2026-05-01 15:23:53

The financial industry understands itself to be an arm of the government. We were inducted into this service other-than-willingly through the ordinary operation of law and regulation.

This is uncontroversial and unsurprising to insiders.

A claim which will be more surprising: some regulated financial institutions have delegated authority for account- and transaction-level decisioning to a non-profit.

Another: that non-profit includes a private intelligence agency, which runs covert assets, publishes intelligence estimates, develops target lists, and communicates them to decisionmakers.

Still another: the non-profit organized a coalition of the willing as an outgrowth of its intelligence agency. The willing non-profits, that is. The coalition engaged in a years-long campaign to coerce financial infrastructure and other firms to give them the ability to direct accounts to be closed. The infrastructure built to do this against domestic terrorists was applied to an American politician’s fundraising efforts, and no one seemed to think that was odd.

Last week, the DOJ unsealed an indictment against the organizing non-profit for bank fraud. This was based, in part, on how it paid the intelligence agency’s covert assets.

They likely developed evidence for that indictment using the Bank Secrecy Act (BSA) mandatory reporting regime.

We begin, as always, with the bank fraud.

White collar prosecutions are structurally difficult because they frequently depend on intent. It is difficult to prove intent beyond a reasonable doubt, as it frequently depends on subjective mental states which we cannot directly observe. This problem is discussed in the literature including in book-length treatments.

There exist ways to overcome this difficulty as a prosecutor.

The classic one is waiting for the criminal to violate Stringer Bell’s dictum on the wisdom of taking notes on a criminal conspiracy. You then introduce their notes into evidence. They will frequently contain explicit statements demonstrating mens rea (a legal concept of a “guilty mind”). The register of those statements will be less guilty and more gleeful. Crime is awesome! Wow I sure hope the government never reads this! Because we are committing so much crime right now!

The prosecutorial toolbox has other tricks, too. Rely less on charges which require demonstrating intent. Rely more on what the economics of law field calls bright-line rules. For those crimes, you do not need to demonstrate what emotional valence someone experienced while committing a criminal act. You only need to demonstrate the fact of the act.

Interdicting crime is an iterated game. Responding to our noted inability to manage some forms of crime, legislators have intentionally added some items to the prosecutorial toolbox. Whether one describes them as tools or weapons depends mostly on whether one touches them with the hand or the face.

As Bits about Money has covered frequently previously, the anti-moneylaundering (AML), Know Your Customer (KYC), and related regulatory edifices function in a subtle manner. They do not simply proscribe conduct and rely on perfect enforcement by the financial industry. To achieve the overall objective of stochastically interdicting crime, the regs are designed to force criminals into repeated unpalatable tradeoffs. One is “You can choose making money, or you can choose never interacting with banks, but it is very difficult to choose both.”

We then follow the criminal into the bank. “By the way, lying to a bank is a crime. It doesn’t matter what you think while you’re doing it. It doesn’t matter why you did it. It doesn’t matter if you’re a sinner or a saint. It doesn’t matter if it is a big lie or a little lie. It doesn’t matter if the bank believes you. Lying to a bank is a crime. And everything you say to a bank will be recorded for decades. It will be routinely forwarded directly to law enforcement if the forward-deployed intelligence analysts we force the bank to hire believe there is even a tiny chance law enforcement will find it useful.”

Al Capone infamously went down for the tax evasion because it was easier to prove than the murders. Drug smuggling is sometimes difficult to prove, but the smugglers will want their money in the regulated financial system. The mandatory questionnaire at account opening will ask “Why are you requesting this account?” They will probably not write down “Drug smuggling!”, because a wag who tries doing so will quickly realize this does not successfully result in a bank account. So they will write any other answer. Now they have lied to a bank.

And then, in the ordinary practice of U.S. prosecutors, you will charge them with any crimes you can prove, including the lie itself. And if you are able to demonstrate that it was in fact a lie, which is easier to prove than e.g. rolling up the entire drug smuggling network, you will then make a simple legal request: give us all the money you lied about. That request will be more directed at the banks than the criminal, and the banks will comply, with alacrity.

Sam Bankman-Fried: SBF continues to believe he is innocent. His argument is, effectively, that being the best investor of his generation excuses stealing the principal to invest. That is not a defense in U.S. law, and the indictment charges fundamentally the same conduct (misappropriating money and crypto investors had on deposit at FTX) under a variety of statutory pathways, including 18 USC §1343 (wire fraud), §1344 (bank fraud), and §1956 (money laundering conspiracy).

Let’s focus on the bank fraud. One part of SBF's criminal empire needed banking in the United States. They could not convince a U.S. bank to let them handle FTX customer funds flows. But they wanted to do that. They incorporated North Dimension, a shell entity. Some shells have legitimate business purposes; this one existed only to deceive. North Dimension filled out a due diligence questionnaire. SBF signed it. It said North Dimension traded on its own account and did not handle customer funds.

You need two bits of evidence to convict SBF of bank fraud. The first fits on one page of paper held by one bank. The second is the answer to a single question: “Did at least one dollar of customer funds flow into the North Dimension account?” Thousands of people at dozens of companies, and hundreds of thousands of electronic documents, know the answer to that question and you only need to find one. A single word convicts.

Other charges can stack on the bank fraud. SBF deployed rationalizations about the core fraud counts like a squid deploys ink. Defeating all of them is unnecessary. A money laundering conspiracy requires showing agreement to a) move money that are the proceeds of at least one of a set of “specified unlawful activities” and b) any act to corrupt the integrity of the paper trail about that money movement.

Bank fraud is a specified unlawful activity.

And so you only need one more sentence to get the second charge. Many many sentences will do. Here’s a question to elicit one: “Caroline Ellison, you are a cooperating co-conspirator. During the duration of your conspiracy, while you were the CEO of Alameda Research, did you at any time direct the North Dimension account to move money on behalf of Alameda Research, knowing that by this direction banking records would reflect the money movement to be directed by North Dimension and not by Alameda Research?” A single word convicts.

SBF was, properly and justly, convicted of all of these crimes and more.

He was not the first and he will not be the last. A brief survey for fellow aficionados of this genre:

Dennis Hastert was accused of horrific acts against children but indicted for other crimes. He could not have been successfully prosecuted on the abuse even with a confession, because it was time-barred long before it came to light.

Hastert paid one of his victims to keep him quiet. He was smart enough to make the payment in cash, but the system was smarter sooner, and made a trivial tripwire for attempting to move large amounts of cash out of the regulated banking system: your bank files a currency transaction report (CTR). Apprised of this, he changed his banking patterns to avoid the filing of a CTR. That is called “structuring” and it is a crime under 31 USC §5324(a)(3).

When the FBI asked him about it they used another frequent prosecutorial tool to pick up a freebie. They asked why he had changed his banking practices. He did not say “To structure transactions to avoid the bank filing a CTR when I pick up hush-money.” Instead, he agreed with the agents suggesting that perhaps he distrusted banks and simply wanted to keep hundreds of thousands of dollars of cash on hand. This gave the prosecutors a second charge of lying to federal officials.

In a routine practice, they agreed to dismiss it if he would simply confess to the structuring. The implicit Or Else: “We go to trial, convict you on both, and you get a longer sentence both because the charges stack and because the sentencing formula will mechanically penalize you for this choice.”

Reggie Fowler was the U.S.-based partner of a payment processor which ripped off Tether. It will still be years before we unravel that ouroboros of crime. But that didn’t need to delay the indictment, because he lied to banks that he was doing real estate development. Trivially a lie; his hundreds of millions had bought neither land nor buildings. Our old friend §1344 brought his new bestie §1343 (wire fraud), not because he defrauded Bitfinex/Tether but because he had caused his ill-gotten bank accounts to move money. Every movement is another crime.

George Santos was indicted for a variety of abuses of the public trust. Prosecutions of elected officials are inevitably tricky business, particularly as finding the precise line between crime and politics-as-usual is contentious. (Many people seem to think that line should move radically every, oh, four years.)

