companies with either junk or junk-adjacent credit putting their futures in jeopardy to pay it.

Oh, right, there’s also the other problem: how the fuck will OpenAI pay for this capacity? If we, based on my estimate of $75 billion a year across the 7.1GW of Stargate data centers, assume that OpenAI would pay around $10.5 billion a gigawatt of capacity, that’s $105 billion a year in compute costs just for SoftBank, or a little less than half of the $122 billion OpenAI will have raised this year, with $60 billion of that coming from NVIDIA and SoftBank.

Nobody has an answer here! Every time one of these insane theoretical deals is announced it’s discussed like building gigawatts or raising hundreds of billions of dollars is both easy and effectively already done. It doesn’t matter that NVIDIA claimed it was investing $100 billion in OpenAI last year to build 10GW of data centers in a deal that never happened (despite CNBC claiming the first $10 billion would close within a month of the announcement!), or that OpenAI can’t afford it, or that OpenAI has been part of no less than three different announced-then-never-completed deals. The media has been fully trained to simply accept whatever slop NVIDIA shovels down their throats, and to avoid discussing messy things like “how this happens” because that wouldn’t be considered objective.

Allow me to be subjective for a second: this deal is bullshit. AI data centers are taking 18-to-36 months to build, and capacity is clearly coming online at such a slow rate that it’s hard to understand why people are still buying more GPUs, other than the fact that once they stop everybody has to admit that it was all kind of a huge waste of money. The media remains ill-prepared for this moment, because of (to quote Ed Elson) a cult-like worship of the wealthy, where the assumption is always that they’ll work it out, and anything they say that doesn’t work out is just a result of the complexity of businesses.

Yet this is actually a very, very simple situation. NVIDIA needs to keep sustained and ever-growing demand for its GPUs, and the only way that it can keep doing that is either by creating and constantly funding neoclouds (who, to quote CEO Jensen Huang, would not exist if NVIDIA didn’t support them), creating massive circular deals focused on OpenAI, or relying on hyperscalers that have run out of hypergrowth ideas and thus must keep building data centers to avoid admitting that to the markets.

You’ll notice that nobody other than hyperscalers, Anthropic, and OpenAI seem to be demanding gigawatts’ worth of compute, and that’s because outside of the AI labs and those supporting them there’s less than a fifteenth of the demand necessary to support the 190GW of planned data center capacity.

As a result, the only way that NVIDIA can continue beating and raising each earnings season is to manufacture these massive deals, all to avoid discussing the blatantly obvious truth that diverse demand does not exist. Why else would it have over $30 billion in commitments to rent back its own GPUs?

Sidenote: While Thinking Machines theoretically might “deploy” a gigawatt of Vera Rubin-powered capacity at some point, it only appears to be doing so because NVIDIA invested in it, and as ever, nobody has ever asked questions like “how?” or “where?” or “with what money?” because, at 360KW of IT load per NVL72 rack, assuming a PUE of 1.3, that’s 2136 VR200 NVL72s at $7.8 million a piece, or $16.66 billion in chips alone for a company that’s only raised $2 billion. Nothing is happening here. No data centers announced, no plans to do anything, just put the story in the bag and pump the stock! Don’t think! Only growth matters!

While NVIDIA continues to sell remarkable amounts of GPUs, it does so to an increasingly less-diverse customer base — 54% of its revenue and 64% of its accounts receivable (IE: orders shipped, revenues booked, but money not received) come from three customers. While its new (as of its latest quarter) “ACIE” (AI clouds, industrial & enterprise) segment might feign a little variety, this includes basically any SPV or VIE or neocloud that NVIDIA itself has helped prop up.

NVIDIA’s revenues are, for the most part, propped up by FOMO rather than any real relationship to revenues, productivity, or reality, much like the rest of the semiconductor companies profiting off of AI. Every move it makes is to further propagate the sense that if you don’t buy GPUs and build AI data centers that you’ll be permanently left behind — which is why it plans to invest $5 billion in mysterious AI startup Safe Superintelligence, a company with no products or plans other than to rent NVIDIA GPUs from someone at some point.

Outside of those building the infrastructure, the only people making a profit (or really much money at all) are the bankers and private credit funds underwriting data center debt, the ratings agencies getting paid to rate that debt, and any VC that’s been lucky enough to get paid out across the (very) few acquisitions of the AI bubble so far.

Otherwise, basically every layer of the AI industry exists to be exploited by the layer above it. AI startups and enterprise customers pay Anthropic and OpenAI on a per-million token rate (losing money in the process) so that Anthropic and OpenAI can rent GPUs from hyperscalers (losing tens of billions of dollars a year) so that hyperscalers can buy a trillion or more dollars’ worth of GPUs (putting them in such a hole that they’ll never, ever be able to make the money back).

It’s all deeply unsustainable, vile and wasteful, and only made possible in a lax regulatory environment, a captured tech and business ecosystem, and an economy dominated by growth-at-all-costs thinking.

As I’ve hinted at previously, AI needs to become something altogether more successful, powerful and financially viable than it is today, and that “something” grows ever-larger with every new massive data center deal and funding round and egregious statement from Clammy Sam Altman.

Hyperscalers will, by the end of the year, have sunk over $1.5 trillion in capital expenditures and equity investments into Large Language Models that have yet to provide good enough revenues to actually disclose.

Their actual AI products — outside of providing compute to Anthropic and OpenAI — are mediocre also-rans that range from embarrassing to actively harmful, deeply unremarkable simulacrums of whatever OpenAI or Anthropic’s product du jour might be, the latest of which are the (deeply embarrassing) attempts by Microsoft and Meta to make their own OpenClaw products. While people might use Google AI overviews by accident or accidentally click the Gemini icon when they’re using Google Docs, the actual outcomes of Google’s various LLMs are unexceptional, much like every hyperscaler product.

The only really successful product — GitHub Copilot — only grew to a few million paying users because it subsidized their usage, allowing them to burn more than 25 times their monthly subscription fee, leading to user revolts when they were inevitably switched to token-based billing.

