2026-07-30 21:52:00

🎙️ Listen on Spotify, Apple, or wherever you get your podcasts.

Jacob Hodes is a partner and Chief Investment Officer of Private Investing at Brown Advisory, the Baltimore firm descended from Alex. Brown & Sons — the first investment bank in the United States. He got there by way of Goldman Sachs, law school, and Skadden, a path he describes as meandering.

In this conversation, he explains why he’s both the loudest advocate for private markets at his firm and increasingly nervous about where they’re headed, what a post-industrial city does to an investor’s judgment, and why the junior people who rise fastest are rarely the ones with the best pedigree.

“You think you do, but committing yourself for 10 years is really tough. … If half of all marriages end in divorce, that’s usually within 10 years. You probably feel much more strongly about getting married than you do about making an investment.”

Private markets were built on information asymmetry: A century ago the Rockefellers and Carnegies could make private bets because their operating businesses gave them a data set nobody else had. That edge migrated to institutions with the balance sheets to go long — and the fund structures followed.

Illiquidity is underestimated by everyone who hasn’t lived it: A ten-year commitment outlasts half of all marriages. As private vehicles push downmarket, Hodes expects investors to fall out of love with positions they can’t exit.

The asset-liability mismatch is the risk to watch: Semi-liquid vehicles wrap multi-year illiquid assets in structures promising something closer to daily liquidity. Smart people will eventually solve it; the road there will be bumpy.

Underdog geography sharpens judgment: Working from Baltimore rather than a coastal financial center means finding value where others don’t look — and holding onto discipline when you’re across the table from a high-flying founder.

Read newspapers from places you don’t live: Local papers from cities and countries outside your own break the echo chamber and show you how other people are actually seeing the same events.

00:00 - Introduction to the Guest and Firm

01:13 - A Meandering Path: Princeton, the Nasdaq, and Goldman Sachs

03:29 - Back to Basics: What Long-Term Investing Requires

05:22 - Why the Dot-Com Bust Was the Formative Crash

08:50 - Politics, Government, and the Limits of Prediction

12:13 - Baltimore as an Investing Lens

17:33 - What a Law Degree Teaches (and What It Doesn’t)

20:32 - The Junior People Who Rise Fastest

24:49 - The Armchair Psychologist Side of Client Work

27:10 - The Contrarian Take: Private Markets and the Retail Push

31:01 - How to Read: Local Papers from Places You Don’t Live

33:01 - Conclusion and Final Thoughts

2026-07-27 21:08:00

Nan Ransohoff (Head of Public Goods at Stripe) recently published a sharp piece on what she calls the third wave of American philanthropy: the tidal change coming as AI wealth becomes liquid and a generation of founders gives it away.

It’s a generous, clear-eyed essay about a real institutional mismatch: an enormous new pool of capital is forming, but the systems built to turn that capital into lasting public good have not caught up. Nan’s point is that the next generation of givers may need new vehicles, new norms, and new institutions to make that money matter.

I agree with all of it. But the piece also surfaced an adjacent question I keep coming back to:

What if the most important social institutions of the next 50 years aren’t nonprofits at all?

For most of modern philanthropy, the sequence was simple: build the company, make the fortune, then decide what the fortune should repair.

Andrew Carnegie endowed infrastructure for self-improvement after he built U.S. Steel. John D. Rockefeller funded medical research after he built Standard Oil. Both were unusually systematic for their era. Carnegie’s “Gospel of Wealth” (1889) argued that the rich had a duty to give in their lifetimes and to do so strategically — “The man who dies rich dies disgraced” — not through charity, which he openly disdained as wasteful, but through institutions that would endure (libraries, universities, museums, research).

Rockefeller went further on the operational side. He hired Frederick Gates (no relation to Bill) as essentially the first professional philanthropic strategist, and Gates ran the giving like a research operation: identify root causes, fund the underlying science, measure outcomes. The Rockefeller Foundation’s work on hookworm eradication in the American South and yellow fever globally was “outcomes-driven public health” decades before that was a phrase.

The pattern was straightforward: industry created enormous wealth and enormous externalities, and philanthropy emerged to repair what industry broke. Make money first. Give later. The two halves were kept on separate ledgers. You don’t have to squint too hard to see the seeds of Effective Altruism in this early philanthropy: earn as much as you can, then deploy it where the math says it matters most.