Happily, we have bright lines which don’t move, like “don’t steal credit cards” (§1028A). You can convict on that without needing to explain whether it was done with a gun or a political donation portal.

Then you stack on wire fraud again, because we intentionally make it hard to spend directly on oneself from politics-adjacent pools of money, and so you need to move money at least once to enjoy it.

Why do these indictments, and hundreds more, rhyme so much? Why can we employ these charges to such devastating effect against the rich and powerful, even those in positions of public trust, even those with allies who still love them? Because we maintain textbooks of how to make these cases and make them stick.

White collar criminal cases are like any other high-end bespoke services work. One could imagine that the production function is fully artisanal, like something out of a traditional French restaurant.

You, an aspiring lawyer, labor for years under the eye of a terrifying supervisor. He periodically steps behind you, rips a brief from your hands, screams at your incompetence, and you have learned one new thing. After twenty years, you now write your own indictments. They bear his distinctive stamp but your signature. You have added your own spin, which you will pass on to the rising generation, via the traditional mix of hazing and hands-on instruction.

This happens. But in law, as in restaurants, we are allowed to write down recipes and tell people to just follow the steps.

For example, we in the financial industry are obliged to file Suspicious Activity Reports (SARs). These are basically three-ish page memos. Combined with statutory tools such as those discussed above, these memos will giftwrap charges and convictions. They get saved by the Financial Crimes Enforcement Network (FinCEN) for decades and some small fraction of the four million filed every year will eventually be read by a public servant.

The bank pays the screening vendor which fires the alert, the bank pays the intelligence officer who reviews it, the bank pays the senior compliance analyst to spend a few hours collecting data from various employees and web applications into a single coherent narrative. And then the public pays the prosecutor to copy/paste the SAR into an indictment. (Accept this as a slight exaggeration, but if you can’t name a paragraph lifted from a SAR into a federal criminal indictment, you will be able to in about five minutes.)

FFIEC BSA/AML Examination Manual:

One purpose of filing SARs is to identify violations or potential violations of law to the appropriate law enforcement authorities for criminal investigation.

…

Examples of agencies to which a SAR or the information contained therein could be provided include:

A diligent public servant is welcome to use FinCEN’s database to get additional information on the subject of an existing investigation. But FinCEN will happily tell you the other sequencing works fine: trawl the database “proactively.” Most SARs are not evidence of crime! But if you have the choice between doomscrolling Twitter and doomscrolling the SAR database, one is much more efficient at converting into prosecutions. Their phrase for this is proactive SAR review and they have twenty volumes more if you are interested.

Very few Americans not professionally implicated in this surveillance regime understand it exists. FinCEN employees and bank compliance officers depend on it for their continued employment, and so it might be understandable why they are such effusive fans. But the regime does have informed critics, including occasionally this author.

One critique is that this regime is functionally an end-run around the Fourth Amendment. Civil libertarians have made this point for decades, but never with the economy of phrase as the U.S. Immigration and Customs Enforcement (ICE) internal magazine Cornerstone’s article The Currency Transaction Report: Controversial To Some—Essential To All.

Why is the CTR so useful to law enforcement, ICE?

ICE: ICE special agents utilize CTRs to establish links between individuals and businesses, and to identify co-conspirators and potential witnesses. This information is often utilized to meet the 'probable cause' requirement necessary to obtain search, arrest and seizure warrants.

Is this surveillance regime narrowly tailored?

ICE: ICE conducts approximately 1 million record checks of BSA data each year.

If a libertarian were scripting you right now they’d ask you to say that innocents have nothing to hide.

ICE: Individuals and businesses conducting legitimate transactions have no reason to avoid the filing of CTRs.

Yikes. Say, did you ever articulate the intentional double-bind twenty years before Bits about Money did?

ICE: However, criminals are forced to make a choice between appearing to be a legitimate customer, thereby exposing their assets and money movements through BSA reporting requirements, or engaging in risky, illegal actions to conceal the movement of their funds.

Wow, it seems like this field is filled with carefully laid traps that function exactly as designed. Did you by chance happen to publish the Hastert prosecutorial strategy ten years early?

ICE: Suspicious attempts to avoid the filing of a CTR by structuring cash deposits (making a series of deposits just under the $10,000 reporting threshold over a number of days) is a significant red-flag indicator of criminal activity and one of the most frequent triggers for the filing of a SAR.

Which brings us to the Southern Poverty Law Center (SPLC).

On April 21st, 2026, the Department of Justice unsealed an indictment of the SPLC for bank fraud.

The SPLC is a storied civil rights organization. Like many non-profits, it runs a portfolio of what are sometimes called “programs” under a single roof. One of those programs is producing a data product listing individuals and entities that it considers to be involved in hate and anti-government activities.

That data product is important financial infrastructure, and we will return to it in a moment.

The SPLC runs a private intelligence service to produce it. The SPLC has in the past paid informants, who it describes as “field sources.” Those informants are generally members of what it describes as domestic terror organizations. The existence of this program has been public knowledge for decades.

It is unlikely that any magistrate in the United States would approve a warrant to search the bluest-of-blue-chip civil rights organization's papers on the suspicion that they have created a fictitious CIA to launder money to the wife of an Exalted Cyclops of the Ku Klux Klan. Are you not aware, officer, that the reason this organization is in high school history texts is they developed a novel civil litigation strategy to bankrupt the Ku Klux Klan? You will not get your warrant. You would be lucky to escape court without a citation for contempt or an order for psychiatric commitment.

Well, good thing nobody ever had to ask for that warrant.

Banks don’t need warrants to become quite alarmed when they discover that they have created an account for the Center Investigative Agency and several other sole proprietorships for the same person… and those businesses don’t receive revenue, run payroll, buy office supplies on their debit card, or rent office space. No, the only thing they do is take large deposits then transfer out hundreds of thousands of dollars directly to, Great Scott, the worst people imaginable.

Substantially every employee of the financial industry, CEO or teller or product marketing manager that they may be, is obligated to attend a yearly training on their BSA compliance responsibilities. That training customarily requires you to pass a test. If that test stipulated this scenario and then asked what the financial institution must do next, there is only one correct answer: Conduct an investigation, close the accounts at issue with very high probability, and file a Suspicious Activity Report.

We return from this flight of fancy to the indictment. Excerpting verbatim:

Starting in the 1980s, the SPLC began operating a covert network of informants who were either associated with violent extremist groups, such as the Ku Klux Klan, or who had infiltrated violent extremist groups at the SPLC's direction.

If one does not closely follow this community of practice, one could be forgiven doubting whether prosecutors are being candid here. This claim does sound farfetched. The indictment, in this paragraph, is neutrally recounting the truth. The SPLC is proud of that program, which it ran for decades. NPR’s gloss:

The indictment came shortly after the SPLC revealed the existence of a criminal investigation into its disbanded informant program to gather intelligence on extremist group activities.

Well, OK, they ran an intelligence agency. One can construct a narrative by which that makes some tactical sense. Sure.

How did they get a bank to go along with making payments to people who the SPLC has spent decades attempting to make it impossible to pay. Did they perhaps… lie to a bank?

Indictment:

To secretly funnel donated money to the Fs, individuals at the SPLC, including a person who would become the Chief Financial Officer ("Employee-1") and a person who would become the Director of the Intelligence Project ("Employee-2"), among others, opened a series of bank accounts at Bank-1 and Bank-2 in the name of various fictitious entities, including, but not limited to, the following: Center Investigative Agency ("CIA"), Fox Photography, North West Technologies ("North West Tech"), Tech Writers Group ("Tech Writers"), and Rare Books Warehouse ("Rare Books").

Oh dear, SPLC! It would be extremely bad for you if you had in fact opened accounts for businesses which do not actually exist, then used them to move funds! Perhaps you can just pray that the feds never find out? … The bank is quite likely going to find out, though. Some bank accounts have red flags. These red flags have bank accounts.