Do not confuse “some revenue coming out of these products” with any kind of success. Microsoft, Google, and Amazon have tens of thousands of salespeople whose job is to harass their customers into buying AI add-ons, on top of simply changing their product categories to force AI services into regular subscriptions as an attempt to claim that they have “AI revenue.” The fact that none of these companies are willing to disclose their actual quarterly revenues for AI is a sign that they’re bad, and the fact that effectively no journalist bothers to include this in their writeups of their earnings from the last few years is a disgrace to the profession that fails the general public.

The problem that hyperscalers face is that they can’t really stop spending on AI, because once they do so, they’ll suddenly start getting graded on their AI investments. As long as we’re in a “capex buildout phase” of indeterminate length with data centers that take two to three years to come online, Microsoft, Google, Microsoft, and Meta can perpetually kick the can by spending tens of billions of dollars on capex, or at least they’ve been allowed to because their current businesses have kept growing.

There’re a few problems with this approach:

As mentioned previously, the payoff here would have to be in the trillions of dollars of new revenue, in a way that was virtually impossible to deny. Incremental revenue growth or improvement of current profit lines are insufficient justification of the current spend, let alone the future trillion-plus (and yet-to-be-unannounced) in capex or the trillion-plus in ongoing commitments.

What could possibly make any of this worth it? None of the hyperscalers have created a single new product line or service that actually matters, nor do they have any unique IP or technology that could turn into one.

AI boosters and paint-eaters continue to claim that the growth we’re seeing now is from investments in AI, but if that’s the case, that means that the current hyperscaler business lines are in such severe decline that they basically stopped growing in 2022, which is most assuredly not the case.

Sidenote: That being said, I do have one revelation for you: based on my reporting on OpenAI’s audited financials, we know that OpenAI spent $17.2 billion on Microsoft Azure in a calendar year where Microsoft had $120.4 billion in revenue in the Intelligent Cloud segment, growing 26% year-over-year (from $95.5 billion in CY2024).

This means that OpenAI’s revenue represents 69% of Microsoft’s year-over-year cloud growth for calendar year 2025, and without it, Intelligent Cloud would’ve only grown 8% year-over-year.

That’s pretty fucking bad!

And please, spare me your warbling about whatever “ad growth” you think Meta is getting from AI. This is the metaverse all over again, except larger, more annoying, and more dangerous to its balance sheet. The fact that we are even debating whether AI is helping these companies and that nobody can just show me the actual numbers to prove me wrong are the signs that something is very, very wrong in a way that’s unlikely to change.

It’s also unlikely to change with another trillion dollars’ worth of capital expenditures.

More capex means more space for Anthropic and OpenAI to spend their venture capital funds on Azure, AWS, and Google Cloud. Even if margins were to remain stable and both AI labs stay alive for the next five years, the revenue growth would still be overshadowed by capital expenditures that represent 100%, 118% and 181% of cloud revenues as of their last quarters.

It don’t take no math genius to say that this does not seem to be working out in a way that makes more dollars than it costs, and I can find no compelling evidence that another three years of data center construction magically turns this all on its head.

Yet the moment they stop spending capex (by which I mean dropping it significantly — below $15 billion, I’d say), the AI bubble pops. Any capital expenditure pullback will be an impossible-to-ignore sign that what they’ve built is sufficient, which will get hyperscalers a short-term stock bump before facing three much-uglier questions:

And there’re really no compelling answers, because, as I discussed in the Rot-Com Bubble, we haven’t had a new Google Search, iPhone, or Microsoft 365 in decades, and without one, hyperscalers don’t have a hypergrowth future.

Their only hope would be if AI itself becomes far more than it currently is, and yes, that includes Anthropic and OpenAI.

People are going to be very mad at me for saying this, but when you strip away the media hype and the investment rounds, the actual things that generative AI can do are, at best, kind of cool and for the most part awkward and mediocre.

The ability to generate code in a mindless and expensive way that sometimes works and may or may not make developers an indeterminate level of more-productive is not a business model, a point made more obvious by the fact that Anthropic and OpenAI allow users to burn $8000 to $14,000 a month for $200.

I know somebody is going to read this and oink that “they have 70% gross margins” or some such bullshit, but none of you have any proof other than something your dad’s friend’s dog’s aunt’s proctologist’s friend heard in a Discord chatroom. However “useful” AI coding tools may be — and it’s genuinely hard to tell! — is immaterial to the larger point that they’re very, very, very expensive to use, that most of those costs are either hidden from the user or subsidized by employers, and that despite all the fucking noise, they are yet to substantively replace or even enhance human beings outside of the loudest and most annoying people on Twitter.

And I think people genuinely underestimate how harmful the vacuousness of AI’s benefits has become.

Per Nik Suresh’s excellent “AI Mania Is Eviscerating Global Decision-Making”:

Unfortunately, we live in a dark timeline. All of the AI projects we have observed as a team are failing. Every single one – we have seen 0% success in a year and a half, not only amongst projects we have been asked to participate in, but even within projects that we have observed in passing while doing totally unrelated work. Even if you grant that AI tooling accelerates specific workloads, the method and scale of the current investments is senseless. Frequently the failure is not related to AI itself, but rather that companies are terminally bad at running software projects effectively, and as I have remarked previously, AI projects are subject to all the failure modes of normal projects plus you can get everything right and then still fail because of the method's novelty. Very few companies are so good at shipping software that they can afford the extra risk profile.

Suresh, a decorated consultant and software engineer who wrote one of the best pieces on AI of all time, tells the story of an economy dominated by people buying and selling AI for symbolic reasons entirely disconnected from actual productivity, with in some cases one’s sufficient devotion to using or supporting AI’s (imaginary) productivity benefits being essential to surviving in many modern businesses.