Squint a little harder and you can see the same shape in a much newer idea: that some of the largest companies in the world might hand shares directly to the next generation. It may be the most promising thing the two-ledger model has produced.

But the architecture never changed. The company is the instrument, the impact is the output, and the two only meet at the end.

I don’t think this new generation of founders sees it that way anymore.

The most ambitious founders building companies now draw no clean line between “what the company does” and “what the company is for.” They want the operating model itself to carry the values. If a company’s success requires people to be healthier, better educated, breathing cleaner air, or more financially secure, then every dollar of revenue is also a unit of the good it claims to want in the world. The two ledgers collapse into one.

The skeptical read is that “mission-driven companies” are a marketing pose — purpose-washing layered over a normal P&L. We see it all the time. A company discovers that virtue is good for customer acquisition, or that the language of impact helps it recruit, raise capital, or soften the edges of an otherwise conventional business. Anyone investing through this lens has to develop a pretty sensitive ear for the difference between mission as decoration and mission as design.

The strongest version of a mission-driven company is not one that donates a percentage of profits after the fact. It is one where the business can only get bigger if the stated mission becomes more true—even if aligned incentives have to be constructed against entrenched ones. A health company should thrive when people get well, not when they stay sick. A climate company should make money as emissions fall. A financial company should grow when customers build wealth, not when they fall into debt. In those cases, the social good is the unit economics.

You can see companies running this experiment right now. WHOOP only grows if their members actually sleep, recover, and live better (i.e. the subscription renews on results). Redwood Materials gets bigger as more batteries come back around instead of ending up in landfills. Base Power scales as the grid gets cleaner and more resilient. Etsy grows only as independent makers earn a living. Periodic Labs is making the wildest bet of all: that accelerating scientific discovery itself can be the business. The list should be much longer.

Call it the Villain Test, the Miracle on 34th St., the Warren Buffett See’s Candy manifesto. The strongest businesses don’t sell what they make; they sell what they mean. The companies most likely to matter in fifty years — the companies with lasting impact — will be the ones whose meaning is indistinguishable from their work.

Nan is right that we’re short of philanthropic startups and capital allocators, and that those gaps need to be filled fast. She is, in fact, doing just that—Stripe recently announced the Intercept Fund, a $500m philanthropic initiative to eradicate respiratory infections. They write: “There are many important products (public goods!) that would improve the world but don’t exist because the commercial motivations aren’t yet sufficient.” I couldn’t agree more, and I’m proud to serve as an Advisor to this initiative.

But not everything will look like philanthropy.

Some of the most important problems of the next 50 years — health, climate, civic trust, the cultural conditions of a good life — won’t be solved by foundations alone, or by nonprofits alone, or even mostly. They’ll be solved by companies that were never asked to choose between profit and progress in the first place.

This is not a claim that every problem has a market solution. Many do not. Some of the most important work in the world will always depend on gifts, public funding, religious institutions, universities, mutual aid, and nonprofits willing to serve people and problems no market will reward. If anything, that need is about to grow: as AI reshapes work faster than institutions can adapt, the safety nets markets don’t provide will matter even more.

But when a problem can be addressed by a company whose incentives are aligned with the outcome we want, that should count as part of the philanthropic imagination too — not a substitute for giving, but as a reminder that the check is not the only vehicle.

That’s the version of the third wave I’m most interested in: not just more wealth moving into philanthropy after the fact, but more founders refusing to separate the wealth from the good in the first place.

2026-06-23 21:42:00

Tristan Walker is joining Collaborative Fund as a Partner.

In that role, he’ll be a voice for the kind of company-building we stand for and a resource for the founders pursuing it. We’ve long believed that the best people to support founders are other founders, specifically those who have built enduring, values-driven companies through the full cycle of highs and lows. Tristan is a textbook example of that.

The relationship here goes back over a decade. I backed Tristan when he launched Walker & Company and watched up close as he built Bevel with incredible clarity and integrity. That journey eventually led to an acquisition by Procter & Gamble—proof that you can build a successful brand by serving communities the market overlooks.