Indictment:

In 2020, Bank-1 conducted an internal investigation into these accounts.

Oh that’s… unsurprising given the asserted facts. Well, your options are diminishing rapidly at this point.

Hey quick intermission: want a surprisingly reliable way to combat credit card fraudsters, drug dealers, and the like? First, you identify one of their accounts which is definitely committing crime. Usually they have lots of these and cycle through them quickly. They are often opened with synthetic or stolen identities. Burning the identity doesn’t get you all that much; they have thousands to cycle through. So just freeze the money in the account. Then, rely on human nature: nobody likes giving up “their” money. So compassionately offer to help them out, by offering to transfer the money from the frozen account to another account they control. We just need your quick written instruction to send your money to your other account, sir.

Indictment:

Thereafter, an SPLC employee requested that Bank-1 close the accounts associated with the CIA, Fox Photography, North West Tech, and Tech Writers and transfer the remaining balances in these accounts to a Bank-1 account ending in 6050 held in the name of the SPLC.

Industry practice varies on whether you give the user their money back before filing the SAR.

There are some grey areas in practice. You can’t return the money if you understand the user to be e.g. Hamas. You might be able to return the money if you understand the user to be e.g. engaged in unsupportable but debatably legal behavior.

“Unsupportable” here is a term of art: the institution, in its considered judgement, cannot allow it to happen on systems it controls. Many legal acts are unsupportable, and a determination of supportability is not and cannot be coextensive with a criminal conviction. Compliance officers are not federal judges and are happy to defer to them.

Please, we beg you, do not ask Compliance to run a parallel criminal justice system. We will do it if you force us to, but you will not like the outcome.

One of the functions of getting an explanation in writing from the SPLC (we will get to it; it is a doozy) is the financial institution seeks to absolve itself. Did we open accounts for cutouts to a domestic terrorism organization? If we did, *#%(, our regulators need to hear about that today. But this admission can be shared with a later regulator to say “We were unaware of the actual ownership of the accounts when opened and for ten years of use, which we agree is bad. We then executed our responsibilities with urgency. On the strength of this communication from the SPLC, which is not a terror organization, we decided to not immediately call you, and instead relied on the ordinary processes of our Compliance function. We will listen attentively if you feel we were ever derelict in our duties.”

One of those duties: a financial institution must, as a matter of black letter law (31 CFR § 1020.320), file a SAR if its investigation discovers a transaction designed to obscure the provenance of money. Transactions, by their nature, reference the account title (ownership, which could be by a e.g. company or trust) and beneficial ownership information (the ultimate people who have economic interest in the account). Any transaction conducted by an intentionally mistitled account is immediately and mandatorily reportable as soon as the financial institution has knowledge of this fact.

Alright, options for the SPLC are narrowing precipitously, but perhaps it can argue that those two employees, senior though they might be, were acting rogue? Or perhaps they could argue that the SPLC was institutionally unaware of the specific financial infrastructure its employees had created to support the SPLC’s intelligence program?

Indictment, quoting the President and Chief Executive officer of the SPLC, to the bank:

Pursuant to the discussion we had earlier this week, please let this correspondence serve as confirmation that the accounts listed below were opened for the benefit of Southern Poverty Law Center operations and operated under the Center's authority. The following accounts are listed below:

...6700 Center Investigative Agency — opened 1/31/2008, closed 8/5/2020

...9674 Fox Photography — opened 1/31/2008, closed 8/5/2020

...6743 North West Technologies — opened 1/31/2008, closed 8/5/2020

...6751 Tech Writers Group — opened 1/31/2008, closed 8/5/2020

...6719 Imagery Ink — opened 1/31/2008, closed 3/15/2013

...6727 J&J Electronics — opened 1/31/2008, closed 3/15/2013

...6735 Kelly's Marine — opened 1/31/2008, closed 3/15/2013

There are a variety of ways for the DOJ to get the CEO’s email. It may have been attached to a SAR, and therefore filed automatically with FinCEN. The other way, of course, is to pivot from a SAR (or any other reason to open an investigation) to a request that the bank produce records. Subpoenas are not strictly required; that document exists to exonerate the bank. A financial institution, concerned it is falling under negative government attention, might proactively offer to share what they know.

In any event, the feds got what they needed.

This written communication is a succinct confession to bank fraud.

There are multiple different ways to charge it, as we have seen. The indictment went with §1014. And if the SPLC admitted to bank fraud, then the transfers are wire fraud. And if the transfers were wire fraud, then the… you’ve seen this movie before and it ends predictably.

I do not expect this conclusion to be a happy one to all readers. I believe it to be correct.

There exist lawyers who say that the legal analysis in the indictment is sloppy. That statute is a weapon. Weapons wielded sloppily hit the target all the time. A weapon that only works when wielded perfectly is poorly designed.

Some commentators have implied theories that, for example, §1014 only applies to applications for loans. Excerpting the statute:

Whoever knowingly makes any false statement to… any [FDIC-insured institution]... upon any application… shall be fined not more than $1,000,000 or imprisoned not more than 30 years, or both.

This is extraordinarily broadly drafted, by design.The long list of alternatives to application includes loan, and as a basic principle of statutory construction, this means that Congress considered limiting the list to only loan applications and then intentionally did not do that.

In Wells, the defendant sold something of value to a bank, rather than borrowing money from them. (Turns out copiers print money, in a sense; you can sell the future revenue stream.) The lie was a relatively tiny detail relevant to the pricing discussion. Wells was prosecuted under §1014. The controversy was not “Does §1014 allow prosecution outside of loans?” Yes, read the plain text of the statute. But the holding is as interesting as the data point. Can you be convicted of fraud over a tiny lie? The Court held there is no materiality requirement under §1014. You can be convicted of fraud for a lie that doesn’t matter if you tried to influence any decision of a bank.

Some have advanced the notion that the account application is misleading but not false. This matters due to Thompson, decided last year by the Supreme Court, which holds that §1014 doesn’t cover misleading but true statements. Consider what happens when the prosecutor summons a senior SPLC executive to the stand and says: “So, Fox Photography, which you ran as a sole proprietorship. Did you buy a camera? Did you advertise? Did you file for a DBA? Did you make a website? Does Fox Photography have any activities other than this bank account application? You had three other businesses. Which of them did anything other than obtaining banking services?”

Some believe, plausibly, that the prosecution is politically motivated. Others might counter that the SPLC is the nation’s leading expert in lawfare and has just discovered sauce for the gander. Still others might believe both claims. Or they might believe “This looks like retaliation for the SPLC coordinating a coalition to interfere with Trump political fundraising,” which is not the way coalition participants say the SPLC gained his enmity [archive]. We will return, at length, to the activities of a coalition the SPLC co-founded.

Many commentators have argued that this program has been discontinued. Yes, bank fraud will frequently cease after its discovery. That is definitely a goal of this apparatus, and is almost definitionally true. Almost all white-collar prosecutions will happen after the conduct giving rise to them has ceased. The financial industry would certainly be chagrined to learn about a live fraud happening on its rails from the indictment. (That does happen; we have processes to detect it happening and then immediately investigate accounts associated with entities that were just indicted. We will discuss how data products and screening infrastructure function in substantial detail below.)

The industry as an institution expects its supervisors in government to bring these cases, all the time, against targets that have many friends, positions of authority, extremely competent defense lawyers, and sincere belief that they are innocent of any real crime. The government expects, as an institution, to be overwhelmingly advantaged in these cases.

Many commentators, including the government itself, have made this indictment mostly about the fraud against donors. Many believe that argument to be a stretch. I agree, unreservedly. As a connoisseur of this genre, I have read few documents which are simultaneously so far from the conventions while adding so little new to the canon.