In every sufficiently large business we have observed (say, with 500+ employees), we have noted that continued advancement, and increasingly continued employment, has started to require repeated professions of belief in the transformative power of AI for said business. I am not talking about providing ideas about how to use AI in the business – I mean religious profession, declarations of faith. Overwhelmingly these statements are made by non-technicians, though it is not uncommon for technicians to emit deranged statements to curry favour.

There have been several occasions where I have seen someone, apropos of nothing, blurt out almost word-for-word “AI is changing everything”, only to concede moments later that their organisation does not currently use LLMs for anything, and indeed, that they cannot name a single thing that has changed other than they get some use out of ChatGPT (frequently the free-tier). In one extreme case, I have seen an executive confess that they had never even used ChatGPT or any AI tool in their life, immediately after producing a technical strategy for an organisation with $2B+ in revenue which was entirely centered around AI.

This is an alarming situation caused by a few things:

Suresh’s piece is both fantastic and vile, telling the story of people “AI-washing” their work, “...meaning that even when they can perfectly competently execute on their jobs to the satisfaction of their management teams, said managers are unhappy if [they didn’t use AI],” of organizations firing top performers because they achieved said performance without using AI, of a global intelligence crisis where executives lie and say they love AI and are 100x more productive with AI because if they don’t, their customers and their customers’ customers will be offended.

LLMs are capable of doing a convincing-enough demo of functional-adjacent software that they can convince basically any CEO that they can do basically anything. As I wrote in Revenge of the Business Idiot, the media and the markets are so used to coddling and celebrating the dull, brainless and mediocre executive class that it was inevitable a technology would grow not based on its actual efficacies but what it represented to the managerial sect, and what it could represent to their stupid friends.

The problem is that there’s only so far you can take something based on everybody pretending it’s magical or its convenience as a symbol of executive power. Outside of coding, AI really has no fundamental use cases beyond being slightly better at interpreting search queries, brainstorming, and searching documents.

Sidenote: The only truly useful use case I’ve found is on the Bloomberg Terminal’s ASKB feature, which takes natural language and turns it into BQL code to make requests of Bloomberg’s datasets. It’s genuinely useful! It’s also something I imagine that could be done with any number of different LLMs.

No amount of anecdotal “I used it for this one thing and it was useful” changes the amount of money that AI requires to exist, plugs the gaping holes in Anthropic and OpenAI’s cashflows, or fixes any of the economic problems with data centers I’ve already discussed.

LLMs are economically and practically unsuited to the tasks they’ve promised to solve, and no amount of extra capital expenditures or venture capital dollars will magically fix that.

If you think that’s an outlandish take, one that only a “hater” or “AI doomer” could make, allow me to refer you to this note from ratings agency Fitch, which warned that a lot of debt is going to AI capex, and the usefulness of AI (and, by extension, that capex) remains a big hanging question mark, which presents a massive risk to lenders, and by extension, the global economy:

The scale of the AI investment boom and the accelerated global technology cycle has been a significant driver of US equity market valuations and corporate bond issuance over the past year. The effects on real economic indicators are profound. The 18% yoy rise in IT capital investment directly added 1.4pp to 1Q26 GDP growth. The wealth effect from AI-related investor optimism and equity market gains has also been a meaningful support for US consumer spending growth, which has been broadly slowing.

That said, the medium- and long-term potential of the underlying technology is highly uncertain, as with previous tech cycles. The combination of revenue uncertainty and the extent to which capital markets and economies have become intertwined with AI have created a vulnerability for credit in the event of a re-evaluation of long-run returns potential. Very short-term spikes in market volatility for individual equities and tech-heavy stock indices have already occurred, but a larger, more protracted correction could have wider market, macro and credit effects depending on its scale, duration and contagion.

Anyway, I want you to imagine you wake up tomorrow, and nobody is talking about AI in the news. AI-related stocks aren’t dominating the market. Nobody on Twitter is discussing AI. Nobody you know or talk to is talking about AI. Nobody you know is using it, nobody you know has even heard of it.

Would you still be as excited? Would you feel the pressure to use it? Would any of this make any sense if there wasn’t someone threatening your job or scaring you in the media every day? Would any of this seem rational?

AI, as it stands, is an exercise in kayfabe — a thing people are taking seriously because the rich and powerful are saying they have to and a media ecosystem built to celebrate them says that you need to.

And the fundamental issue, to paraphrase Roger McNamee on CNBC, is that they’re trying to make a niche tool a general-purpose technology.

The trillion-plus dollars in capex and venture investment is an attempt to turn Large Language Models that generate and summarize things into something that can do anything, because the people at the top of both the organizations building and buying AI services don’t actually do real jobs and thus can’t understand that the vast majority of tasks are neither generative nor replaceable with a median version of their outputs.

Every layer of GPU (and CPU) intensive agentic bullshit is a tacit admission that LLMs are not a tool with any of the features of “artificial intelligence” anyone has dreamed of. Their greatest innovation is their symbolic ability to scare and compel people to change who they are or how they treat others as a patronage to the tech industry, or a general fealty to the powerful.

And I fear everything will end in tears, all because those with the responsibility to tell the truth or stand in the way of grifters both opened the doors and sung their praises, attacking and othering skeptics who wanted to avoid what I fear is now an inevitably painful future.

If you liked this piece, you should subscribe to my premium newsletter. It’s $70 a year, or $7 a month, and in return you get a weekly newsletter that’s usually anywhere from 10,000 to 18,000 words, including vast, detailed analyses of the biggest events and companies in the AI bubble.

2026-07-25 00:56:52

Good morning premium subscribers! As ever, please ping me at [email protected] if you have any questions.

Oracle has one of the strongest mythologies in the tech industry. Ask a regular person and they’ll tell you that it’s “incredibly profitable” and “growing fast,” that it’s “unstoppable,” and that Larry Ellison has the mandate of heaven with regard to the continual sales of software and hardware related to databases and AI.

And those people are completely and utterly wrong.