Tristan’s experience isn’t limited to a single win. He was the third employee at Foursquare, an EIR at Andreessen Horowitz, and co-founded Code2040 to help diversify Silicon Valley. Today, he brings a wealth of governance and leadership experience from his board service at Shake Shack, Foot Locker, and Children’s Healthcare of Atlanta. And he’s still building: his latest venture, Heirloom, is working to reshore American fine craft, training the next generation of artisans and rebuilding the supply chains behind it.

At Collaborative, we look for builders rather than just allocators. Tristan’s track record as a founder and his deep roots in both business and civic life make him an invaluable partner for the founders we support.

We’re lucky to have him on the team.

2026-06-11 02:03:00

Why we misunderstand odds and why it matters

Why we misunderstand odds and why it matters

Everyone has a weakness. A blind spot. A vulnerability.

For Achilles, it was his heel. Superman had kryptonite. Ted Williams struggled with pitches low and away.

But what about the average person?

I often think our Achilles heel is our inability to understand probabilities. And increasingly, it’s making us more stressed than ever.

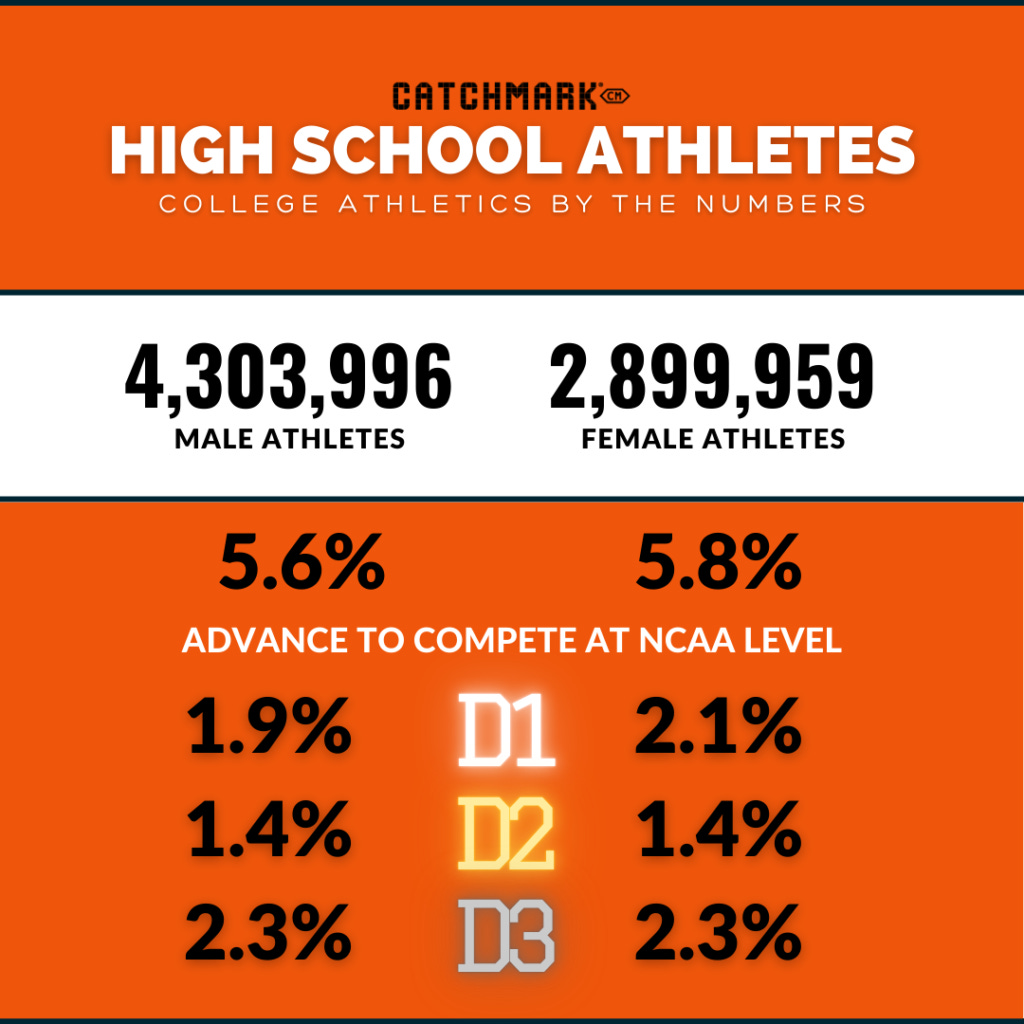

I was reminded of this recently after speaking with a young man who is navigating the college admissions process. He had been accepted to several very good universities, but not his first choice, which happens to accept fewer than 6% of applicants.