It is a stretch that the government routinely makes and wins in other contexts. Matt Levine has collected several hundred examples of the genre, which he calls Everything Is Securities Fraud. That genre is, succinctly, “If you run a for-profit corporation, and have raised money from outside investors, and anything at all goes badly, and you did not describe exactly that thing to the investors as a risk, you have arguably defrauded your investors.” The government is comfortable making that argument and wins it routinely.

Perhaps Everything Is Donor Fraud. Perhaps not.

But, again, the design of this system is so you don’t have to prove the hard crime, the one where you’re being creative and taking some risks and pushing the envelope. You only have to prove the easy one, in exactly the same way hundreds of cases have won before. You will then use the spectre of conviction for (minimally) that as procedural leverage, and your target will likely settle.

Absolutely textbook.

A brief break from the SPLC’s situation. We’ll return in a moment. I had promised you a discussion about how the financial industry uses certain data products, including one published by the SPLC. We will begin with the canonical example of a data product.

As BAM has noted in discussing so-called debanking, the United States does not maintain a secret blacklist of people who can’t gain bank accounts. It maintains a public one.

Regulated financial institutions must deterministically reach the correct conclusion about accounts or transactions where they benefit certain people and organizations. That blacklist is called the Office of Foreign Asset Control (OFAC) list of Specially Designated Nationals (SDN). In broad strokes, this is a blacklist for foreign terrorists and narcotraffickers. (Banks aren’t the only people who can’t transact with the OFAC list. Reader, if you are an American, you can’t either, under penalty of law. But enforcement action is concentrated against banks et al because they are a, how might one phrase this, choke point for money movement.)

In theory, every time a bank opens a student checking account, it can have a bank employee mosey on over to the OFAC website, search the list in real time, and then determine that the prospective customer, yep, isn’t on the OFAC list. This is quite impractical and unlikely to be considered an acceptable set of controls by a regulator unless it is the smallest-of-small-town community banks.

You could write your own software to periodically download the list (yep, we just publish the files) from OFAC, and then compare new accounts and in-progress transactions against your recently-synced copy in your database. Most financial institutions do not choose to do this. It is fiddly, extremely high downside if you get wrong, and has zero financial upside if you do a better job than “minimally adequate.” Also, you have to do it many times redundantly across hundreds of functions of your financial institution. Checks, wire transfers, accounts payable, even your employee giving program! This set of considerations spells “outsource this function.”

The jargon for the function is “OFAC screening” and the company or companies which the financial institution engages to handle this are selling “data products.” You will work with your vendors and your internal IT teams to integrate those data products (which might be APIs, or platforms, or similar) with your other IT systems.

Then you turn everything on. Presto! You get alerts sent to Compliance if someone appears to be OFAC-listed. One of the large team of intelligence analysts you are forced to hire will be instructed to click through alerts as they stream by. The interface frequently resembles a Twitter feed from the most boring possible circle of hell.

Your analyst will tell the system to ignore the false positives (extremely common relative to true positives, but you basically have to look at every one) and action the true positives. “Action” here means close the account or block the transaction. A close synonym is “decision” the account.

If you’re technically sophisticated, you can probably configure your screening vendor to pass alerts off to some combination of heuristics, machine learning models, and other AI techniques before they are sent to a human. Alert fatigue is real and dangerous. You can decrease it by automatically decisioning low-risk accounts/transaction, based on criteria acceptable to your regulator, which you will write in your policies. Perhaps you have recorded that you have a U.S. passport or other evidence of citizenship on file for the account holder and therefore it is vanishingly unlikely they are the SDN whose citizenship is Farawayistan even if the names look similar. You might reasonably argue that, for retail accounts that are incapable of moving large amounts of money, that is good enough.

A bit of engineering and Compliance jargon: this architecture is a pipeline. An alert enters the pipeline from your screening vendor. It goes through some automated decisioning and routing to end up in a particular queue for a particular team of analysts. They decision the alerts which will, in some cases, be the end of it. In other cases, this will result in a new type of entry in a new pipeline, perhaps to effect the series of actions one must take to offboard an account. Pipelines are serviced by a mix of technical and human systems, and governed by both computer code and process documents written in English. Both the code and the documents are subject to review from your regulators. (They are far more likely to read the documents than the code, but they have essentially carte blanche to ask Compliance for anything they want that describes e.g. the OFAC pipeline, and Compliance will probably not push back very hard. Keeping a positive relationship with regulators is a very large portion of their job.)

The OFAC list is the canonical data product, but your screening vendor really wants to sell you several. Can you charge for a list the government makes freely available? Absolutely! Because the screening vendor isn’t simply charging for the list. They are charging for a complex technical and human system around the list.

One factor among many: you expect the list to change and you want them to be in charge of making sure you always have a very recent version. You also want them primarily in charge of understanding the e.g. regulatory environment around their data products. If one of the products goes from advisory to mandatory, you want to learn that from your vendor before you learn that from a pissed-off examiner wondering why you didn’t read the bulletin two years ago.

Some data products have very different characteristics than the OFAC list.

One example, alluded to above, is repackaging criminal indictments into a screening list. You might bank Bob’s Autos. If Beneficial Owner Bob is indicted as a money launderer for the mob, you want to know that very quickly so that no one e.g. drives off with the balances in Bob’s Autos’ accounts.

But you don’t have to close an account if someone is indicted, not like you have to close the account if they’re added to the OFAC list. It’s a judgement call, and you’ll have described your decisionmaking process for it in internal procedures documents, and your regulator will have blessed them. So one of your intelligence analysts gets the tweet-sized version of the indictment from the pipeline, reads “Misdemeanor assault”, and probably decides “Bob’s in trouble, certainly, but still supportable.” Or they read “Felony bank fraud” and that analyst very likely kicks off an internal investigation. Or, and again this is the dominant case, Close As False Positive. Turns out there are a lot of Bobs in the world who own car dealerships; that Bob was not our Bob.

Another data product is so-called “adverse news” screening. This one is not an extension of state power like the OFAC or prosecutorial lists, not directly. You have much more discretion on whether you buy it than you have on OFAC screening. But your screening provider might have gone to the trouble of licensing wire service articles or newspaper feeds or the Twitter firehose or similar. They repackage it and match e.g. mentions of colorful local businessmen (a classic newsroom euphemism for “mob, but we can’t prove it and he has lawyers ready to sue for defamation”) to your accountholders. If a colorful local businessman is reportedly on the lam and feared to have left the country, and then he asks for an international wire transfer, you probably don’t want to simply process it.

And now the data product you’ve been waiting for: the SPLC Extremist Files. Like the OFAC list, it’s available for free on their website, but there do exist screening providers which will happily charge you for it. Part of that work is for scraping, part of that work is for e.g. matching names to e.g. charity EIN numbers, etc. Your screening vendor will happily tell you, though, that the data product they’re selling you is really SPLC’s considered judgement, packaged in a way that makes it easy to include into your pipelines.

Why would you buy this data product? In part, it is because the financial industry broadly considers the SPLC an extraordinarily trustworthy non-profit. It is widely believed that if they say you’re a Nazi, you’re a Nazi, and we don’t want to do business with Nazis. Financial institutions, like other firms in capitalism, have broad discretion (with some specifically enumerated exceptions) in choosing who they do business with.

An aside to conservative and progressive critics of the SPLC: yes, I know, they are not as selective, restrained, and expert as their reputation suggests. But please accept for the moment that the financial industry understands this less well than you do.

One citation for the industry broadly considering the SPLC reliable and being aligned with their views on the good: JPMorgan Chase, the largest bank in the U.S., practically a metonym for conservative-as-a-banker, gave them $500,000 specifically to "work in tracking, exposing and fighting hate groups and other extremist organizations."

If you were to have a thousand conversations in the financial industry about non-criminal clients you don’t want to do business with, you would hear the SPLC cited more than any other group or data product.

Some of the most established screening providers do not carry the SPLC data product, though they have data products which compete with it. The SPLC has in the past criticized those providers by name:

World-Check is often criticized by civil rights organizations, advocates, and experts on international terrorism for bias and misinformation that can result in the blacklisting and de-platforming of legitimate charitable groups. The commercial nature of World-Check, its lack of coordination with civil society organizations, its use of unsubstantiated data, and its lack of transparency make it a highly problematic tool to screen out hate.