The original title of this article was “Is Oracle Dying?” because I assume, when I took a deeper look, that there’d be some sort of debate, some sort of bull case for a decades-old quasi-hyperscaler run by one of the more nakedly-evil CEOs in the history of tech. I assumed — incorrectly, I might add — that Oracle as a business was doing fine other than the ridiculous commitments it made to support the whims of Sam Altman and OpenAI via deals that I believed (and still believe) will kill Oracle.

Except it turns out that Oracle has already been on a death spiral for the best part of a decade (if not longer) and has only survived this long by screwing its customers, taking on masses of debt, and — most importantly — more than $85 billion in acquisitions over the last 23 years. Pretty much every major product line outside of databases is a hodge-podge of other people’s innovation stapled together with a legendary contempt for the customer. These acquisitions (and continual price increases) are the only thing keeping the reaper from Oracle’s door other than margin-destroying GPUs.

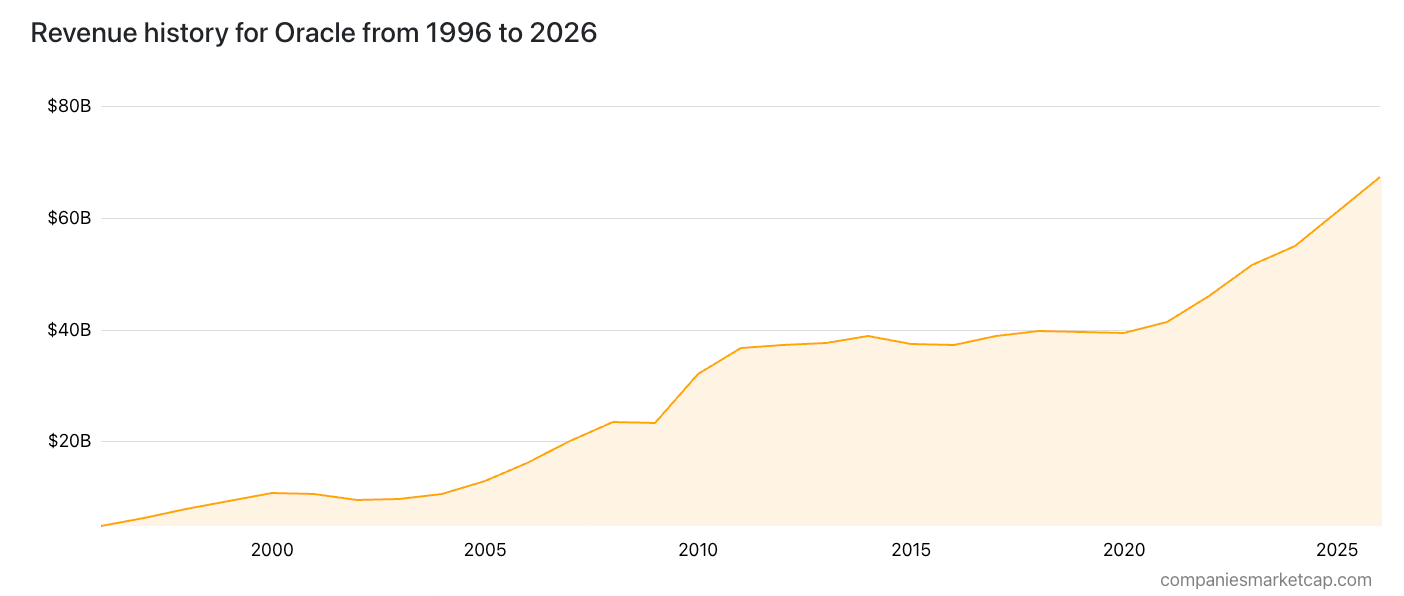

And that’s why Oracle’s revenue looks like this:

After April 2009’s $5.7 billion acquisition of Sun Microsystems, Oracle’s revenues barely kept pace with inflation until December 2021’s $28.3 billion acquisition of Cerner allowed it to create Oracle Health, adding about $6 billion in annual revenue that had 40% lower margins (about 21.7%) than Oracle’s other businesses, though Oracle immediately started closing offices and brutal layoffs to try and bring them up.

And as I mentioned above, Oracle’s other plan was to sink a little over $99 billion in capital expenditures since the middle of calendar year 2020 into AI GPUs.

Anyway, let’s see what that’s done to margins-OH MY GOD!

Oracle is a decades-long mission to keep reapplying lipstick to a pig. Billions of dollars of acquisitions have, for the most part, only succeeded in keeping the company’s revenue growth from going negative, and as noted by forensic accountant Howard M. Schilit, this is one of the most well-documented cases of accounting shenanigans being used to cover up that a business is in decline.

Today’s newsletter is a sequel to the Hater’s Guide To Oracle, where I told the sordid tale of how Larry Ellison grew a massive, lucrative business out of a database business that one reporter once told me was a “law firm with a database company attached,” an Enterprise Resource Planning (ERP) product that competes with SAP to create the most-annoying way to run a large company, and a business built around licensing Java that exists mostly to email people and say “you need to pay us for Java or we’ll sue you.”

Then, as I’ve mentioned, there’s Oracle’s cloud infrastructure business, a decade-old also-ran that was meant to compete with Microsoft Azure and Amazon Web Services, but only managed to catch up following the advent of AI GPUs and a movement where all it took to party was buying billions of GPUs and saying “gosh darn, we love AI.”

I originally started drafting this as a much tamer piece where I’d ask whether Oracle was dying, but as my editor and I started digging into the research, it became obvious that not only is Oracle dying, it’s been dying for years, kept alive through decades of acquisitions and a desperate and dangerous commitment to generative AI.

And AI, I believe, will be what eventually kills Oracle dead.

In the past, all Oracle had to do to survive was buy somebody else’s company and replace its flagging revenues with theirs, turning the screws on their customers and laying off as many people as necessary to balance the books. While chaotic and decaying, Oracle’s empire has kept above water by never overextending itself, always keeping a positive free cashflow, and generally avoiding buying into industry hype cycles outside of whatever SaaS vehicle might potentially plug the gap in its earnings.