In an attempt to alleviate some of his angst, I asked him a simple question:

“How many high schools do you think there are in the United States?”

He guessed 12,000.

The actual number is closer to 25,000.

I then asked him how many valedictorians there are in the U.S.

He understood the point. Roughly one valedictorian at each high school, so 25,000 in total.

Considering that the Ivy League enrolls approximately 15,000 freshmen each year, in theory, 40% of all valedictorians don’t have a spot. Once you account for international students, even fewer do.

Yet every year, students and parents across the country are devastated by rejection letters from elite universities.

This phenomenon isn’t limited to college admissions. It shows up practically everywhere. Companies, marketers, and advertisers know it and often exploit it.

Youth travel programs charge thousands of dollars and promise pathways to scholarships and college admissions despite the long odds.

Sports franchises convince us to invest our hearts and wallets every season despite the tiny probability of winning a championship. (As a long-suffering Washington Commanders fan, I can personally attest to this.)

Investment managers pitch market-beating strategies despite the fact that most fail to outperform the S&P 500 over time.

Which reminds me of a story involving Charlie Munger.

Munger once asked an investment manager what annual returns he promised clients.

“Twenty percent,” the manager replied.

“Twenty percent annually is impossible,” Munger shot back.

The manager shrugged.

“Charlie, if I told them a lower number, they wouldn’t give me any money to invest.”

So what’s the solution? Should we all have paid closer attention during the probability chapter in high school math?

When I began writing this piece, I would have answered with an unequivocal yes.

Then something occurred to me.

Ironically, our greatest weakness may also be one of our greatest strengths.

After all, how else do you explain entrepreneurs starting companies in garages, explorers venturing into the unknown, or America’s Founding Fathers risking everything to declare independence from Great Britain?

Viewed purely through the lens of probability, many of humanity’s greatest achievements look irrational.

No rational calculation alone would have inspired those leaps.

Something else was required.

But what?

Passion.

And that leaves us with an interesting tension.

When should we trust the odds, and when should we challenge them?

When the pursuit matters as much as the outcome.

If you love learning, study hard. Chase your dream school. Take the APs and advanced classes. But if the acceptance letter never comes, your efforts will not have been in vain. The education you gain and continue building throughout your life will matter far more than the name at the top of your diploma.

If you pour countless hours into a sport you love, but never earn a scholarship, it won’t have been a waste. You will have experienced victory and defeat, learned what it means to be a good teammate, and chased a dream.

Your favorite team may never win a championship, but the memories of rooting for them will last a lifetime.

And if an investment you believed in fails, you will have learned a lesson every successful investor eventually does: even the best are wrong much of the time.

The key is understanding why you’re doing something.

If you’re chasing a dream because you genuinely love the pursuit, the odds matter less.

If you’re doing it solely for status, recognition, or some promised outcome, disappointment is almost inevitable.

My takeaway?

Understanding probabilities is essential for maintaining perspective in a world filled with unrealistic expectations and carefully curated success stories.

But if you find something you truly love, don’t let the odds become your Achilles heel.

Instead, understand the probabilities, then decide whether the dream is worth pursuing anyway. And when others choose to chase theirs, root for them too.

After all, many of humanity’s greatest achievements began with someone willing to pursue a dream despite the odds.

2026-05-20 03:35:00

What defines Collab Holdings future success isn’t the capital; it’s the stewardship.

Few investors understand both the rigor of private equity and the nuance of what makes a brand actually matter to people. Parker Hayden does, and he is joining Collaborative Fund as a Partner to lead Collab Holdings.

Collab Holdings exists to be a home for enduring companies, and Parker is the right person to lead that work.

Over more than two decades, Parker has deployed over $3 billion across dozens of transactions. His track record includes investments in some of the most culturally significant consumer brands, among them Supreme, Beats by Dre, CAVA, OGX, and 66° North. He has served on more than 15 boards and has handled everything from sourcing through exit, including public offerings and strategic sales.