In substance, the SPLC’s complaint is that our competitors list people we wouldn’t, don’t list people we would, and we’re just better at this. Which, fair enough, everyone is allowed to have an opinion.

How did we arrive at the position where financial institutions clamored for their data providers to offer SPLC screening? Marketing and sales are skills and the SPLC is very, very good at them. Also, again, read a history book of your choice; they picked a fight with the KKK and won. If you get a reputation for doing that for decades and also have an aligned product many customers feel the need for, sure, they will want to get it from you specifically.

That is not the only reason why many people in tech companies, financial infrastructure companies, and banks are intimately acquainted with the work of the SPLC. We will return to the other reason in a moment.

But, what does your SPLC pipeline do? Depends! Perhaps alerts go to an analyst, who checks it for false positives (yep, hits will frequently be false positives), and in the case of true inclusion you have a spirited debate within your firm. Perhaps some people argue that even Nazis need to eat, and to eat you need money, and that on balance the marginal harm of giving this particular Nazi a checking account is outweighed by the social utility of their children not starving to death. You are consuming the SPLC’s data product on an advisory basis; your firm retains full control of decisioning.

Or you could configure your pipeline to automatically deny services to anyone the SPLC lists, either by operation of computer code or by the programmatic-but-in-the-sense-of-directing-humans way that many processes still work in the financial services industry.

Jeff Bezos, in Congressional testimony, describing Amazon's reliance on the SPLC data product for AmazonSmiles, a now-discontinued charitable product they offered:

"We use the Southern Poverty Law Center data to say which charities are extremist organizations. We also use the U.S. Foreign Asset Office [sic] to do the same thing.”

Bezos was interrupted before he could finish his next thought; you're welcome to read the testimony for full context. He is clearly referring to the OFAC SDN list.

Bezos went on to elaborate that the Fortune 2 company could not operate AmazonSmile without some way to kick out the extremist organizations and that SPLC was, effectively, the only reasonable option. He asked Congress for other suggested data providers. None were offered. (No, really, he did that.)

Let us pause to acknowledge that Bezos, one of the richest men in the world, considers these two four-letter organizations as peers. One of them is created by statute, operates within constitutional and administrative-law constraints, and answers to Congress, the courts, and ultimately the people of the United States of America. It could jail Bezos, personally, for willful non-compliance. And the other is …some people in Montgomery with a very specific interest, whose decisions are subject to review by no court, and whose only power appears to be moral suasion.

Bezos was equally and entirely committed to satisfying both.

Why? We’ll return to it in a minute.

As a longstanding financial infrastructure enthusiast and practitioner, I am confident that SPLC screening is used on an advisory basis in very many sectors of the financial industry. It is also used in a delegated authority fashion for some products at some firms, in the fashion that Amazon used to. In the delegated-authority cases, an SPLC hit kills an account application or transaction as cleanly and automatically as an OFAC hit does.

Perhaps that strikes readers as implausible, even after you just heard it in sworn testimony to Congress. I offer to you publicly documented examples, frustrated that they all cluster in a small set of the vast panoply of financial products. There is a reason for that clustering, related to the SPLC’s marketing and sales motion, and we will discuss it in a moment. A warning: if you assume the public examples are fully representative of the SPLC’s delegated authority you will materially underestimate how much actual power the SPLC has over financial infrastructure.

Many employers in the United States offer a perk: if you donate to charity, we’ll match what you donate, up to some dollar amount and subject to some restriction. This is, morally, compensation, just like the salary is compensation, just like the 401-k match is compensation, just like the healthcare benefits are compensation. Firms use specialist providers of financial services to run payroll, administer 401-k plans, and deliver health insurance.

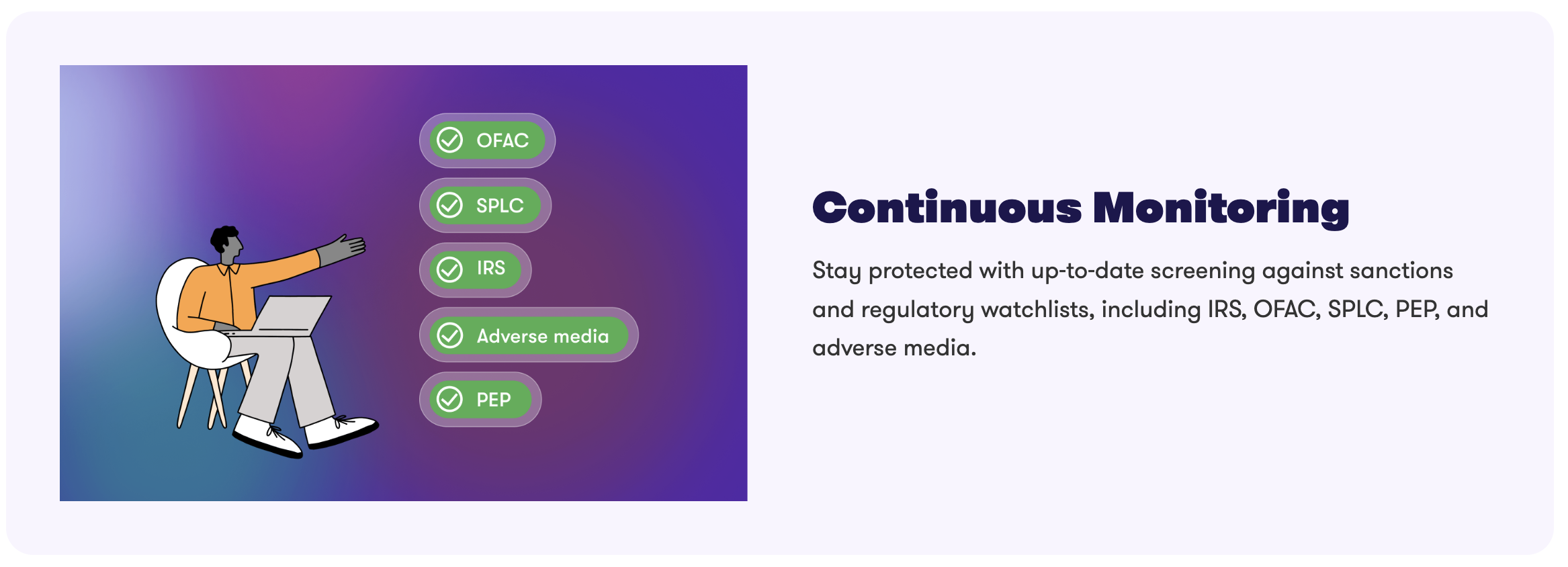

Deed offers a workplace giving program as a service (WGPaaS? We’ll workshop it.) Some Deed customers are banks, and so they have a ready answer [archive] for your Compliance people on the work Deed already does on your behalf: Continuous Monitoring: Stay protected with up-to-date screening against sanctions and regulatory watchlists, including IRS, OFAC, SPLC, PEP, and adverse media.

One of these acronyms is not like the others.

This perk is quite popular in banks, who have been trying to shake the heartless image since the Medicis, and who want people to feel good that they teleport value through time and space but also really and truly care. So some financial institutions in the United States, possibly without knowing it, may have, in delegating authority to Deed to decision requests for compensation, indirectly delegated it to the SPLC.

I assume, as enterprise-grade software, that many workplace giving programs have many levers available to customers if they want HR to review every match of a $20 donation to someone’s parish. As a self-evident statement of prioritization: no, HR does not want to do this, at all, ever, please stop wasting my time, configure it the way you do for every other bank. Do you expect Customer Success to press on and say “Nope, sorry, not enough to proceed. Is being able to donate to Nazis important to your employees?”