Yet with AI, Oracle broke its long-standing trend of letting someone else figure out the innovation, choosing instead to build its own cloud infrastructure, spending more in capex in its last fiscal year ($55.6 billion) than it did in the previous nine years combined ($50.4 billion), tripling its debt from $56.91 billion in FY2017 to $167.4 billion in FY2026, a year that ended with its free cashflow sitting at negative $23.69 billion.

For comparison, Oracle has had positive free cashflow every single year since 2001, including the Great Financial Crisis and COVID.

Oracle has doomed itself with its commitment to the AI bubble. It has committed to building 7.1GW of data center capacity for one company — OpenAI — as part of a $300 billion, five-year-long contract that requires it to build an impossible amount of capacity in an impossible period of time for a client that could never afford the $70 billion or more in annual costs to make any of it worth it.

Today I am going to talk trash on what I consider to be one of the single-worst companies in the tech industry that’s survived only through financial engineering and never, ever overextending itself.

With revenue plateauing and customers in revolt, Oracle’s future already looked murky, but with the power of AI — and $95 billion in FY2027 capex — it’s becoming increasingly clear that this may be Larry Ellison’s last dance with Silicon Valley.

This is the Hater’s Guide To Oracle Part 2, or AIpoaclypse Now.

2026-07-23 00:08:51

Thanks for reading this week’s free Where’s Your Ed At newsletter. Friday’s premium newsletter will ask the simple question: Is Oracle dying?

It’s been one year since I launched the premium newsletter, and I’ve decided to extend the discount on annual subscriptions. Between now and 12AM ET, July 26, you can get a permanent annual rate of just $60— a $10 discount on the usual price of $70 — for life. Click here for the offer.

In addition to getting access to the entire back catalog of premium posts, you’ll also receive one additional post each week — usually anywhere between 10,000 and 20,000 words — covering the most pressing topics in the AI bubble — the best value in tech analysis. Highlights include the Hater's Guide To The Memory Crisis, a guide to how AI made everything more expensive, How OpenAI Kills Oracle (which pairs nicely with the Hater's Guide To Oracle), The Hater's Guide To NVIDIA, The Hater's Guides To Private Credit and Private Equity, and how the entire AI Compute Demand Story Is A Lie.

Soundtrack: Dillinger Escape Plan — Black Bubblegum (2007)

In The Big Short, Mark Baum shook with anger as a CDO manager told him that the market for insuring mortgage bonds was about 20 times larger than the mortgage bond market, realizing in real-time that speculation driven by greed and hype had set up a massive systemic weakness under everybody’s noses.

To get specific, Baum (played by Steve Carell) is giving a short, dramatic summary of a much greater problem — that there were trillions of dollars of synthetic collateralized debt obligations (effectively bets on whether somebody else’s bucket of mortgages (well, mortgage bonds) will actually pay up) that allowed multiple people to bet on the same mortgages again and again, meaning that once said mortgages went belly-up, the carnage would be widespread and hard to contain.

This became even more chaotic when it became clear that the same mortgage bonds were attached to many different CDOs — one study found that 5500 different mortgage bonds had been placed or referenced in CDOs over 36,000 times. A mortgage bond (or mortgage-backed security) is a slice of a pool of payments from thousands of mortgages, with each slice sold off to different buyers at different levels of seniority, the most-senior ones getting paid first and taking losses last.

In the end, the only thing you really need to know is that financial institutions built CDOs that threw together bonds in ever-more complex and dangerous ways, selling synthetic CDOs to bet on the outcomes, with different CDOs having different bonds covering the same pools of mortgages — bonds that were routinely rated by agencies at a higher grade than they should’ve been. When IMF Chief Economist Raghuram Rajan attempted to warn the financial services industry at the Kansas City Fed’s 2005 Jackson Hole symposium about the instability of the system, former US Treasury Secretary (and close friend of Jeffrey Epstein) Larry Summers referred to his concerns as “misguided.”

Meanwhile, the industry was handing out awards. On July 1, 2005 Lehman Brothers would receive one of Euromoney’s “Awards For Excellence,” where it was named the “Credits Derivatives House Of The Year.” Euromoney also referred to Lehman, a financial institution that was leveraged 25.3x in 2005, as “one of the more conservative credit derivatives houses.” It added that the company, which routinely overvalued its CDOs, was being able to take on the heavy burden of synthetic CDOs because it “...understands the arbitrage-driven economics of cash CDOs, the way that loan deliverable credit default swaps track the loan markets, how high-yield CDS trade (like bonds), and so on.”

Three years later on January 1, 2008 — nine-and-a-half months before its collapse — Risk Magazine would name Lehman Brothers’ “Point” risk management system as its “In-House System of the Year,” saying it “...stood out for the breadth of its coverage and depth and quality of its functionality.”

All of this started because of a flood of overseas money in the early 2000s buying up U.S. Treasuries as a result of a “global savings glut” — a fancy way of saying that there was too much money floating around — pushing yields down, leaving investors with far fewer places to get those all-important yields.

Low interest rates in the early 2000s (a direct response to the collapse of the dot com bubble) dropped mortgage rates to “generationally low” levels, and financial institutions realized they had an opportunity, as government policies had allowed them to loosen underwriting standards at exactly the time that foreign investors were desperate for places to park their money — mortgage-backed securities, and their associated derivatives. More mortgages meant more mortgage-backed securities, so banks made it incredibly easy to get a mortgage, to the point that in 2006, 20% of all new mortgages were subprime.

You’re probably wondering why nobody feared they’d get burned by this endless stack of different interconnected debts, and that’s because they’d “spread all that risk out” across credit default swaps with insurers, not realizing that insurers could and would become insolvent if everybody tried to make a claim at once.