Before joining Collaborative, Parker oversaw the portfolio at Redesign Health. Prior to that, he led direct investing at Mousse Partners. He spent more than a decade at The Carlyle Group on the Consumer and Retail U.S. Buyout team and began his career at Morgan Stanley.

At Collaborative, we look for partners who recognize that the best businesses are built for the long term. Parker’s track record as an investor and a board member speaks for itself.

We’re glad to have him.

2026-04-15 19:00:00

A few months ago I was in Northern California, visiting a company we’ve known for years. They make one product. They’ve made it the same way for decades. Their customers are borderline religious about it. The business is profitable, growing steadily, and has been for a long time.

Over dinner, the founder told me something I’ve now heard in some version from at least a dozen founders over the past fifteen years.

“I have investors who need to sell. I don’t want to sell. And there’s no one in the middle.”

She didn’t want to go public. She didn’t want to get rolled up by private equity. She didn’t want a strategic acquirer who’d strip the thing down to a margin optimization exercise. She just wanted to keep building the company she’d already built, with a partner who saw the same horizon she did.

I didn’t have a great answer for her. Not yet.

I think about this problem a lot, partly because it keeps showing up, and partly because the conditions that created it are getting worse.

Right now, an enormous amount of capital is flowing toward AI. That makes sense. The technology matters and the opportunity is real. We’re investors in AI ourselves. But one consequence of that concentration is that a whole category of great businesses is being quietly starved of the right kind of capital.

These are companies that make real, physical products people love. Products you can hold, taste, wear, give to someone you care about. They tend to be profitable. They tend to have customer bases that behave less like “users” and more like communities. And they tend to be run by founders who measure their work in decades, not funding rounds.

You know these companies when you encounter them. You probably own their products. A cast iron pan you’ll pass down. A pair of socks guaranteed for life. A soap that’s been made the same way since your grandparents were alive. A bag built to outlast you. They don’t chase trends. They set a standard and hold it, year after year, until the standard becomes the identity.

If you were starting LVMH today — not as a luxury conglomerate, but as a home for brands built on craft, obsession, and generational loyalty — what would it look like?

That question has been rattling around my head for a while. It’s what led us to build Collab Holdings.

Collaborative Fund has spent fifteen years backing companies at the intersection of strong values and strong economics — Blue Bottle, Sweetgreen, Kickstarter, OLIPOP. The thesis has always been the same: companies that align what’s good for people with what’s good for business tend to outperform over time.

But venture capital, even mission-aligned venture capital, has a structural limitation: the clock. A ten-year fund needs liquidity on a ten-year timeline. For software companies growing at triple-digit rates, that works. For a beloved consumer brand growing steadily with healthy margins and fanatical customers, it can be a slow-motion disaster. The fund timeline kicks in, and suddenly there’s pressure to juice growth, dilute the product line, “explore strategic alternatives.” The thing that made the company great becomes the thing that gets sacrificed.

There’s a real gap in the capital stack, and we think we can fill it.

Collab Holdings is a new private equity strategy, purpose-built to be a long-term home for extraordinary consumer brands. No forced exits. No ten-year clock. Success measured by cash flow and customer devotion, not by how quickly we can engineer an exit.

This isn’t a roll-up. We’re not consolidating brands under one umbrella to extract synergies. We’re looking to partner with founders who’ve already built something they’re proud of and give them the capital structure to keep doing it; for five years, ten years, thirty years.

We think the best brands are built by people who refuse to compromise. Who understand that the most valuable thing they own isn’t their revenue — it’s the relationship they have with the people who buy their products. Who believe that protecting what makes something great is how you make it last — and that making it last is how you make it enormous.

Historically, that conviction hasn’t had a capital partner that matches it.

Last month, I came across a letter Warren Buffett wrote to the president of See’s Candy in 1972. He’d just bought the company for $25 million. It’s produced billions in profit since — not because he optimized it, but because he understood what it was and gave it room to be that thing for a very long time.

That’s the instinct behind Collab Holdings. We want to be the kind of partner who understands what a company is — and gives it the room and the capital to keep being that, on its own terms, for as long as the founders want to build it.

If you’re building something like this — a company your customers love in a way that spreadsheets can’t quite capture — we’d love to hear from you.

Please meet: collab.holdings