An observation from someone who worked in the marketing department of a financial services company: features on the industry-specific solutions page are there because customers care about them and not having them is a dealbreaker. So you must offer the SPLC screening to customers. But it is socially impossible to ask whether they want it. Product decision time: what is the default value of the Allow Gifts to Nazis checkbox.

Now, a quiz: do you think Compliance at a bank is neutral on “Can the bank delegate transaction-level decisioning authority, in any part of the business, however small, to an entity under federal indictment for bank fraud? Does the answer change if they are convicted of bank fraud?”

No! Compliance will not let you do that! Not because they are worried about the integrity of the blacklist. An accused bank fraudster has the final say to approve money movement out of a regulated financial institution. That is very likely intolerable to Compliance.

What happens next? Well, remember, when you bought the data product, you were also buying someone anticipating your concerns before you even voice them and preparing options before you ask. Jeff Bezos’ words echo in San Francisco today: Does anyone know another option?

Deed is not an outlier in workplace giving programs.

Groundswell? The FAQ recently read “Groundswell does not process donations to organizations denoted as hate groups by the Southern Poverty Law Center.” but changed to “Groundswell conducts due diligence to confirm they meet applicable IRS standards. Clients can also configure their own charitable restrictions within Groundswell, including allowing or blocking specific organizations or categories of organizations, in accordance with their internal policies.”

No prizes for guessing the default.

Millie? Blog: "Vetting nonprofits can be a time and labor sensitive task… That is why vetting is typically left up to the experts at SPLC. All vetting for the Millie database is even through the SPLC!” [sic throughout] [archive]

And, again, you are reading the tip of the iceberg. There is much more use of the SPLC list in the financial industry, in much more important products than workplace giving.

Why is it so easy to find public evidence in giving programs but not of SPLC blacklisting in e.g. life insurance or wire transfers or options trading?

The SPLC and its allies bootstrapped a consensus in their core community of practice, non-profits and the supply chain that funds them. I will describe the shape of that consensus without making specific claims about truths. It is: either you’re screening charitable donations for hate funding, or you are a monster. You will not attend our parties. You will not get our retweets. You will be iced out of the flow of money, because we have friends at Ford. One phone call and Open Society is closed to you. And then good luck paying your staff. We have spent our professional careers getting very good at delivering social consequences through tightly coordinated coalitions. Get with the program, or get consequenced.

If you want to understand why the charitable giving world moves in lockstep here, start with the Amalgamated Foundation's "Hate Is Not Charitable." You will find it a project to reconstruct what that did, but the SPLC has a whitepaper with most of the important story beats.

It's a long story, and I would rather tell you a different story, about how the SPLC formed a coalition to gain account- and transaction-level decisionmaking capability at tech companies, financial infrastructure firms, and banks through a coordinated pressure campaign.

Parts of this story are abundantly reported in public. Parts are extremely well understood in the organizations that the SPLC’s coalition repeatedly persuaded, cajoled, or threatened (pick your favorite verb for the moment).

Some parts of the story are original public interest reporting. What is the public interest in candidly recounting the exercise of power over Nazis? Because they did not stop once they achieved power over the Nazis.

One coalition of non-profit organizations ran an organized pressure campaign against industry, for years. It started in 2017, with the SPLC and another non-profit informally coordinating. It intensified and formalized in 2018, under SPLC co-leadership. It escalated sharply in 2020 and 2021.

The campaign had two main components. The first was public advocacy and communications work. The second, less visible but more consequential, was a series of meetings with industry. Hundreds of meetings. With a specific target set of companies.

The campaign's declared aims were three. To convince those companies to censor more communications the coalition characterized as hate. To blacklist organizations and individuals the coalition characterized as promulgators of hate or violence. And to interdict the flow of funds to those blacklisted parties.

The coalition claimed to be non-partisan. Be on the lookout for mentions of “non-partisan,” because it is a word the coalition understands differently than I do.

The coalition calls its targets “Internet companies” and relies on government, media, and the public to not read the fine print. In it, they define Internet company mendaciously to include banks, credit card processors, and any other financial infrastructure their enemies could touch. The coalition was going after posts, but it was also and primarily going after money. I will use the language “industry participants” going forward to identify who they met with.

Industry participants included Facebook, Twitter, JPMorgan Chase, Visa, Mastercard, and many other firms. Some were among the largest companies in the world. Others had fewer than 10 employees. (I estimate headcount based on published reporting and industry experience.)

Stripe was an industry participant. I was employed at Stripe continuously from late 2016 through early 2023, covering the entire period under discussion. I remain an active advisor to Stripe. Stripe does not necessarily endorse what I write in my personal spaces.

This series of hundreds of meetings involved hundreds of employees from industry participants. Those employees included C-suite executives and managers and individual contributors across a host of functions. Those functions included communications, legal, government affairs, Trust and Safety, and compliance professionals.

Meeting notes were frequently kept, and sometimes widely circulated, as is the routine practice in industry. The meetings were documented on calendar invites (often with full participant lists), shared docs, attachments, emails, and other contemporaneous records. In the ordinary practice of industry these primary documents distribute themselves promiscuously into secondary documents; think of an email being screenshot to paste into a PowerPoint to discuss the response in a meeting. Records exist on conservatively hundreds of systems and can be accessed by many more than 10,000 people.

No employee of an industry participant I have spoken to, familiar with the contents of the meetings, was willing to provide quotes for publication with their name and corporate affiliation attached.

Their reasoning included not being authorized to disclose private information, fear for their personal and corporate reputation, future career consequences for leaking, personal consequences for being identified adjacent to national political controversies, in some cases fear for their physical safety, and in some cases unwillingness to betray a cause they personally support.

Industry participants recount the tone of the meetings differently, and as varying over the meetings. Some meetings were strained-but-professional. Sometimes the coalition participants were described as demanding and “hectoring.” Industry participants report abusive remarks towards their companies and to the people in the meeting.

Industry participants were repeatedly told that if they did not accede to demands they would be profiting from evil, complicit in the death of innocents, or benefitting from white supremacy. The innocents claimed to be at risk were often specifically identified as black, including during a period of intense societal concern for the lives of black Americans specifically. Industry participants were told that they wanted this. That they were taking “blood money”. Industry participants repeatedly felt personally attacked, in ways and using language not normative in their professional experience.

On the account of multiple industry participants, coalition participants explicitly held individuals in the meeting personally responsible for the actions of their employers. This was aimed at individuals with substantial influence and authority in companies, and also at junior employees.

Industry participants describe the coalition participants as threatening their employers, openly and by implication.

The most commonly described threat was coordinated negative public messaging with the goal of causing reputational harm to the industry participants. Feared comms outcomes ran the gamut from heavy mainstream media coverage to a Twitter pile on. Twitter is real life, particularly when a large and vocal contingent of your employees use it and Slack simultaneously. Ever been pulled into a meeting over a single customer tweet then burn weeks on managing the fallout? Count yourself lucky.

Less commonly, the industry participants perceived they were being threatened with adverse legislative, executive, or regulatory action indirectly by coalition participants who are reasonably read as exercising substantial political influence. Industry participants sometimes report that coalition participants flaunted their political influence.

Industry participants were repeatedly told that if they did not accede to specific demands, they would share the blame for future deaths. Bits about Money has reviewed contemporaneous records which unequivocally make this claim, authored by coalition participants. We note that this echoes language the coalition routinely puts in press releases, Medium posts, and similar artifacts after presumptively careful review of the phrasing. The coalition was inconsistently disciplined in phrasing in documents we have reviewed, and we decline to quote their phrasing, in part, out of charity.

You will share the blame. We will hold you responsible.

The coalition has publicly and voluminously described their own understanding of what was said in those meetings.

Where employees of industry participants dispute their characterizations, I will characterize broadly what some employees of industry participants have said, to preserve their anonymity. You should not view this as a claim on behalf of all industry participants. Patterns emerge frequently, but I am making no claims about unanimity.