This was all avoidable, and there were many warnings, and just as many people lining up to protect the grift. In June 2005, Larry Kudlow would say that housing bears were “wrong again,” dismissing those concerned with increasing default rates as “bubbleheads” that “don’t do their homework.” In September 2006, financier Michael Milken would refer to CDOs in the Wall Street Journal as a “financial innovation” that “helped to spread risk and create tens of millions of jobs by freeing up investment capital for growing businesses,” saying that they would “increase prosperity by multiplying the value of human capital, social capital and real assets.”

In other words, the argument was that the “financial innovation” of ever-expanding financial speculation was good for the economy because it created more money out of thin air, with the “risk” spread out somewhere, in a way that you shouldn’t think about because everything is going to be fine. Everybody would keep building houses forever, the numbers would only ever keep increasing, every new house would add a new mortgage to a new mortgage-backed security, and the line would only ever go up.

To put it all very simply, the great financial crisis was caused by inflated demand for housing caused by a mixture of historically-low interest rates and banks incentivizing bad habits as a means of increasing the value of speculative assets. In the end, “mortgage-backed securities” stopped existing as ways to invest in large swaths of mortgage payments, and more as high-risk financial vehicles that promised to be an infinite money glitch where nobody could lose because there would always be more demand for mortgages and, by extension, collateralized debt obligations made up of mortgage-backed securities.

It all broke because eventually those speculative assets had to interact with the real world, by which I mean mortgage defaults began to spike starting in 2005 with the expiration of teaser rates and multiple fed rate hikes throughout 2006 making adjustable-rate mortgages creep upwards. As mortgages collapsed, CDOs — and their connected synthetic CDOs — collapsed with them, crushed by the weight of the consequences of offering so many people so many mortgages under volatile and unrealistic terms, and assuming that nothing bad would ever happen because nothing bad had happened yet.

And, fundamentally, the great financial crisis was caused by massive speculation based on demand that was, in and of itself, an illusion created by the financial institution itself to justify further investment.

Say, that kinda reminds me of something!

I realize that the comparison between an AI data center and a CDO might seem a little ridiculous, but they’re actually remarkably similar. I’m going to generalize here, because each of these deals has weird little unique terms that make them, well, more dangerous.

Put simply, every time somebody builds a data center, they form a completely separate entity that owns the chips, owns the debt, and, in many cases, owns most of the risk. These SPVs only pay out to their creditors in the event that customer revenue flows in, which means that they are dependent both on the speed of construction of said data centers and their customers’ ability to pay.

CoreWeave is the main offender in the SPV no IT loads refused cash-dump, with a different SPV for each of its Direct Draw Term Loans (DDTLs), most of them non-recourse, meaning that if their customers fail to pay, investors get screwed to varying degrees based on their seniority in the debt, and CoreWeave’s assets can’t be pursued in court, though it is on the hook for the payments on the debt.

For example, CoreWeave’s $8.5 billion DDTL 4.0 loan was raised using its contract with Meta and the underlying data center assets as collateral with funding coming from banks like MUFG, Deutsche Bank, and US Bank, with funds being deposited into an SPV called CoreWeave Compute Acquisition Co VIII LLC, with another filing showing that the funding would be used to lease space from Applied Digital in Ellendale, North Dakota and fill it full of GPUs and provided to an “investment-grade customer” that Wells Fargo believes is Meta.

Similarly, CoreWeave raised its $2.6 billion DDTL 3.0 loan last year to “accelerate delivery of services from OpenAI,” funding two different SPVs called CoreWeave Compute Acquisition Co. V and VII, LLC. that, in turn, signed a deal to provide compute to OpenAI through the main CoreWeave entity. The deal also features a “cash trap” that means that if either CoreWeave screws up (IE: doesn’t deliver the compute) and OpenAI can quit or OpenAI doesn’t pay for three months, the SPV stops feeding any money to CoreWeave until the situation is cured, and if OpenAI (or someone else) doesn’t start paying, things start to break, as the deal has a contract realization ratio of .85x,.

To be clear, “non-recourse” does not mean “CoreWeave gets off scot free if these SPVs collapse,” just that creditors can jump on the SPV’s assets first and cannot immediately go after CoreWeave’s assets, though because each of these deals is guaranteed by the parent company (CoreWeave itself), it will eventually be forced to make them whole.

You can probably guess how that goes badly.