Many left-of-center voices felt that white supremacists had been emboldened by the 2016 election of Donald Trump. Beginning in mid-2017, Color of Change communicates with and meets with PayPal, with the objective of cutting off financial services to hate groups. Color of Change is a civil rights organization which specializes in online organizing.

The Center for Media and Democracy, an aligned non-profit, quotes a senior executive as saying “Let’s be clear: public speech promoting ideologies of hate always complements and correlates with violent actions.”

Industry participants characterize the coalition participants as asserting that speech was inseparable from conduct. Free speech concerns were dismissed and, industry participants report, mocked, including with the dismissive rendering “freeze peach.”

As has been abundantly reported elsewhere, a coalition of white nationalist, neo-Nazi, and alt-right organizations (per voluminous public reporting tracking self-identification) organized a rally in Charlottesville, Virginia. This sparked counter-demonstrations. A rally attendee struck and killed a counter-demonstrator with his car.

Color of Change intensified its existing engagement with PayPal and other industry participants. Rashad Robinson, then executive director, would describe them in detail later, to a podcast on iHeartRadio. Fast Company [archive] approvingly cites that this came after “Robinson used similar tactics to move companies to withdraw sponsorship from the 2016 Republican National Convention.” The Republican National Convention is a get-together sometimes described as a grand old party.

Robinson articulated the coalition’s theory of change: “Power is the ability to change the rules.” The coalition perceived the industry participants as having power, desired power for itself, and took steps to achieve it.

Color of Change swiftly organized what it describes as a social media campaign using the hashtag #NoBloodMoney.

In the wake of Charlottesville, which was shocking in the broader U.S. political environment and perceived as a watershed moment within tech companies, many industry participants made decisions to end services to a variety of groups they felt had violated their policies against promoting violence or extremism. This was sometimes proactively. It was sometimes after receiving communication from activists, either in their personal capacity or identified as coalition participants.

Meetings were, prior to this point, relatively ad hoc. This would soon change.

As mentioned above, the SPLC enjoyed broad trust within the financial industry dating to long before these events. Chase’s donation to SPLC immediately after a galvanizing tragedy could, if one were immensely cynical, be read as a tiny communications expenditure.

Industry participants routinely claimed shock and a sense of urgency after Charlottesville. A grown man once wept in my presence recounting that event. While there is substantial diversity of views among industry participants, many have, in their private spaces, when the cameras are not rolling, when there is nothing to gain, repeatedly described the SPLC to me as being on the side of the angels.

Keep this in mind as the coalition describes industry as being standoffish and foot-dragging.

The SPLC co-led an effort to unify, coordinate, and intensify previously ad hoc organizing actions. Change the Terms (CTT) was a coalition, to its friends, a conspiracy, to its enemies, and an unincorporated association, to a geek with an unhealthy interest in LLC formation. (The only fact I’ve ever retained about unincorporated associations is that they are jointly and severally liable for acts of the members.)

The individuals identified contemporaneously as co-chairing CTT were Heidi Beirich (then-head of the SPLC Intelligence Project) and Henry Fernandez, of the Center for American Progress (CAP).

SPLC’s Intelligence Project ran the private intelligence service and produced its data products. It also produces an annual intelligence estimate, such as the (2024) Year in Hate and Extremism.

(Beirich left SPLC in 2019 to co-found Global Project Against Hate and Extremism (GPAHE) with a fellow SPLC alumna.)

The SPLC characterized the CTT coalition as its own initiative under the Intelligence Project, and not simply Beirich’s initiative, in charitable governance and fundraising documents in the possession of Bits about Money. We cite one such document below, contrasted against later Congressional testimony.

According to documents reviewed by Bits about Money produced by coalition participants, the SPLC participated in cost-sharing arrangements to fund expenses of other coalition participants incurred in carrying out the joint purpose of the coalition. We are unaware of the extent of this practice.

CTT presently describes its most senior members as CAP, Color of Change, Common Cause, Free Press, GPAHE, Muslim Advocates, the National Hispanic Media Center, and the SPLC. There is some ambiguity around who claims founding member status and whether that list has evolved over time. Startup life, I get it.

I will refer to CTT’s primary artifact as the Terms. This document, announced at the coalition’s debut, was foundational to CTT’s positioning (they are Change the Terms). The Terms were sometimes described as recommendations, sometimes as a model Terms of Service (ToS). They were consistently positioned as being for Internet companies.

This is sleight-of-hand. A primary purpose, perhaps the primary purpose, of the Terms is to interdict money movement.

The Terms define “Internet Companies” in a non-standard fashion to include banks, credit card brands, any business of any character which facilitates a transfer of money with a web or mobile interface, and also more central examples of Internet companies. This is in keeping with the coalition’s by-now demonstrated target selection of PayPal (an Internet company) and Mastercard (which predates the commercial Internet by decades).

The SPLC co-drafted the Terms.

The SPLC referenced the Terms in Congressional testimony as being an extension of the SPLC’s long-running campaign to interdict money movement to targeted organizations.

For decades, the SPLC has been fighting hate and exposing how hate groups use the internet. We have lobbied internet companies, one by one, to comply with their own rules to prohibit their services from being used to foster hate or discrimination. A key part of this strategy has been to target these organizations’ funding.

The Change the Terms coalition existed to coordinate and parallelize execution on this tactic. In addition to nominating targets for existing policies, it extracted concessions from industry in the form of policy changes. The coalition, when minimizing its own power served its purposes, sometimes described all actual decisions as made by industry. The coalition was very candid when speaking with itself, with allies, and with industry participants. The coalition understood itself to have some degree of coercive power, and factually had some degree of coercive power, as we will discuss. It also secured delegated authority, routinely but not universally, as we have discussed.

Industry participants do not consider the Terms to be reasonably characterized as a ToS.

I would say the Terms are an advocacy artifact which adopts the stylization of a ToS without making any effort to be one. A ToS is a binding contract that industry customarily pays professionals to produce or adapt from firm-maintained templates appropriate to young startups. The English-language U.S. ToS of a major tech company has consumed more than 7 figures in bespoke services work, as a rule. The idea that a filesharing service and regulated U.S. depository institution could adopt the same ToS is fatuous on its face.

The purpose of the Terms was to get the meeting and, oh boy, did the coalition get them. I estimate they successfully achieved hundreds of meetings.

Color of Change’s Robinson was interviewed by Hillary Clinton on her podcast You and Me Both in March 2021. You and Me Both is available on major podcast platforms through iHeartRadio. Readers may recognize Clinton from other work.

Bits about Money has archived the podcast MP3 file, to make specified quotations findable via timestamps. Many professional podcasts use dynamic insertion of ads, which is good for advertising revenue but bad for reproducibility of timestamps across listeners. Please do not use the archive unless you need these specific timestamps.

Robinson confirms that CoC works with SPLC and that its relevant work began after the 2016 election (29:15).

Episode at 29:30:

We started calling the credit card companies. We started calling these payment processing companies. And you know what they told us? They said, oh, we're with you, but, you know, you have to talk to the banks. And then the bank said, you know, you have to talk to the credit card companies. So we start building the #NoBloodMoney campaign and we start building this platform. And, you know, we're not quite done with it all when Charlottesville happens.

Robinson describes a central tactic of the coalition: identifying particular accounts it wants deactivated, with a consequence if demands are not met. He claims this to have been demonstrably effective.

Multiple industry participants describe the same sequence of events across several invocations of the tactic. I feel it necessary to caveat causality, as described below.

Episode at 30:00:

We have been talking with you [companies] for months. We’ve given you these lists of white nationalist groups. And then within about twenty four hours [of launching the #NoBloodMoney campaign], they start sending us a list of white nationalist organizations that they are cutting off from processing. No law had changed.

Clinton interjects: Exactly.

Robinson locates this within his non-partisan broader political project.