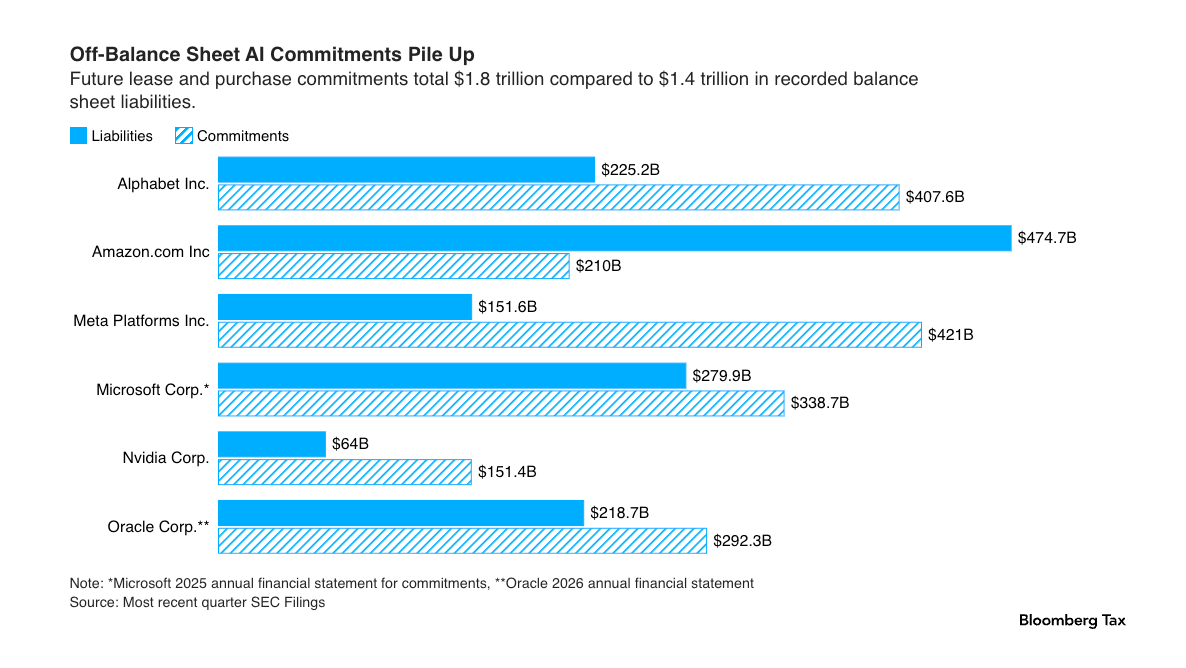

The nature of these SPVs makes it difficult to quantify the exact scale of data center debt, but Bloomberg estimates that there’s over $500 billion in outstanding AI data center debt, with (per Garima Kapoor of Elara Securities Research) at least $200 billion of it held by private credit, making up roughly 8% of outstanding private credit loans.

That being said, the number is likely much higher. Nikkei Asia reported this week that Meta, Google, Amazon, Microsoft and Oracle have accrued around $1.65 trillion in outstanding debt in the last five years, with an additional hundreds of billions of dollars’ worth of “off balance sheet” debt, meaning that the corporate structure allows the company to not include it as part of its liabilities.

For example, BlackRock is currently raising $12 billion to build a data center for Meta, which in practical terms means BlackRock has invested in and is raising debt for a holding company called “Project Sopaipilla Holdings,” of which it owns 80% and Meta owns 20%. This holding company will then buy NVIDIA GPUs and pay construction firms to build the data center, and Meta’s (theoretical) payments will be used to pay down the debt.

Despite the fact that Meta will (theoretically) own and operate as the exclusive tenant of this data center, the actual debt — $12 billion or more! — won’t appear on its balance sheet, much like its $27 billion Hyperion Data Center that belongs to an SPV called Beignet Investor LLC which is 80% owned by Blue Owl, 20% owned by Meta, and funded using bond sales to PIMCO and BlackRock.

The problem with these SPV-based deals is that they allow companies to, at least on a balance sheet basis, hide the scale of their debts. Meta’s long term debt sits, as of its latest quarter, at around $58.7 billion. It’s as if the $39 billion in debt for gigawatts’ worth of AI data centers doesn’t exist out of the payments it’ll eventually have to make.

This is all legal, worrying, and yes, a little bit Enron.

Per Amanda Iacone of Bloomberg:

Enron Corp. exploited US accounting rules to hide from investors and lenders hundreds of millions in debt it had bundled into off-balance sheet entities — obligations that contributed to one of the biggest corporate collapses in US history.

Alphabet Inc. and Meta Platforms Inc. each have turned to vehicles known as variable interest entities (VIEs) as part of the financing mix needed to construct data centers and related energy infrastructure.

Meta, the parent of Facebook, last year formed a joint venture, a VIE, to build a Louisiana data center through a partnership with Blue Owl Capital. The social media titan’s maximum exposure for the venture is $46 billion, according to its filings with the Securities and Exchange Commission. The company announced last week that it would expand its planned campus and is expected to spend as much as $250 billion on the project, Bloomberg News has reported.

To be clear, a Variable Interest Entity is a type of SPV where you have control over the entity, and you must consolidate it into your balance sheet…unless you are not considered the “primary beneficiary,” which Meta argues isn’t the case despite being the primary tenant and reason that Hyperion is being built. Per Bloomberg:

Meta determined it shouldn’t bring billions in debt from the Louisiana project onto its own balance sheet because it isn’t responsible for finding tenants to replace or join it at the nearly 4,000-acre campus — a critical job that impacts the entity’s economic performance, the social media company said in its most recent quarterly SEC filing. Meta said its role is limited to construction management, along with administrative and property management services.

Auditor Ernst & Young raised a “red flag” (per the WSJ) about this arrangement, flagging it as a “critical audit matter,” adding that it “...was especially challenging due to the significant judgment required in determining the activities that most significantly affect the VIE’s economic performance.” Nevertheless, it was approved, it happened, and everything is fine and normal.

This is why Google backstopped Fluidstack and Cipher Mining’s 300MW data center and another for TeraWulf. Both will, eventually, operate as data centers that Google will lease to provide compute to Anthropic, booking revenue for doing so, acting as the sole tenant and the entire reason that the debt was raised, yet because Fluidstack and TeraWulf and Cipher Mining are the actual entities involved, nothing shows up on Google’s balance sheet.

What’s also important to note is that none of the money going into these SPVs counts as capital expenditures. For example, across the space of five quarters (Q1 2025 through Q1 2026), Meta spent around $88.6 billion in capital expenditures, but that doesn’t include any of the debt or purchases of GPUs or anything else done in its name as part of the Hyperion SPV, despite it having (per its own fillings) $45.95 billion of exposure.

To be clear, even “on balance sheet” obligations are off-balance-sheet until the leases begin. Bloomberg has a truly horrifying chart that illustrates its scale:

Much like the Great Financial Crisis, nobody has seen any of these data center SPVs (or the greater data center bubble) as a problem yet because

I want to be very blunt about something: we do not, at this point, have a firm hand on exactly how much demand there is for AI compute, and evidence suggests that it’s much, much smaller than we’ve been led to believe.

I estimate that 70% or more of Microsoft, Google and Amazon’s compute capacity is taken up by OpenAI and Anthropic, and in my analysis of non-hyperscale compute providers, I struggled to find any customer other than them that was spending more than $50 million a year on compute.

That’s because real, diverse demand does not exist for AI compute, as evidenced by the fact that the same four or five companies are the only ones interested in renting it at scale.