Episode at 28:00:

We really built what I feel is a new strategy. It was focused not simply on resistance, but on opposition. What would it mean to not just resist but to build power, to oppose, so that we could get back to governing, focusing on winning real victories at the local level, while also recognizing that the game was not fair, that the rules were rigged, and that we couldn't simply say that what happened in 2016 was democracy. It was what happened.

Clinton later comments, at 31:20 :

Moving [your advocacy] to the private sector, and corporate power, was an incredibly smart approach.

Industry participants have, compared to anyone else in the world, broadly better information about account status, account history, position in pipelines, and similar. (This is not to say they have total awareness of all information in their possession, or that all employees of an industry participant have equivalent access to information and capacity to understand it. Some organizations tightly silo information internally by role.)

It is easy to infer causality from timelines without that being warranted. One mechanism for this: accounts may be in pipeline at the time of target nomination. An external observer will perceive “account active, nomination communicated, account closed shortly thereafter” and make the obvious inference.

If one understands one’s counterparty to have misunderstood something, one can correct them. Or not.

Industry participants describe a variety of tactics for extending olive branches to the coalition participants, including but not limited to acceding to demands. One such tactic was giving more visibility into pipelines than the broader public had, with or without influence on operation of those pipelines. “Thanks so much for bringing that to our attention. They are absolutely on our radar now.” can mean many things, including “Message received.”, “I confirm they are in pipeline.”, “I confirm they are in pipeline thanks to you.”

The CTT Terms include the following recommendation.

Many Internet Companies have granted special exemptions to official accounts, government actors and powerful people, allowing them to promote hateful activities, disinformation and other divisive behavior. Instead, these actors should be held to the same standards (if not higher standards) as regular users. There should be no special exemptions that allow the powerful to spread hate with impunity. Many official accounts at various social-media companies have circumvented platform policies despite promoting hateful activities, disinformation and other divisive behavior. Policies should apply equally to all users and must be enforced.

Industry participants perceived themselves as being in an impossible situation with regards to a handful of accounts which were both extremely vexatious to coalition members and obviously newsworthy. Consider how manifestly unwise it would be to intentionally deplatform the sitting, duly elected President of the United States. While nominally about a large class of users, industry participants describe the motivating examples brought up in meetings as consistently circling back to Trump, Tucker Carlson, and a very short list of other names.

The ADL, a coalition-aligned non-profit, co-authored a press release with some coalition members titled Deplatform Tucker Carlson.

The coalition benefits from the mistaken impression that it only asks platforms to remove accounts controlled by terrorist organizations. No. The first, unobjectionable list is the ante. After you’re in the hand, they raise you Tucker.

Once the coalition has achieved agreement in principle it defines the bounds of polite society, it soon broadens the ask, framing the new concession as something you have already committed to publicly.

The coalition often communicates the ask privately but the retaliation for non-compliance publicly. The public, mainstream media sources, and similar interpret the sudden coordinated pressure intensification as evidence that the targeted company has failed at the original commitment, the one about terrorist organizations.

In public communications, some coalition participants exhibit message discipline in locating the agency within the industry participants: the coalition “recommends” policies, the industry participant agrees to a policy, then the industry participant is responsible for enforcing what is now their own policy.

Coalition participants were, in the recollection of many industry participants, frequently undisciplined in meetings. They specifically nominated accounts for adverse actions, up to account closure, in no uncertain terms, and it was not a request.

Color of Change, at a minimum, was quite disciplined: they consistently adopted coercive conditional escalation as their default engagement model. Get the meeting, communicate demand, show a marketing brief of words and images that would be activated if you did not swiftly accede to the demand. This account is described by industry participants and by executive director Robinson to Fast Company, where he describes employing it “95% of the time.”

Coalition participants were inconsistently disciplined in their contemporaneous written records, some of which Bits about Money has reviewed. Authenticating these as true copies is tricky; authenticating public statements is not.

The Leadership Conference on Civil and Human Rights in October 2019 wrote Facebook a public letter, which the SPLC and many coalition members co-signed.

And yet, sabotaging your own efforts, Facebook recently announced that it would automatically deem speech from politicians to be newsworthy, even when it violated the company’s Community Standards; exempt politician-created content from its fact-checking program – permitting anyone running for office to post or purchase ads with falsehoods; and exempt content deemed to be “opinion” from its misinformation rules. Politicians should not get a blank check to lie, incite, spread hate, or oppress groups of people. Politicians are historically responsible for perpetuating discrimination and erecting barriers to voter participation, while autocrats throughout history have relied on mass media to rise to power and subjugate minority communities.

Note the conflation here of committing incitement (illegal), spreading hate/oppression (probably bad), and lying while being a politician (Tuesday). This sort of conflation, of attempting to box someone into a proposition they had never actually agreed to, was routine, in the view of some industry participants.

I contemporaneously viewed the brouhaha about politicians lying as being battlespace preparation for the 2020 election. First, establish the general principle that social media platforms had a duty to censor lies told in campaigning. (This was sometimes described as “misinformation,” to imply that an American politician lying was doing so in a Russian accent.) Then, seize on every lie in one very specific political campaign, and use the platforms to interdict that political campaign’s storytelling. I didn’t expect campaign financing shenanigans, because I have a strong prior that responsible professionals might fly close to the sun but do not attempt to fly through it. More on that later.

Industry participants have their own compliance issues to worry about and frequently perceived this two-step as being too cute by half. The aim was obvious to them. Industry participants describe coalition participants as stating directly that Trump lies frequently, and helpfully telling people with degrees in logic that it therefore follows that if lies cause decisioning, and Trump lies, Trump should be decisioned.

The SPLC has described the coalition's strategy in its own voice, in the most formal venue available to it: sworn testimony before Congress. Lecia Brooks, who self-identifies as senior SPLC leadership, appeared before the House Financial Services, Subcommittee on National Security, International Development and Monetary Policy on January 15th, 2020.

Verbatim quotes from prepared testimony:

For decades, the SPLC has been fighting hate and exposing how hate groups use the internet. We have lobbied internet companies, one by one, to comply with their own rules to prohibit their services from being used to foster hate or discrimination. A key part of this strategy has been to target these organizations’ funding.

The coalition was an extension of the SPLC Intelligence Project, identified as such in their 2018 Annual Report, pg 9 [archive]. A charity annual report is a governance and fundraising document exhaustively reviewed by professionals and customarily approved by the board. It would be uncharitable to argue the SPLC misunderstands or is dissimulating about its role in the coalition in that document.

Brooks, to Congress, chooses to describe the SPLC as a member of the coalition and not the animating force of it:

On Oct. 25, 2018, the Change the Terms coalition – including the SPLC and other civil rights groups – released a suite of recommended policies for technology companies that would take away the online microphone that hate groups use to recruit members, raise funds and organize violence. In response to Change the Terms’ advocacy, several Silicon Valley leaders have made promising changes that align with the coalition’s vision for a safer online world.

Brooks then lists several examples of specific wins the coalition achieved.

Brooks then claims these accomplishments advanced the SPLC’s mission. She implies that the coalition’s important work will continue.

Hate groups have clearly been damaged by the efforts of the SPLC and its allied organizations, including the Change the Terms coalition, to fight them and their funding sources online. But the fight is far from over.

Brooks had an opportunity to describe industry participants as valued partners. Brooks describes the SPLC’s relationship with industry participants in part as follows:

The public exposure was half the battle. We conducted the other part of the campaign privately. SPLC officials held dozens of meetings with top Silicon Valley executives. Some companies acted. Some took half steps. Others did little or nothing. But eventually, the far-right extremists who depended on Silicon Valley were beginning to feel the pain.

Brooks characterizes the SPLC’s tone in a similar fashion to industry participants quoted above.

She indirectly confirms one of the campaign’s core tactics: get the meeting, get a commitment under threat of coordinated public pressure, then judge progress against the commitment to be inadequate. In the next meeting, offer absolution and de-escalation, contingent on policy concessions. Repeat as desired.

The SPLC kept up the pressure, cajoling companies and exposing those that dragged their feet.