Sidenote: Furthermore, any demand for compute that exists currently is inflated by the effective subsidization of paying subscribers to ChatGPT and Claude, who can burn tens of thousands of dollars worth of tokens while only paying $200-a-month.

For example, on July 1, Bloomberg reported that Meta (mere months after Zuckerberg said that “selling capacity was on the table if it overbuilt”) was creating a cloud business to rent out its AI GPU capacity. A mere two weeks later, the New York Times reported that it was in talks to rent capacity to Anthropic.

While one might argue that Meta is taking advantage of a wealthy buyer, one has to ask: if there was such insatiable demand for compute, why wouldn’t it want to sell it to a diverse set of customers who would likely pay a much higher rate than a years-long contract?

It’s because those customers do not exist at a scale that would actually make it worthwhile! If they did, we’d see massive bursts of remaining performance obligations from neoclouds like Nebius, IREN and CoreWeave that were unrelated to new contracts they’ve signed with either hyperscalers, OpenAI or Anthropic. Companies like Lightning, Runpod, and Lambda would have billions in revenue. Instead, Runpod has $120 million in ARR, $500 million in ‘annualized’ revenue, and Lambda had $114 million in revenue as of the second quarter of 2025, with a little less than half of that coming from Microsoft and Amazon.

While the counter-argument is that these companies are all GPU-constrained, and that demand is simply waiting in the wings…except surely that would mean that these companies also had massive remaining performance obligations?

To be clear, the point I’m making is not that there’s no demand, just that the vast majority of that demand is coming from either Anthropic and OpenAI — two companies that cannot afford to pay for it long-term — and hyperscalers, who are mostly buying compute on behalf of OpenAI and Anthropic.

And I’m not sure that people are taking me seriously when I say that AI compute demand does not exist at the scale that it needs to, will likely never reach that scale, and data center construction is a debt-funded asset bubble with ruinous consequences.

So, let’s set some table stakes.

Per my own analysis, NVIDIA’s predicted $1 trillion in Blackwell and Vera Rubin GPU sales (by the end of 2027) represents around 40GW of data center capacity, which will, assuming a PUE of 1.35, result in around 30GW of usable capacity. At a cost of around $12 million a megawatt, that works out to around $435 billion in global annual compute revenue to make these data centers necessary.

Right now, there appears to be roughly $100 billion or so in annual compute spend, with OpenAI representing around $50 billion (per their statements in the Musk trial), and Anthropic likely spending similar amounts. Microsoft and NVIDIA represent a combined 65% of CoreWeave’s $2.08 billion in (latest) quarterly revenue, with the rest likely taken up by OpenAI. IREN, another neocloud, recently announced it was targeting a year-end cloud ARR of “over $4 billion,” or around $333 million a month, with a customer base that includes, unsurprisingly, Microsoft and NVIDIA, as well as companies like Perplexity, Figure AI, and Together AI that are unlikely to be spending more than $50 million apiece given their funding status and revenues.

Sidenote: It’s important to note that spend isn’t necessarily the same as utilization. Much of the compute spend comes in the form of long-term contracts, where the price-per-hour for a GPU is (naturally) lower than it would be if it was rented to deal with a momentary spike in utilization. The vast majority of AI compute spend comes in the form of these long-term contracts.

Another concerning anti-demand signal is the fact that NVIDIA has committed to $30 billion in multi-year cloud compute agreements, spending $6 billion or more a year through 2028 to rent back its GPUs, including a $6.3 billion backstop for CoreWeave that explicitly states that NVIDIA is “is obligated to purchase the residual unsold capacity” through April 2032, suggesting that there would be residual capacity that had gone unsold to the tune of billions of dollars.

Oh, and NVIDIA owns 9.3% of Nebius too. It’s also invested in IREN, CoreWeave and has both invested in and rented capacity from Lambda.

If you’re wondering why these deals keep getting signed — as mentioned previously — it’s because a financial guarantee from NVIDIA is sufficient collateral for a bank to lend money to these companies to buy more GPUs.

I imagine a conversation in the Big Short 2 might go a little like this scene.

HUANG: So there’re these companies I invest in that, at least in theory, build data centers using my AI GPUs, but I need them to buy more GPUs, so I sign a contract saying that I’ll rent the GPUs back from them in the future. Because NVIDIA has such a strong balance sheet, these companies can raise billions of dollars to buy my GPUs just because I promised to rent them in the future, and the best part is all the risk is held by the companies and the investors. When I need more money, I just sign another contract, they raise more debt, I sell more GPUs.

BAUM: So — just so I have this clearly — you, the guy who makes the GPUs, invest in companies that exist pretty much to buy GPUs from you and rent them to customers. Except you’re the customer too, and a big one.

HUANG: That’s right. We call them neoclouds. S&P just revised CoreWeave’s outlook to positive.

BAUM: That’s fucking crazy.

HUANG: It’s not crazy — it’s awesome.

Those Meta and Microsoft neocloud deals exist explicitly to lower their capex and debt — by which I mean that if Nebius or IREN takes on the billions in debt to buy all of those GPUs, Microsoft and Meta only have to worry about the ongoing leases, assuming that construction is ever complete. These deals also regularly include a clause that allows them to be terminated in the event that delivery milestones are not met, as is the case with Microsoft’s $17.4 billion deal with Nebius.

This means that hyperscalers take on effectively no risk, and investors are left holding the bag. For example, Nebius’ recent $775 million debt facility is “backed by contracted cashflows and deployed GPU infrastructure,” meaning that if things fall apart, the only entity that can be sued would be a company that explicitly exists to buy NVIDIA GPUs and rent them.

To be abundantly clear, the vast majority of the AI data center compute revenue is contingent on the continued ability of two unprofitable, unsustainable AI companies’ to raise tens or hundreds of billions of dollars a year. This is not an overstatement, this is not hyperbole, it is the quite literal situation we’re stuck in.

Putting aside whether data centers are profitable or not (they aren’t), if the demand does not exist at this remarkable scale, the vast majority of AI data centers and their associated SPVs will collapse.